Recreational boats manufacturer Malibu Boats (NASDAQ: MBUU) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, but sales fell by 5.8% year on year to $188.6 million. Its non-GAAP loss of $0.02 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Malibu Boats? Find out by accessing our full research report, it’s free.

Malibu Boats (MBUU) Q4 CY2025 Highlights:

- Revenue: $188.6 million vs analyst estimates of $181.4 million (5.8% year-on-year decline, 4% beat)

- Adjusted EPS: -$0.02 vs analyst estimates of $0.02 (significant miss)

- Adjusted EBITDA: $8.02 million vs analyst estimates of $8.99 million (4.3% margin, 10.8% miss)

- Operating Margin: -1.9%, down from 1.6% in the same quarter last year

- Market Capitalization: $665.4 million

"We exceeded second-quarter revenue expectations, despite a challenging retail environment and are optimistic entering the early boat show season," commented Steve Menneto, President and Chief Executive Officer of Malibu Boats, Inc.

Company Overview

Founded in California in 1982, Malibu Boats (NASDAQ: MBUU) is a manufacturer of high-performance sports boats and luxury watercrafts.

Revenue Growth

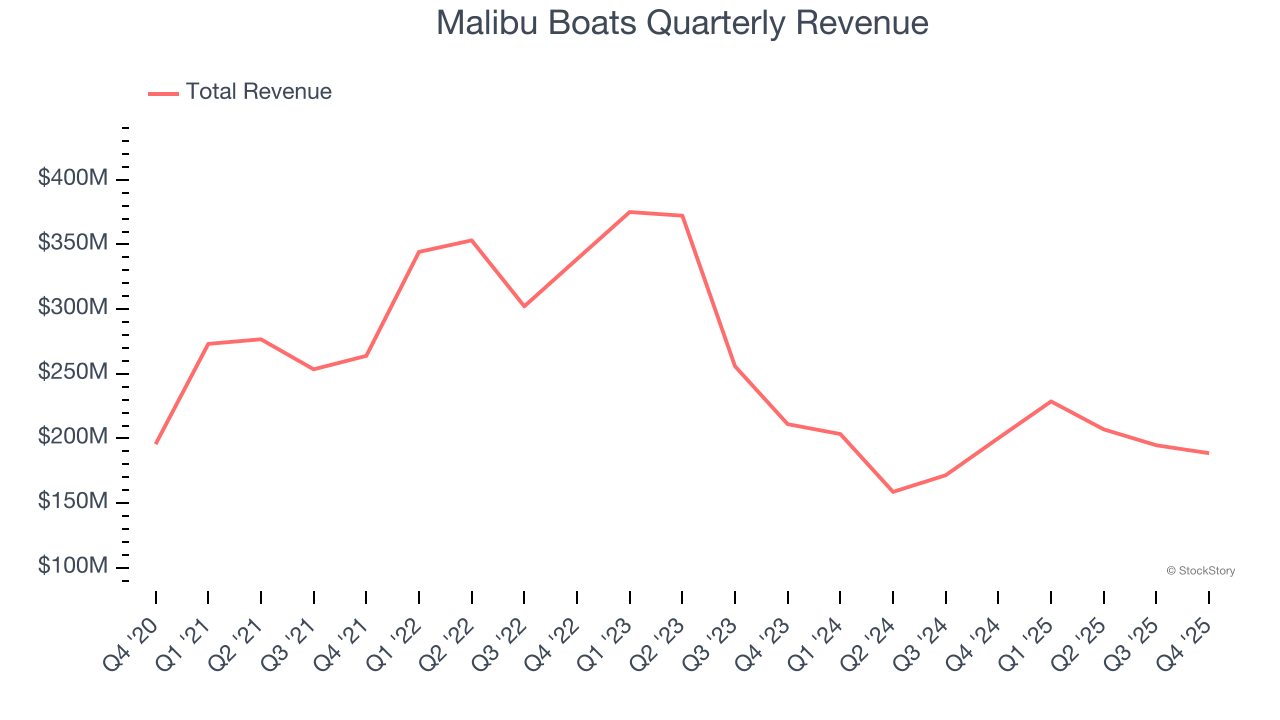

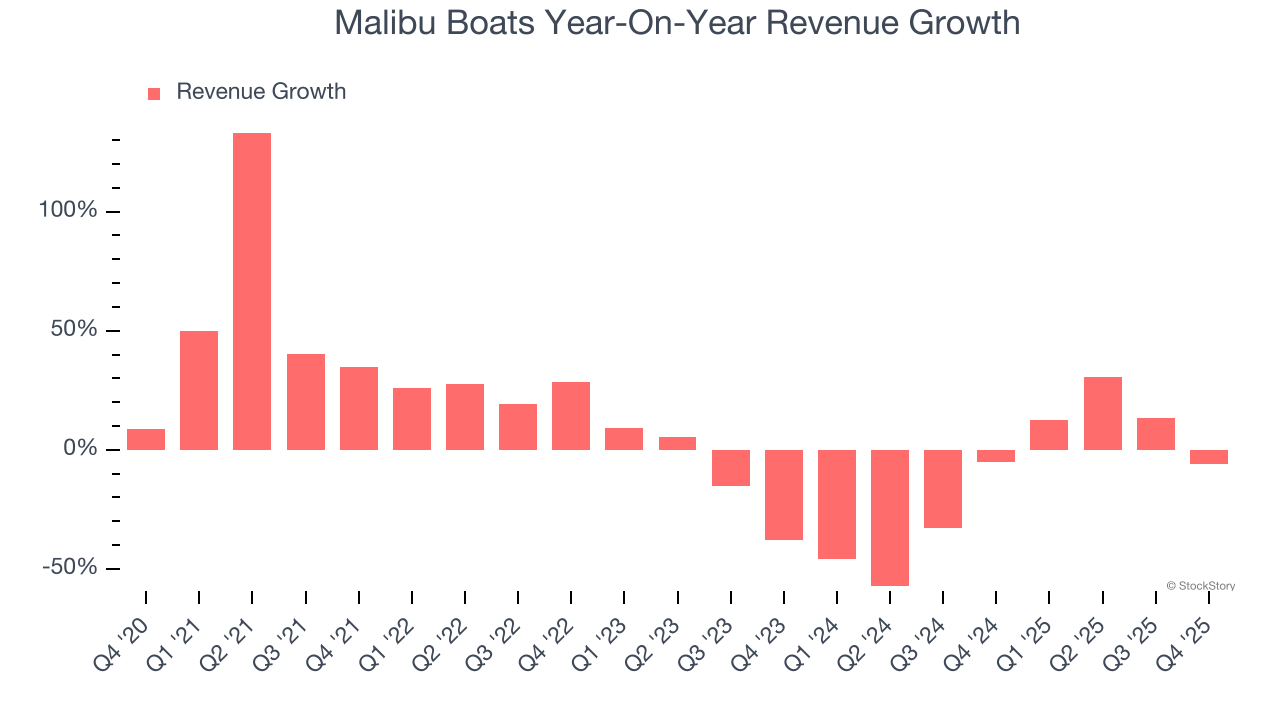

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Malibu Boats’s 3.9% annualized revenue growth over the last five years was weak. This fell short of our benchmark for the consumer discretionary sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Malibu Boats’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 17.9% annually.

This quarter, Malibu Boats’s revenue fell by 5.8% year on year to $188.6 million but beat Wall Street’s estimates by 4%.

Looking ahead, sell-side analysts expect revenue to decline by 1.4% over the next 12 months. Although this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

