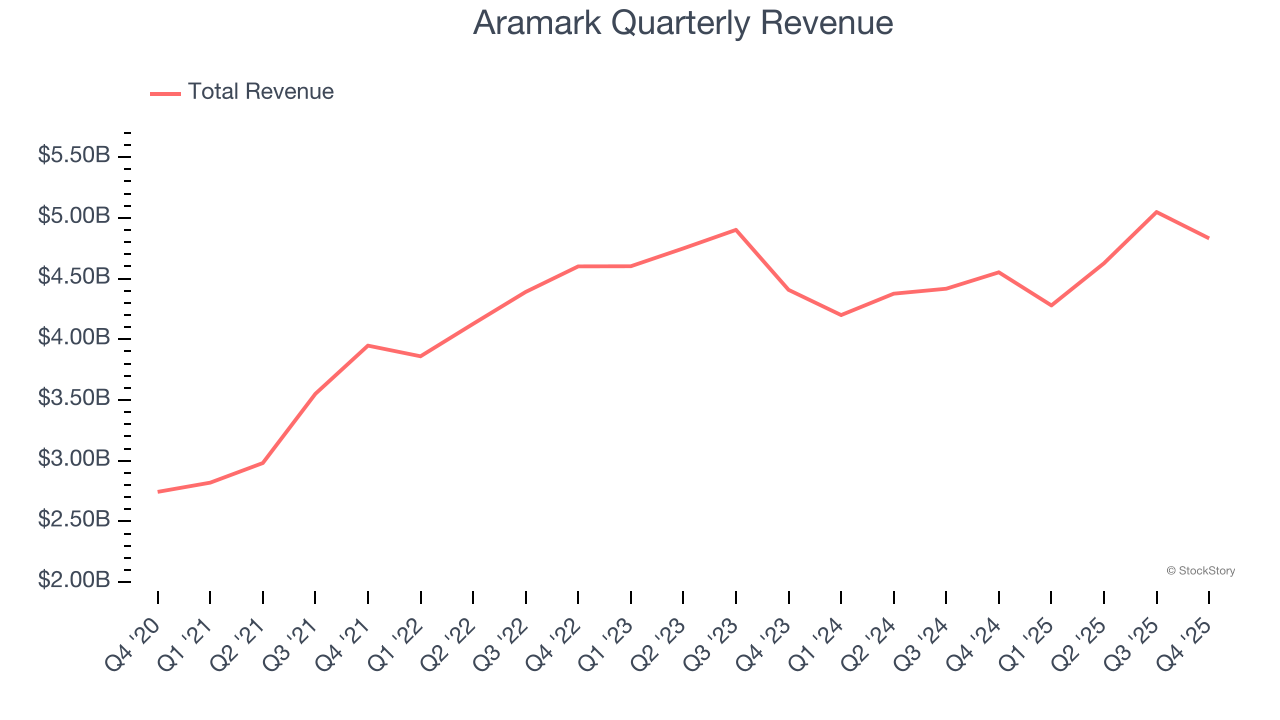

Food and facilities services provider Aramark (NYSE: ARMK) announced better-than-expected revenue in Q4 CY2025, with sales up 6.1% year on year to $4.83 billion. The company expects the full year’s revenue to be around $19.75 billion, close to analysts’ estimates. Its GAAP profit of $0.36 per share was 20.1% below analysts’ consensus estimates.

Is now the time to buy Aramark? Find out by accessing our full research report, it’s free.

Aramark (ARMK) Q4 CY2025 Highlights:

- Revenue: $4.83 billion vs analyst estimates of $4.75 billion (6.1% year-on-year growth, 1.8% beat)

