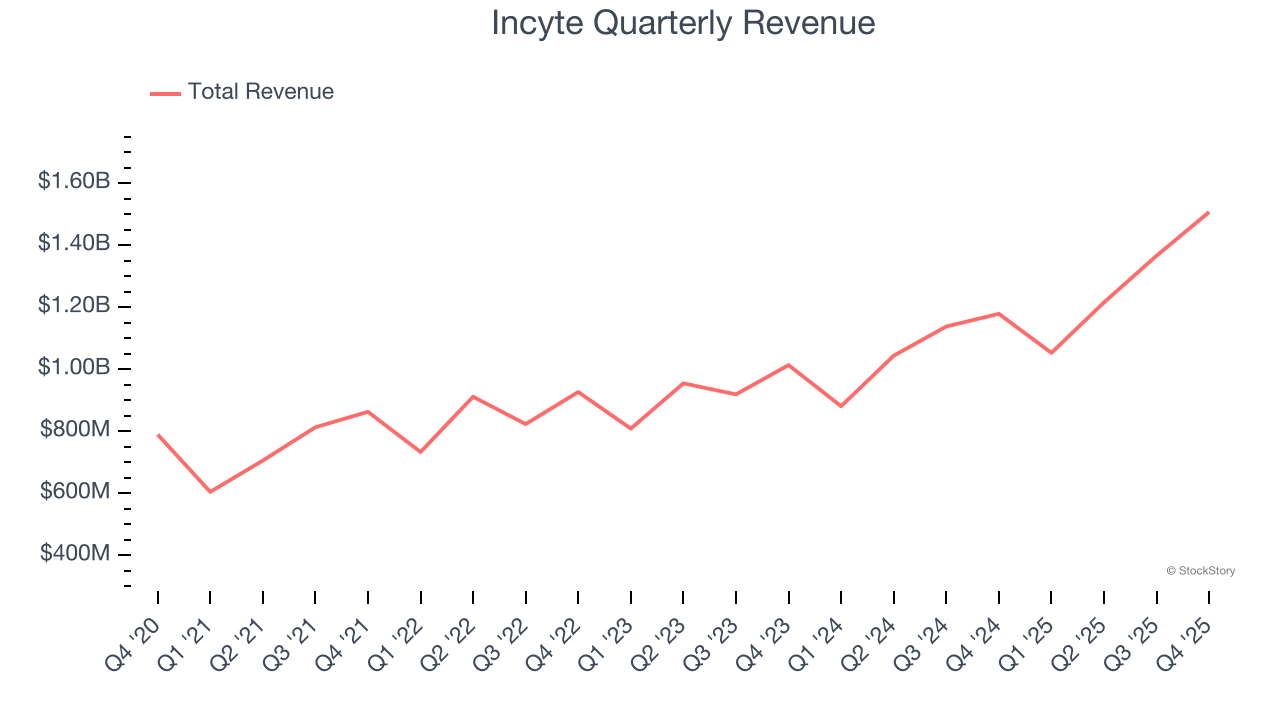

Biopharmaceutical company Incyte Corporation (NASDAQ: INCY) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 27.8% year on year to $1.51 billion. Its non-GAAP profit of $1.80 per share was 6.1% below analysts’ consensus estimates.

Is now the time to buy Incyte? Find out by accessing our full research report, it’s free.

Incyte (INCY) Q4 CY2025 Highlights:

- Revenue: $1.51 billion vs analyst estimates of $1.35 billion (27.8% year-on-year growth, 11.4% beat)

- Adjusted EPS: $1.80 vs analyst expectations of $1.92 (6.1% miss)

