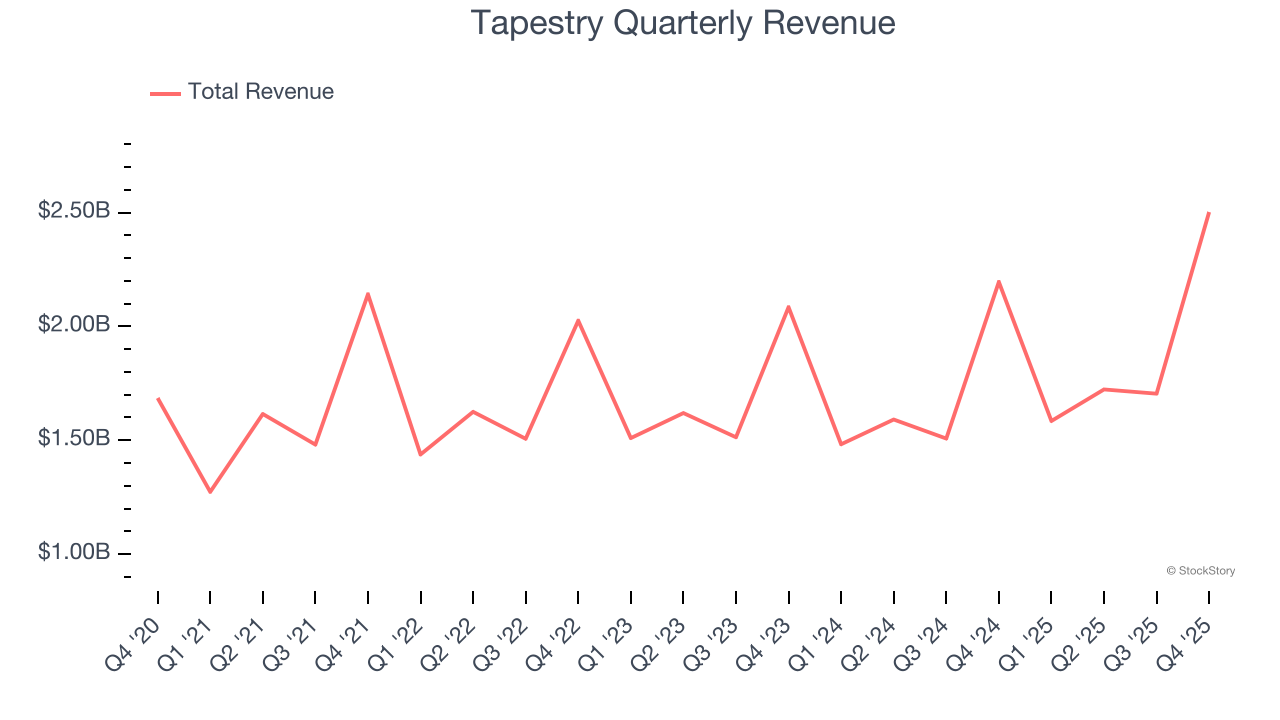

Luxury fashion conglomerate Tapestry (NYSE: TPR) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 14% year on year to $2.50 billion. The company’s full-year revenue guidance of $7.75 billion at the midpoint came in 4.8% above analysts’ estimates. Its GAAP profit of $2.68 per share was 20.7% above analysts’ consensus estimates.

Is now the time to buy Tapestry? Find out by accessing our full research report, it’s free.

Tapestry (TPR) Q4 CY2025 Highlights:

- Revenue: $2.50 billion vs analyst estimates of $2.32 billion (14% year-on-year growth, 7.7% beat)

- EPS (GAAP): $2.68 vs analyst estimates of $2.22 (20.7% beat)

- Adjusted EBITDA: $800 million vs analyst estimates of $655 million (32% margin, 22.1% beat)

- The company lifted its revenue guidance for the full year to $7.75 billion at the midpoint from $7.3 billion, a 6.2% increase

- EPS (GAAP) guidance for the full year is $6.43 at the midpoint, beating analyst estimates by 16.4%