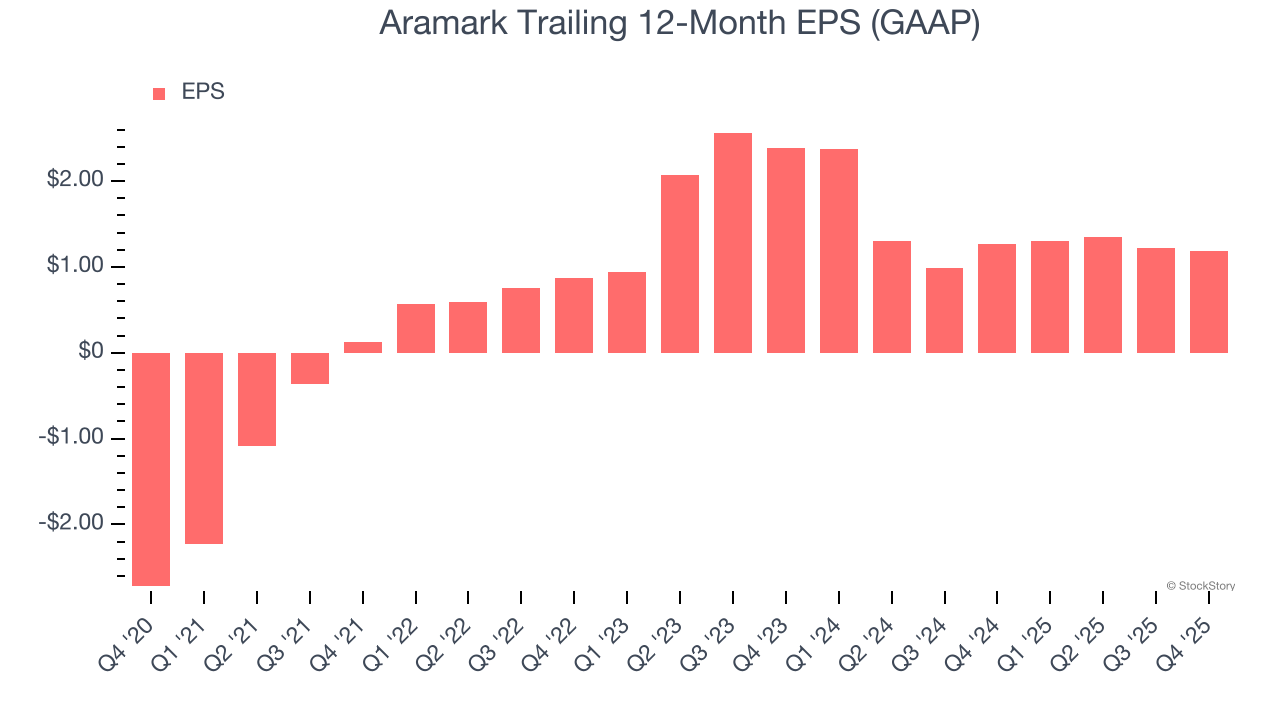

- EPS (GAAP): $0.36 vs analyst expectations of $0.45 (20.1% miss)

- Adjusted EBITDA: $359.8 million vs analyst estimates of $361.4 million (7.4% margin, in line)

- The company reconfirmed its revenue guidance for the full year of $19.75 billion at the midpoint

- EPS (GAAP) guidance for the full year is $2.23 at the midpoint, beating analyst estimates by 16.4%

- Operating Margin: 4.5%, in line with the same quarter last year

- Free Cash Flow was -$902.2 million compared to -$707 million in the same quarter last year

- Market Capitalization: $10.2 billion

Company Overview

From serving hot dogs at major league stadiums to managing college dining halls that feed thousands daily, Aramark (NYSE: ARMK) provides food services and facilities management to schools, healthcare facilities, businesses, sports venues, and correctional institutions across 16 countries.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $18.79 billion in revenue over the past 12 months, Aramark is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices.

