Vehicle systems manufacturer Commercial Vehicle Group (NASDAQ: CVGI) reported Q4 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 5.2% year on year to $154.8 million. The company’s full-year revenue guidance of $680 million at the midpoint came in 7.1% above analysts’ estimates. Its non-GAAP loss of $0.18 per share was 20% below analysts’ consensus estimates.

Is now the time to buy Commercial Vehicle Group? Find out by accessing our full research report, it’s free.

Commercial Vehicle Group (CVGI) Q4 CY2025 Highlights:

- Revenue: $154.8 million vs analyst estimates of $147.1 million (5.2% year-on-year decline, 5.2% beat)

- Adjusted EPS: -$0.18 vs analyst expectations of -$0.15 (20% miss)

- Adjusted EBITDA: $2.3 million vs analyst estimates of $2.21 million (1.5% margin, relatively in line)

- EBITDA guidance for the upcoming financial year 2026 is $27 million at the midpoint, above analyst estimates of $21.4 million

- Operating Margin: -1.2%, up from -2.8% in the same quarter last year

- Free Cash Flow was $8.71 million, up from -$30.59 million in the same quarter last year

- Market Capitalization: $57.47 million

James Ray, President and Chief Executive Officer, said, “We are encouraged by the resilience and consistency seen in our fourth quarter results. The actions we took to drive operational efficiencies and right-size our footprint continued to pay off, highlighted by the year-over-year gross margin improvement of 190 basis points seen last quarter. Our focus on our cost structure also drove a full year decline of $4.8 million in SG&A expenses in 2025. We expect to see continued operating leverage into 2026 as we ramp new business wins and our end markets stabilize and start to recover."

Company Overview

Formed from a partnership between two distinct companies, CVG (NASDAQ: CVGI) offers various components used in vehicles and systems used in warehouses.