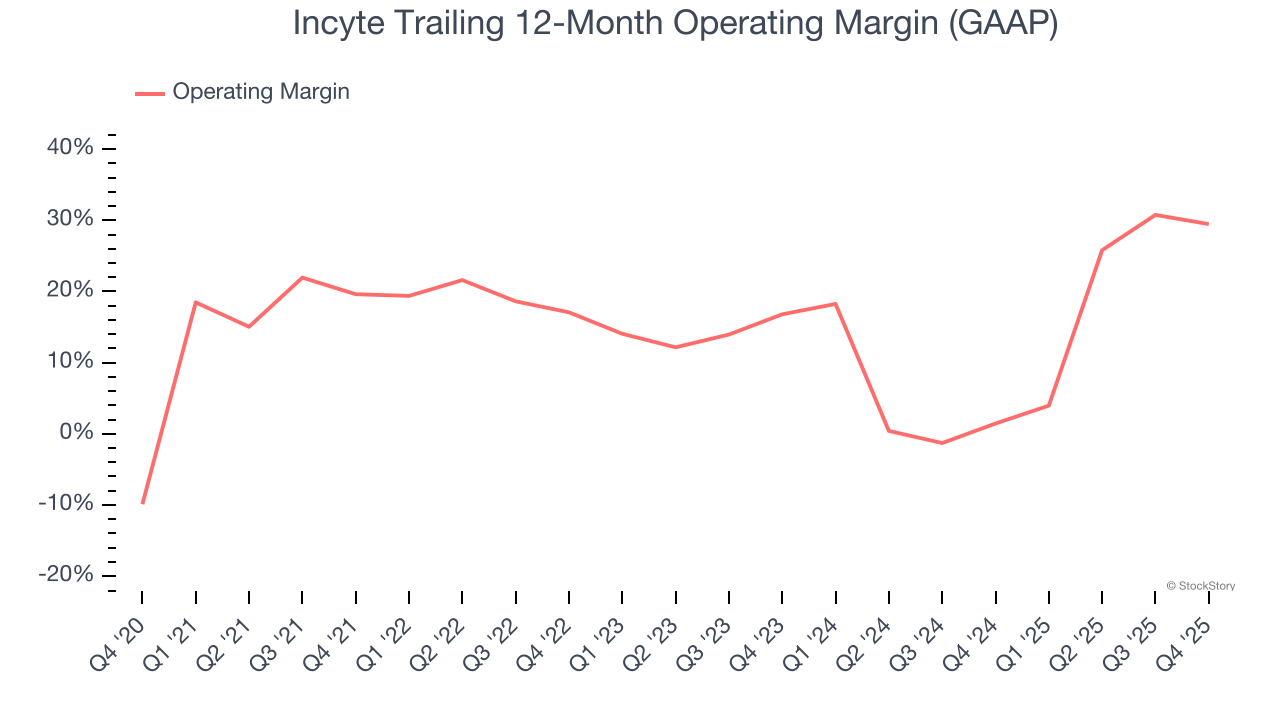

- Operating Margin: 22.3%, down from 25.6% in the same quarter last year

- Market Capitalization: $21.41 billion

“Our fourth quarter and full year 2025 results reflect exceptional core business growth and pipeline progress,” said Bill Meury, President and Chief Executive Officer, Incyte.

Company Overview

Founded in 1991 and evolving from a genomics research firm to a commercial-stage drug developer, Incyte (NASDAQ: INCY) is a biopharmaceutical company that discovers, develops, and commercializes proprietary therapeutics for cancer and inflammatory diseases.