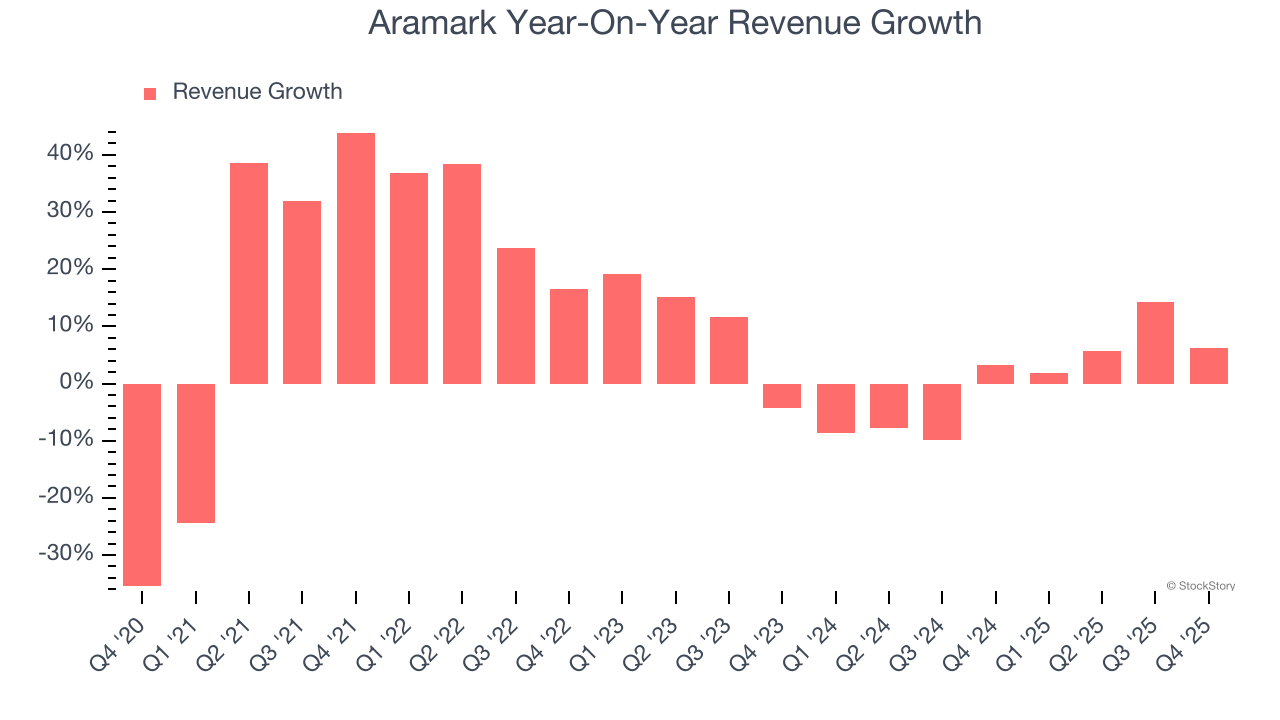

As you can see below, Aramark’s sales grew at an impressive 10.7% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Aramark’s recent performance shows its demand has slowed significantly as its revenue was flat over the last two years.

This quarter, Aramark reported year-on-year revenue growth of 6.1%, and its $4.83 billion of revenue exceeded Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow 6.2% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and implies its newer products and services will catalyze better top-line performance.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

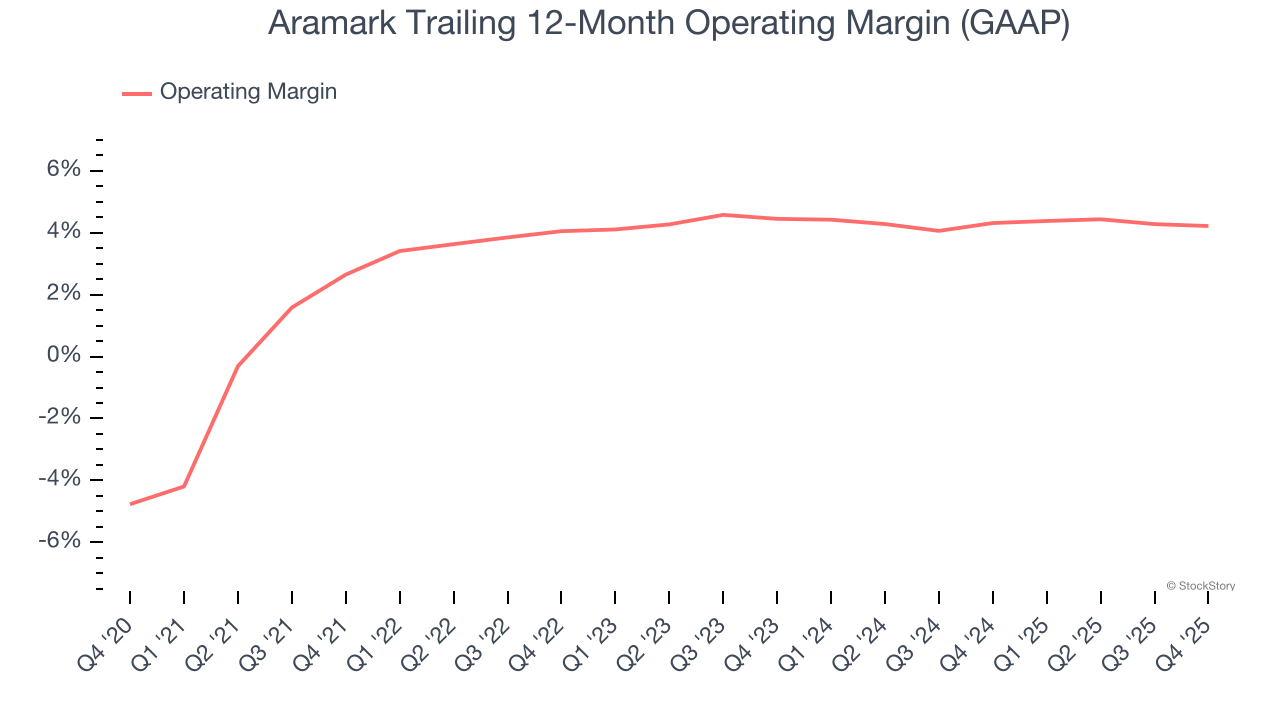

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Aramark was profitable over the last five years but held back by its large cost base. Its average operating margin of 4% was weak for a business services business.

On the plus side, Aramark’s operating margin rose by 1.6 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q4, Aramark generated an operating margin profit margin of 4.5%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Aramark’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Aramark, its EPS declined by 29.5% annually over the last two years while its revenue was flat. This tells us the company struggled to adjust to choppy demand.

In Q4, Aramark reported EPS of $0.36, down from $0.39 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Aramark’s full-year EPS of $1.19 to grow 73.5%.

Key Takeaways from Aramark’s Q4 Results

We were impressed by how significantly Aramark blew past analysts’ full-year EPS guidance expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed. Zooming out, we think this was a mixed quarter. The stock remained flat at $38.86 immediately after reporting.

Is Aramark an attractive investment opportunity right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).