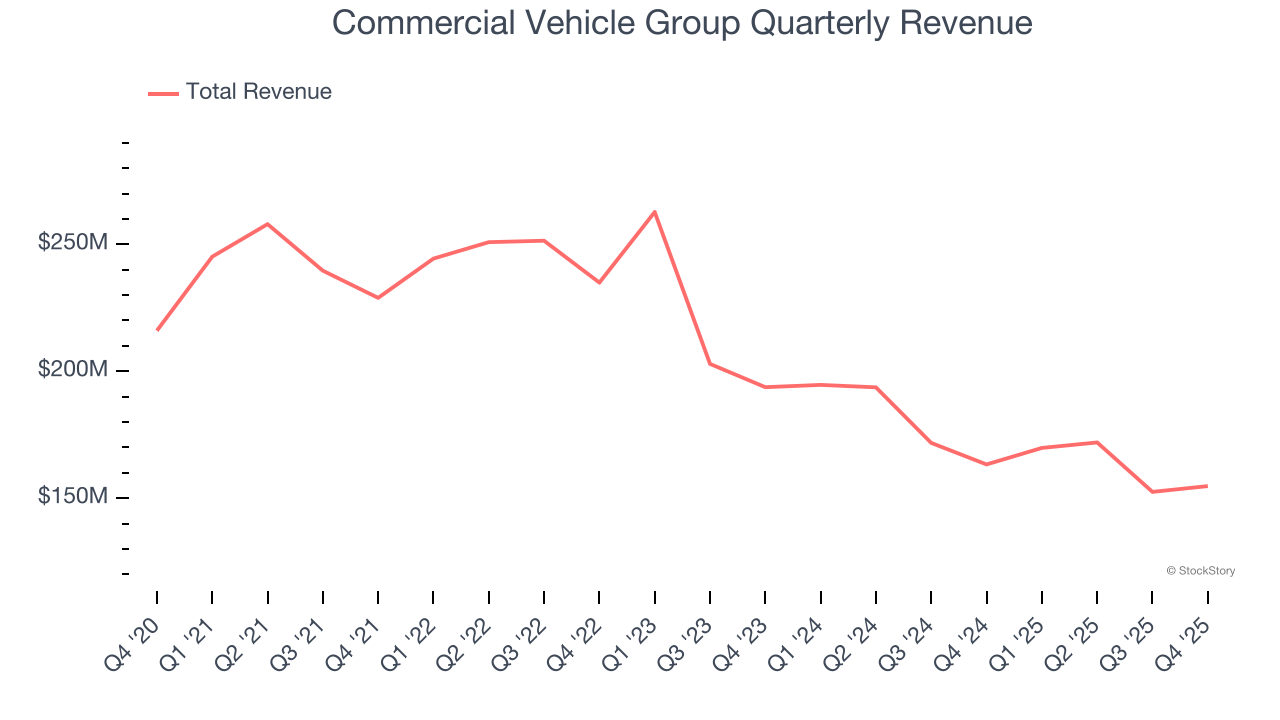

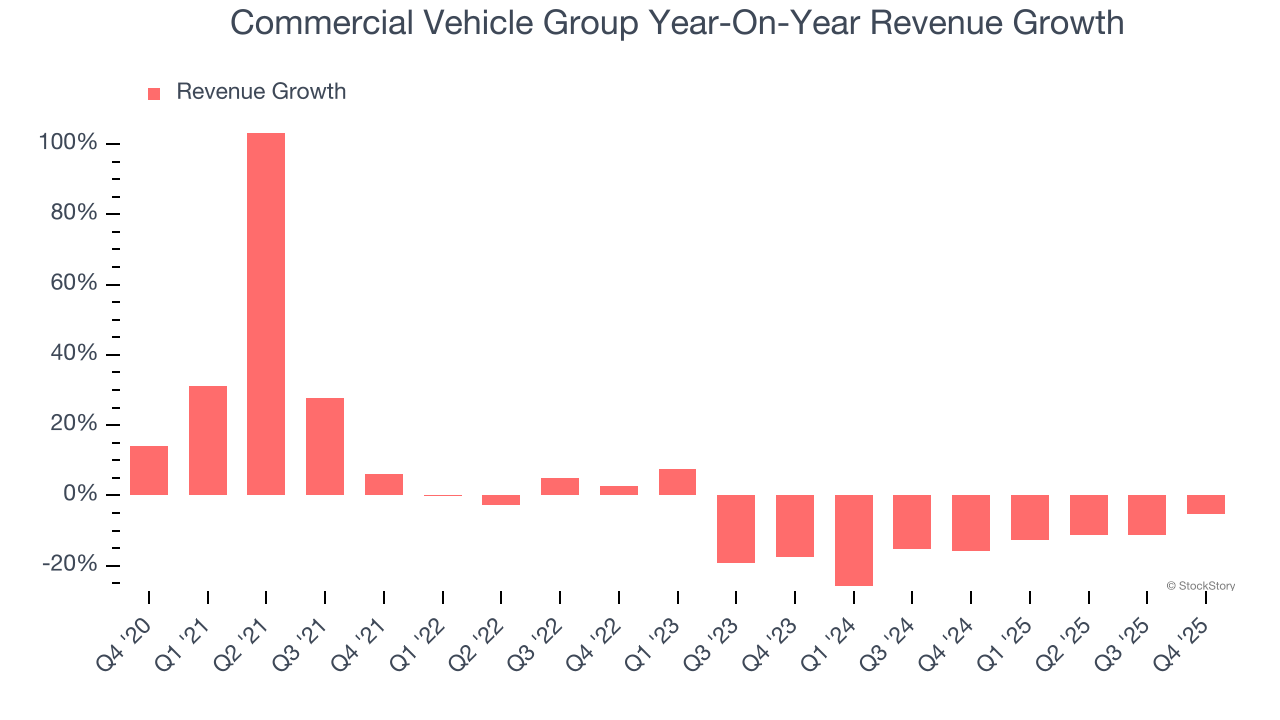

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Commercial Vehicle Group struggled to consistently generate demand over the last five years as its sales dropped at a 2% annual rate. This was below our standards and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Commercial Vehicle Group’s recent performance shows its demand remained suppressed as its revenue has declined by 14.9% annually over the last two years.

This quarter, Commercial Vehicle Group’s revenue fell by 5.2% year on year to $154.8 million but beat Wall Street’s estimates by 5.2%.

Looking ahead, sell-side analysts expect revenue to decline by 2.2% over the next 12 months. While this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