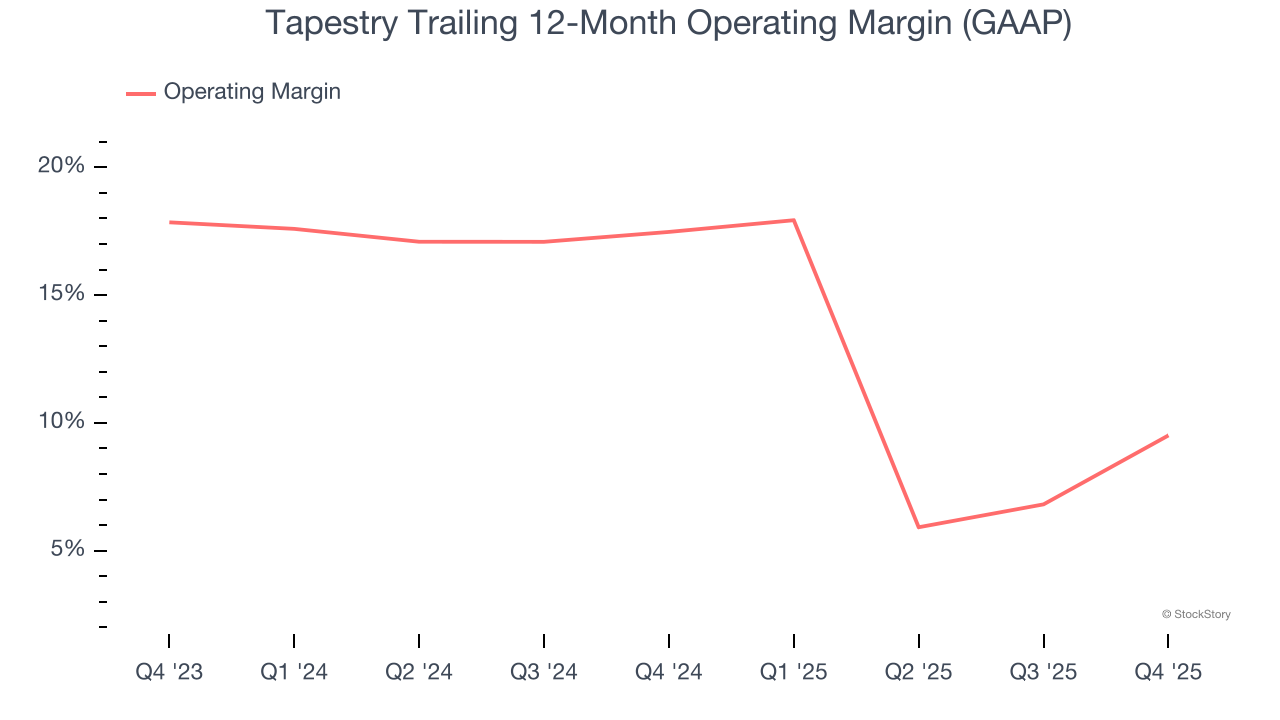

- Operating Margin: 28.6%, up from 22.4% in the same quarter last year

- Free Cash Flow Margin: 44.7%, up from 21.6% in the same quarter last year

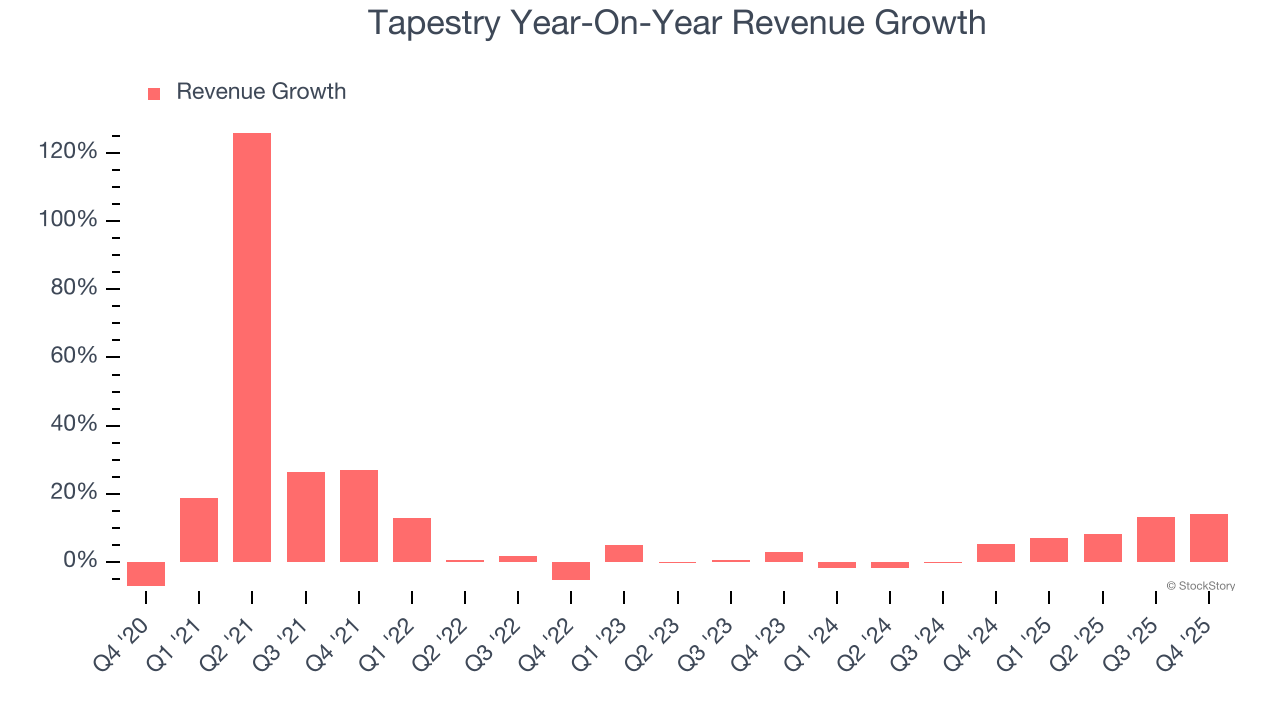

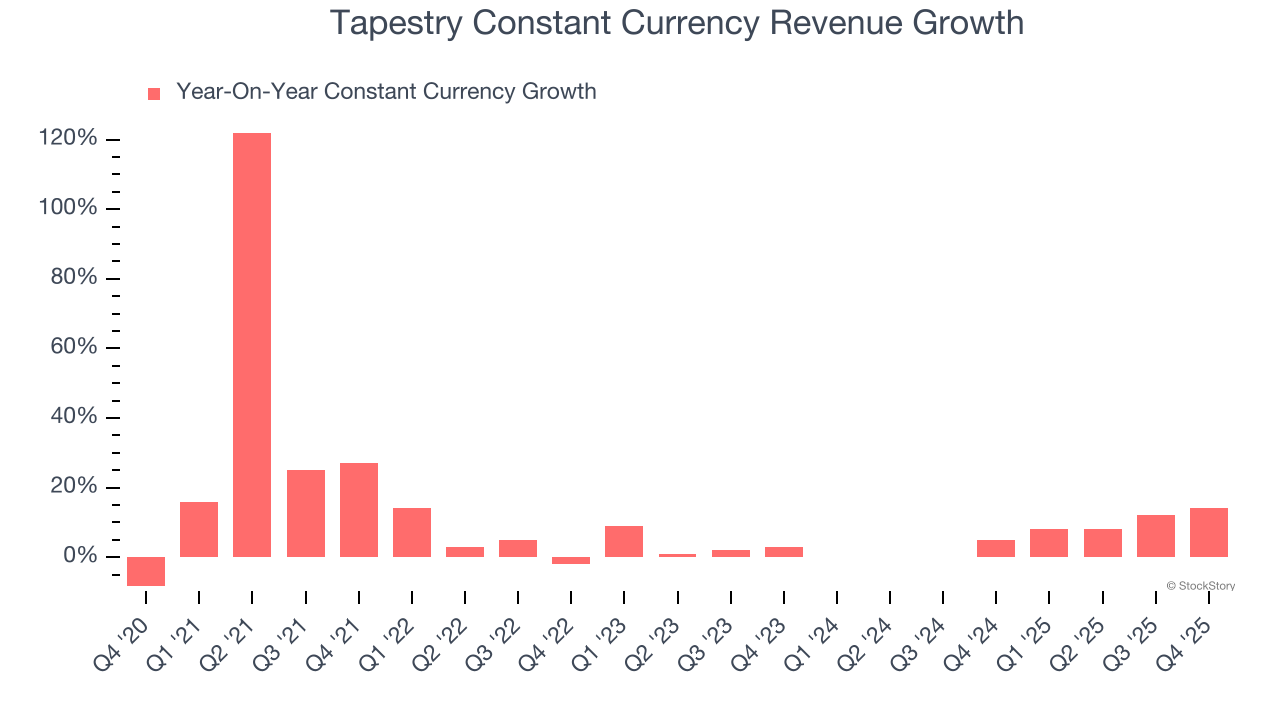

- Constant Currency Revenue rose 14% year on year (5% in the same quarter last year)

- Market Capitalization: $26.59 billion

Company Overview

Originally founded as Coach, Tapestry (NYSE: TPR) is an American fashion conglomerate with a portfolio of luxury brands offering high-quality accessories and fashion products.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Tapestry grew its sales at a 10.1% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Tapestry’s recent performance shows its demand has slowed as its annualized revenue growth of 5.7% over the last two years was below its five-year trend.

