PubMatic has gotten torched over the last six months - since July 2025, its stock price has dropped 41.4% to $7.49 per share. This might have investors contemplating their next move.

Is now the time to buy PubMatic, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think PubMatic Will Underperform?

Even with the cheaper entry price, we're swiping left on PubMatic for now. Here are three reasons why PUBM doesn't excite us and a stock we'd rather own.

1. Customer Churn Hurts Long-Term Outlook

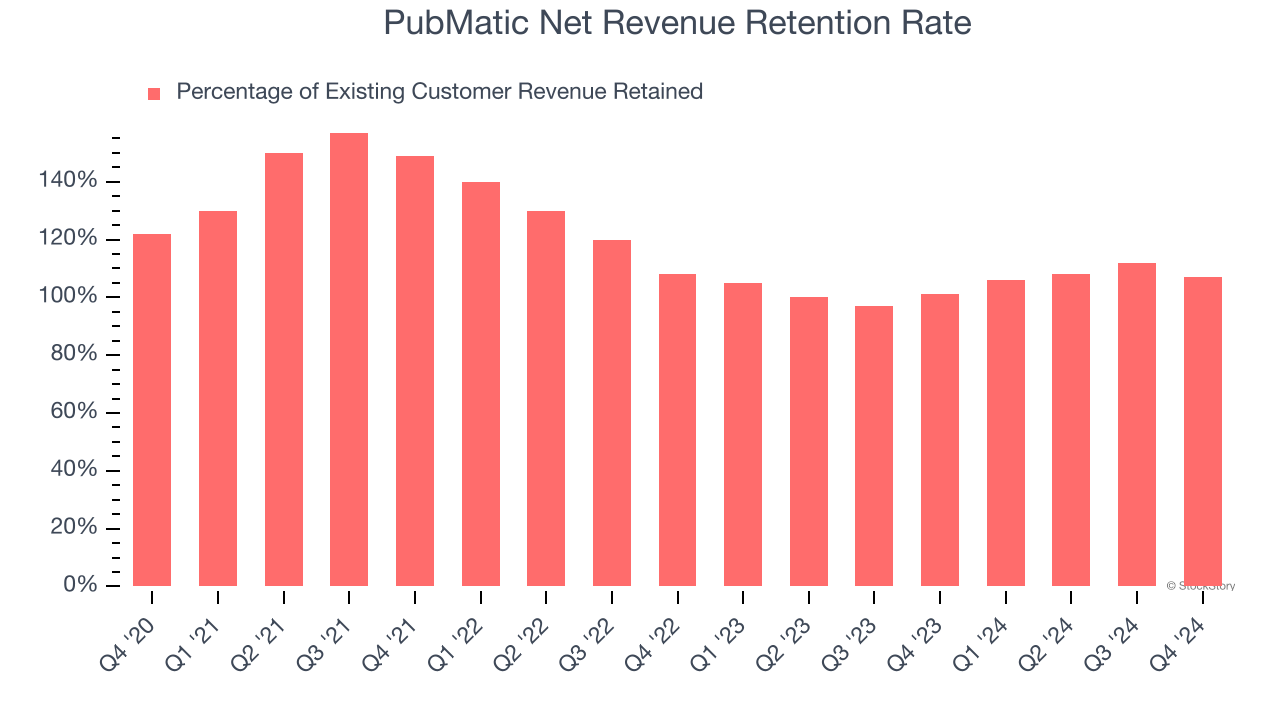

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

PubMatic’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 107% in Q3. This means PubMatic would’ve grown its revenue by 7% even if it didn’t win any new customers over the last 12 months.

PubMatic has a decent net retention rate, showing us that its customers not only tend to stick around but also get increasing value from its software over time.

2. Long Payback Periods Delay Returns

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

PubMatic’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between PubMatic’s products and its peers.

3. Cash Flow Margin Set to Decline

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the next year, analysts predict PubMatic’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 16.7% for the last 12 months will decrease to 25.6%.

Final Judgment

We cheer for all companies solving complex business issues, but in the case of PubMatic, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 1.3× forward price-to-sales (or $7.49 per share). At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment. We’d recommend looking at one of our all-time favorite software stocks.

Stocks We Would Buy Instead of PubMatic

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.