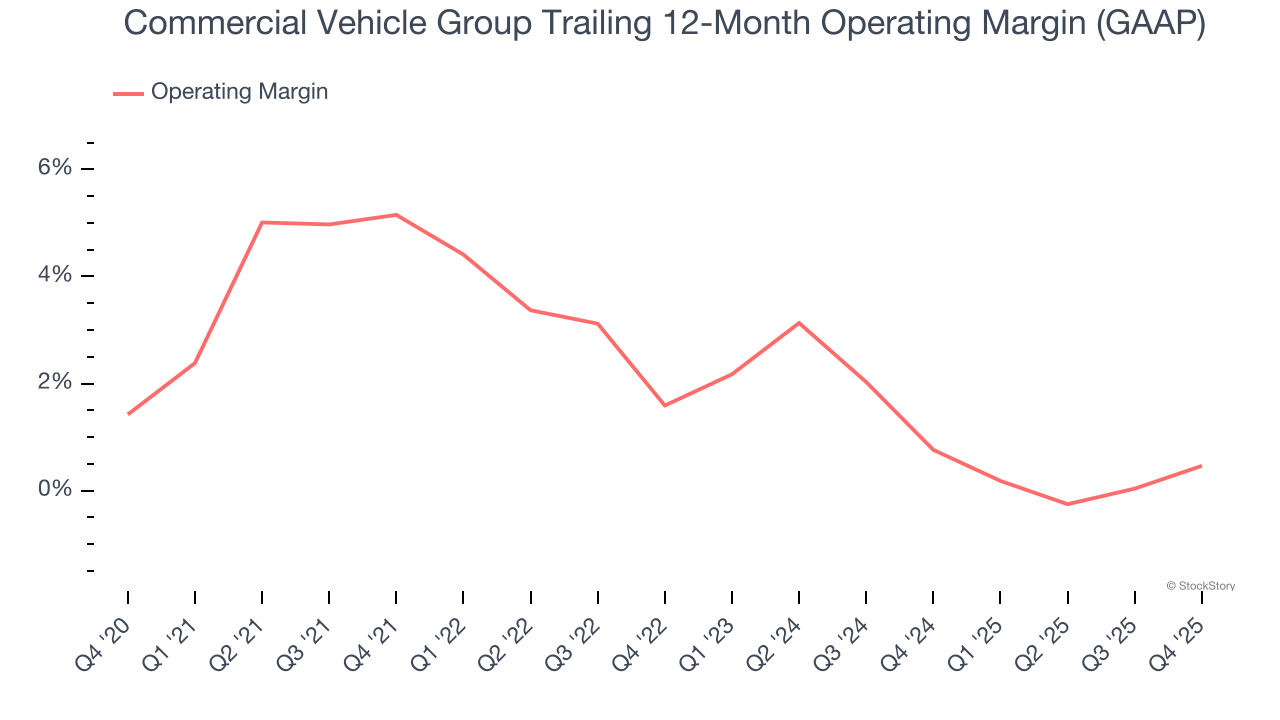

Operating Margin

Commercial Vehicle Group was profitable over the last five years but held back by its large cost base. Its average operating margin of 2.6% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Commercial Vehicle Group’s operating margin decreased by 4.7 percentage points over the last five years. Commercial Vehicle Group’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Commercial Vehicle Group generated an operating margin profit margin of negative 1.2%, up 1.6 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