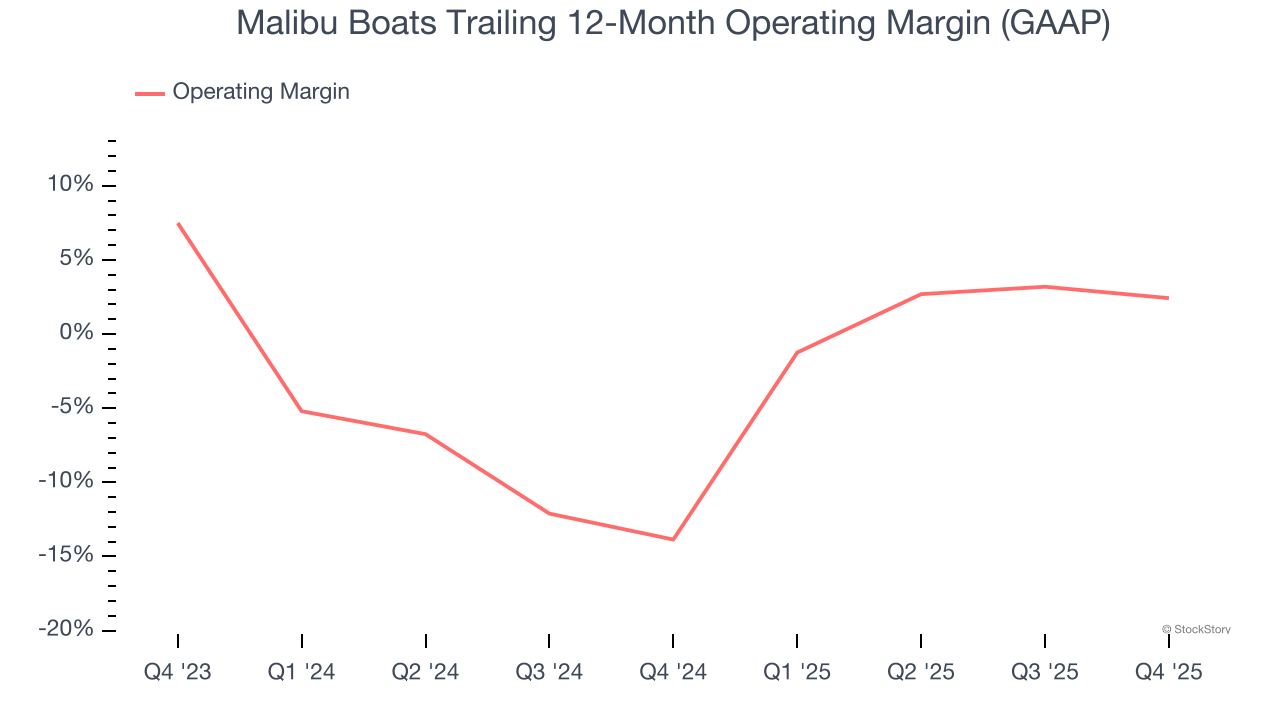

Malibu Boats’s operating margin has been trending up over the last 12 months, but it still averaged negative 5.3% over the last two years. This is due to its large expense base and inefficient cost structure.

Malibu Boats’s operating margin was negative 1.9% this quarter. The company's consistent lack of profits raise a flag.

Earnings Per Share

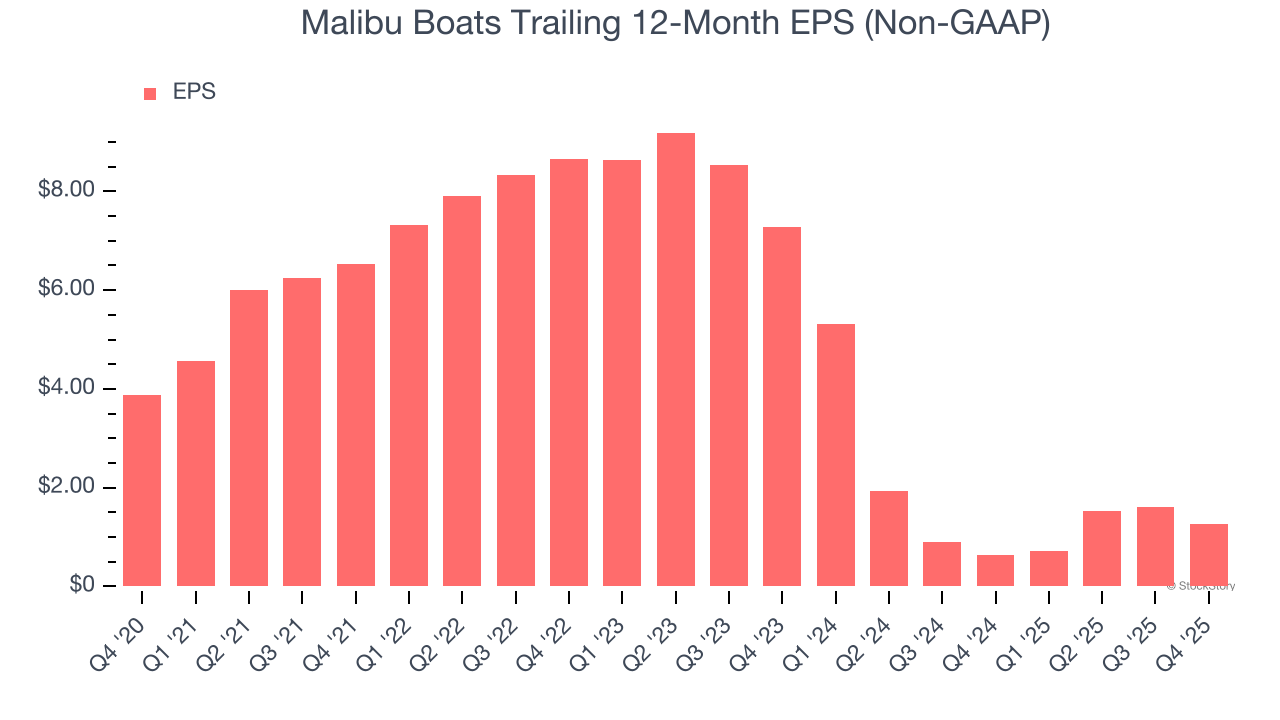

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Malibu Boats, its EPS declined by 20% annually over the last five years while its revenue grew by 3.9%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

In Q4, Malibu Boats reported adjusted EPS of negative $0.02, down from $0.31 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Malibu Boats’s full-year EPS of $1.27 to grow 17.1%.

Key Takeaways from Malibu Boats’s Q4 Results

It was encouraging to see Malibu Boats beat analysts’ revenue expectations this quarter. On the other hand, its EPS missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $34.54 immediately after reporting.

Malibu Boats underperformed this quarter, but does that create an opportunity to invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).