Revenue Growth

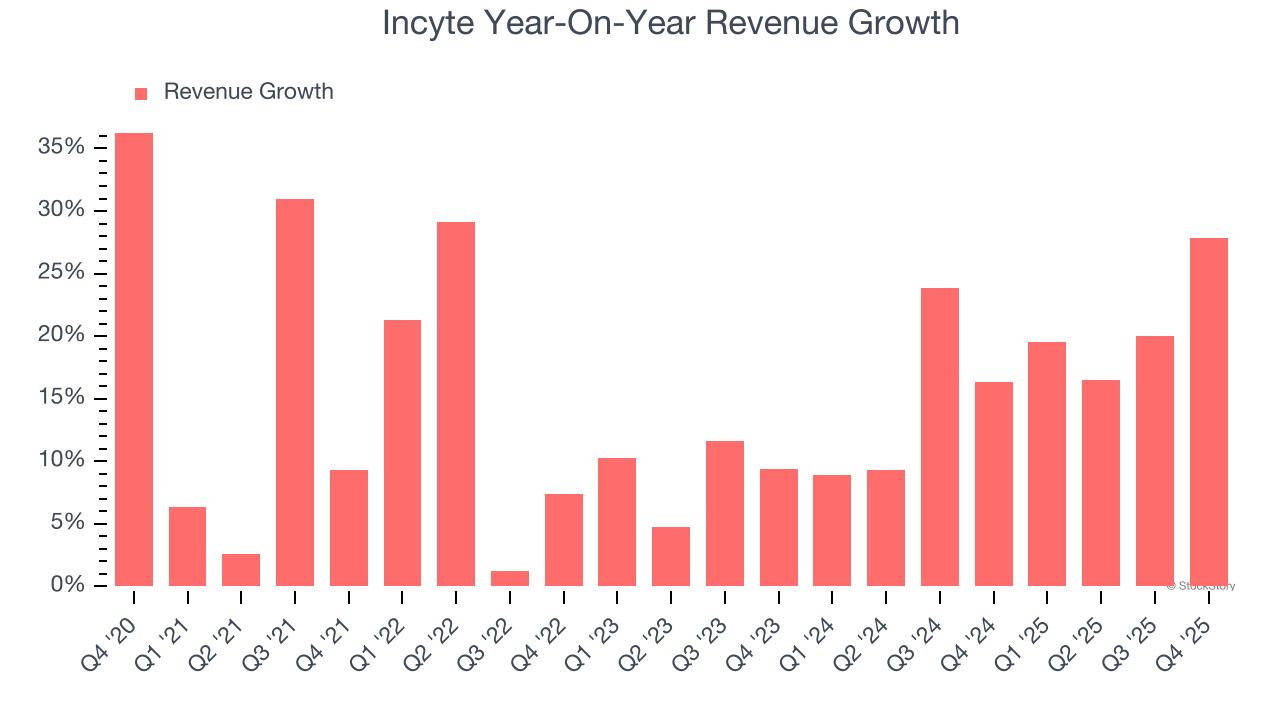

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Incyte grew its sales at a solid 14% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Incyte’s annualized revenue growth of 17.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Incyte reported robust year-on-year revenue growth of 27.8%, and its $1.51 billion of revenue topped Wall Street estimates by 11.4%.

Looking ahead, sell-side analysts expect revenue to grow 7.3% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is above the sector average and suggests the market is forecasting some success for its newer products and services.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Incyte has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average operating margin of 17.3%.

Analyzing the trend in its profitability, Incyte’s operating margin rose by 9.8 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its recent improvements as the company’s margin has increased by 12.7 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

In Q4, Incyte generated an operating margin profit margin of 22.3%, down 3.3 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

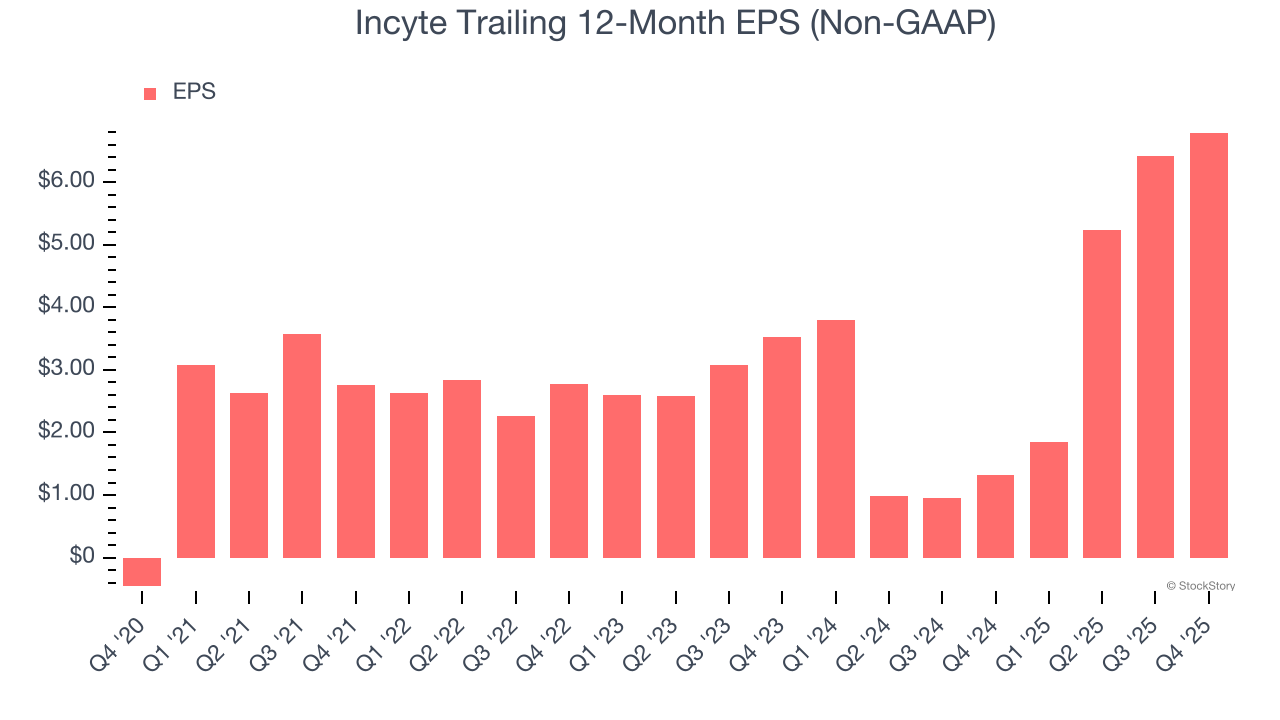

Incyte’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

In Q4, Incyte reported adjusted EPS of $1.80, up from $1.43 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Incyte’s full-year EPS of $6.79 to grow 19.1%.

Key Takeaways from Incyte’s Q4 Results

We were impressed by how significantly Incyte blew past analysts’ revenue expectations this quarter. On the other hand, its EPS missed. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 3.8% to $105.50 immediately after reporting.

Big picture, is Incyte a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).