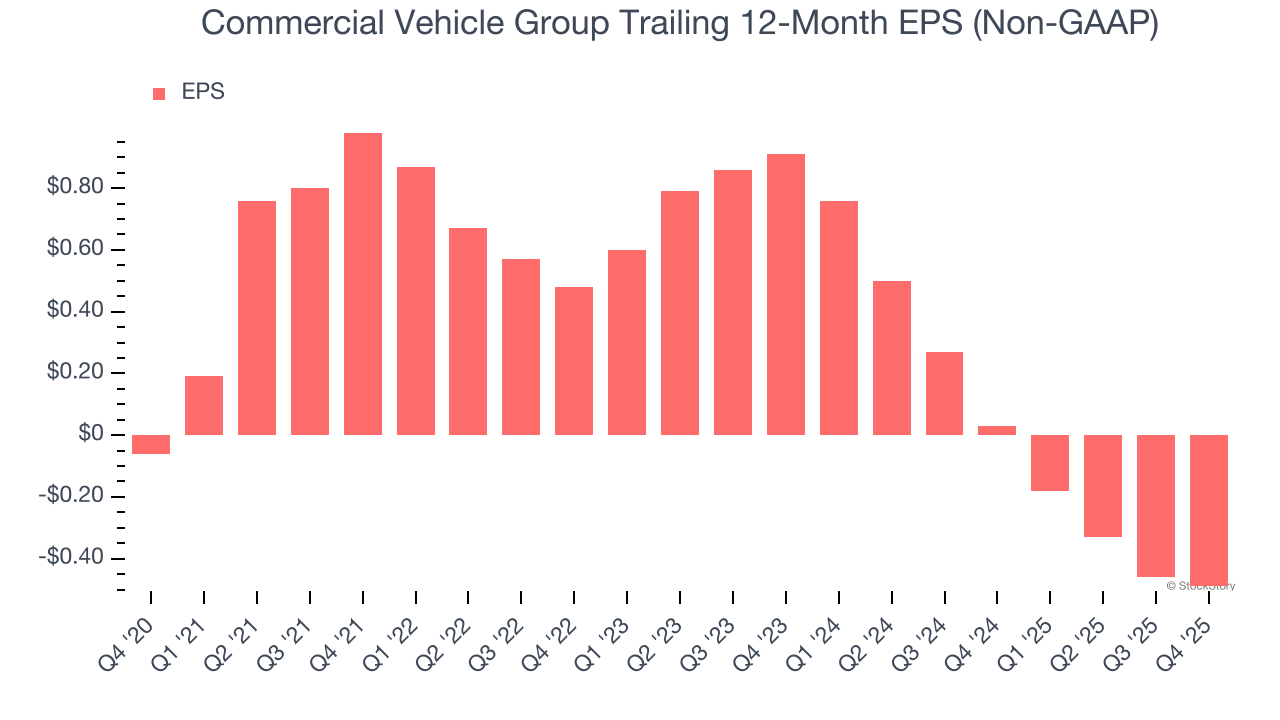

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Commercial Vehicle Group’s earnings losses deepened over the last five years as its EPS dropped 52.2% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Commercial Vehicle Group’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Commercial Vehicle Group, its EPS declined by more than its revenue over the last two years, dropping 59.3%. This tells us the company struggled to adjust to shrinking demand.

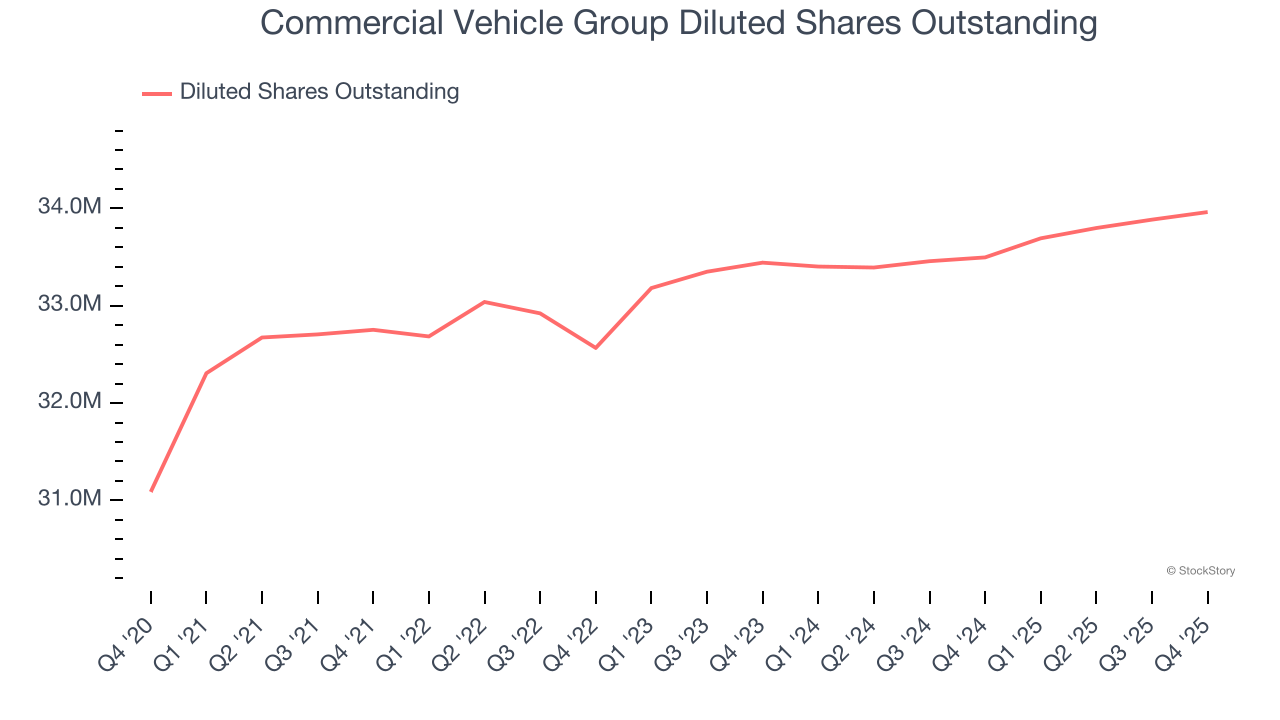

Diving into the nuances of Commercial Vehicle Group’s earnings can give us a better understanding of its performance. We mentioned earlier that Commercial Vehicle Group’s operating margin expanded this quarter, but a two-year view shows its margin has declinedwhile its share count has grown 1.6%. This means the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, Commercial Vehicle Group reported adjusted EPS of negative $0.18, down from negative $0.15 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Commercial Vehicle Group to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.49 will advance to negative $0.25.

Key Takeaways from Commercial Vehicle Group’s Q4 Results

We were impressed by how significantly Commercial Vehicle Group blew past analysts’ revenue expectations this quarter. We were also glad its full-year EBITDA guidance trumped Wall Street’s estimates. On the other hand, its EPS missed. Zooming out, we think this was a solid print. The stock traded up 24.5% to $2.02 immediately following the results.

Indeed, Commercial Vehicle Group had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).