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 5.9% year-on-year growth. Because this number aligns with its normal revenue growth, we can see that Tapestry has properly hedged its foreign currency exposure.

This quarter, Tapestry reported year-on-year revenue growth of 14%, and its $2.50 billion of revenue exceeded Wall Street’s estimates by 7.7%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

Tapestry’s operating margin has shrunk over the last 12 months and averaged 13.3% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q4, Tapestry generated an operating margin profit margin of 28.6%, up 6.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

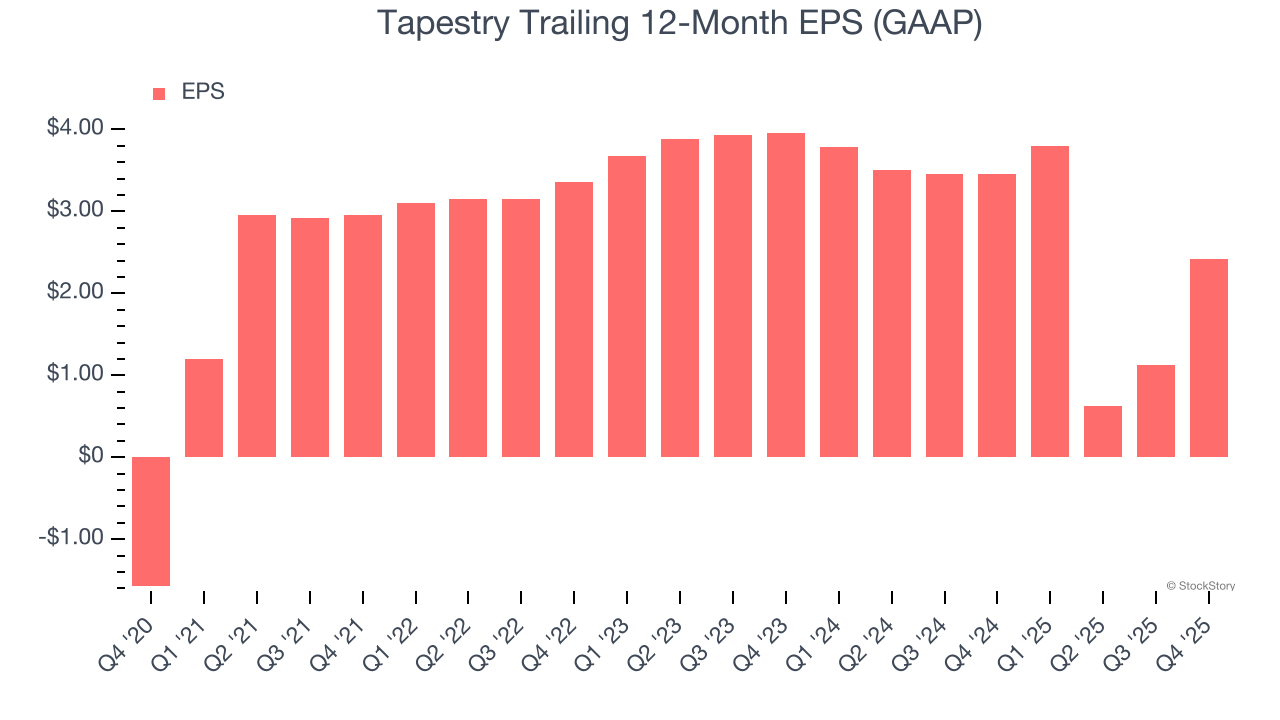

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Tapestry’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Tapestry reported EPS of $2.68, up from $1.38 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Tapestry’s full-year EPS of $2.42 to grow 142%.

Key Takeaways from Tapestry’s Q4 Results

We were impressed by how significantly Tapestry blew past analysts’ constant currency revenue expectations this quarter. We were also glad its full-year EPS guidance trumped Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 5% to $136.38 immediately following the results.

Tapestry put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).