Over the past six months, Maximus has been a great trade, beating the S&P 500 by 9.1%. Its stock price has climbed to $86.33, representing a healthy 20.4% increase. This run-up might have investors contemplating their next move.

Is now still a good time to buy MMS? Or are investors being too optimistic? Find out in our full research report, it’s free for active Edge members.

Why Does MMS Stock Spark Debate?

With nearly 50 years of experience translating public policy into operational programs that serve millions of citizens, Maximus (NYSE: MMS) provides operational services, clinical assessments, and technology solutions to government agencies in the U.S. and internationally.

Two Positive Attributes:

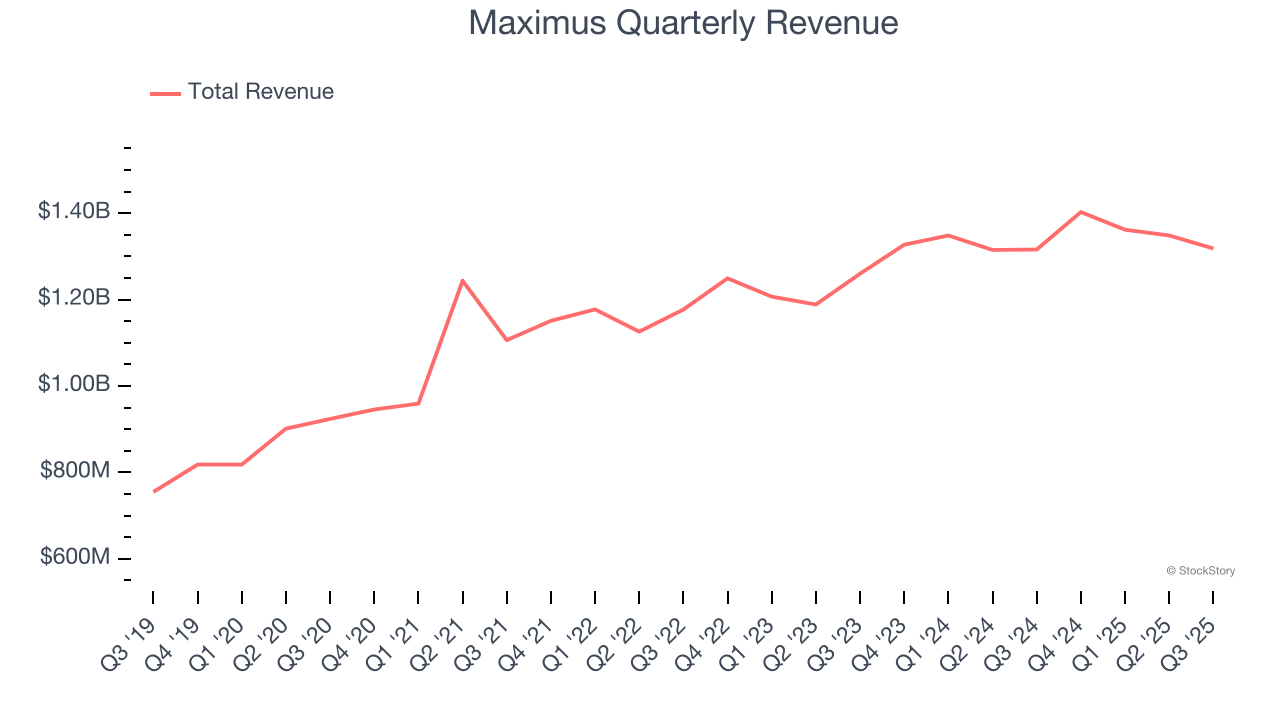

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Maximus’s sales grew at an impressive 9.4% compounded annual growth rate over the last five years. Its growth beat the average business services company and shows its offerings resonate with customers.

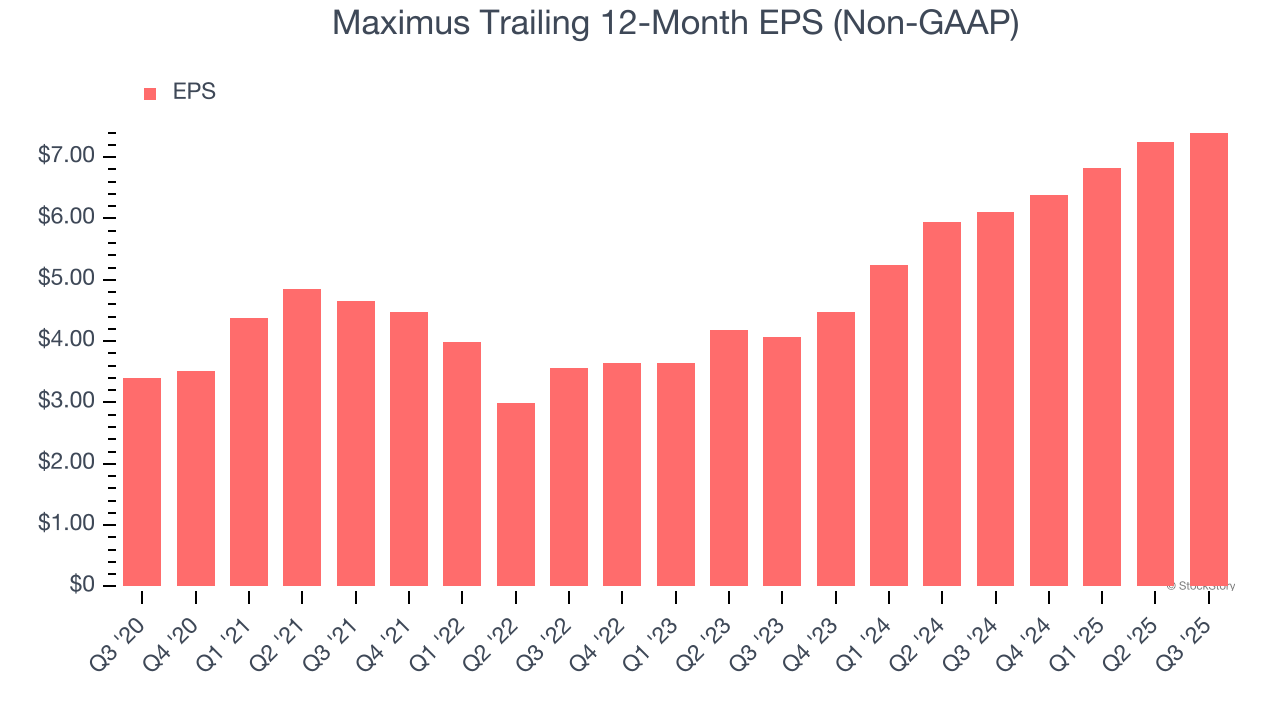

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Maximus’s EPS grew at an astounding 16.8% compounded annual growth rate over the last five years, higher than its 9.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

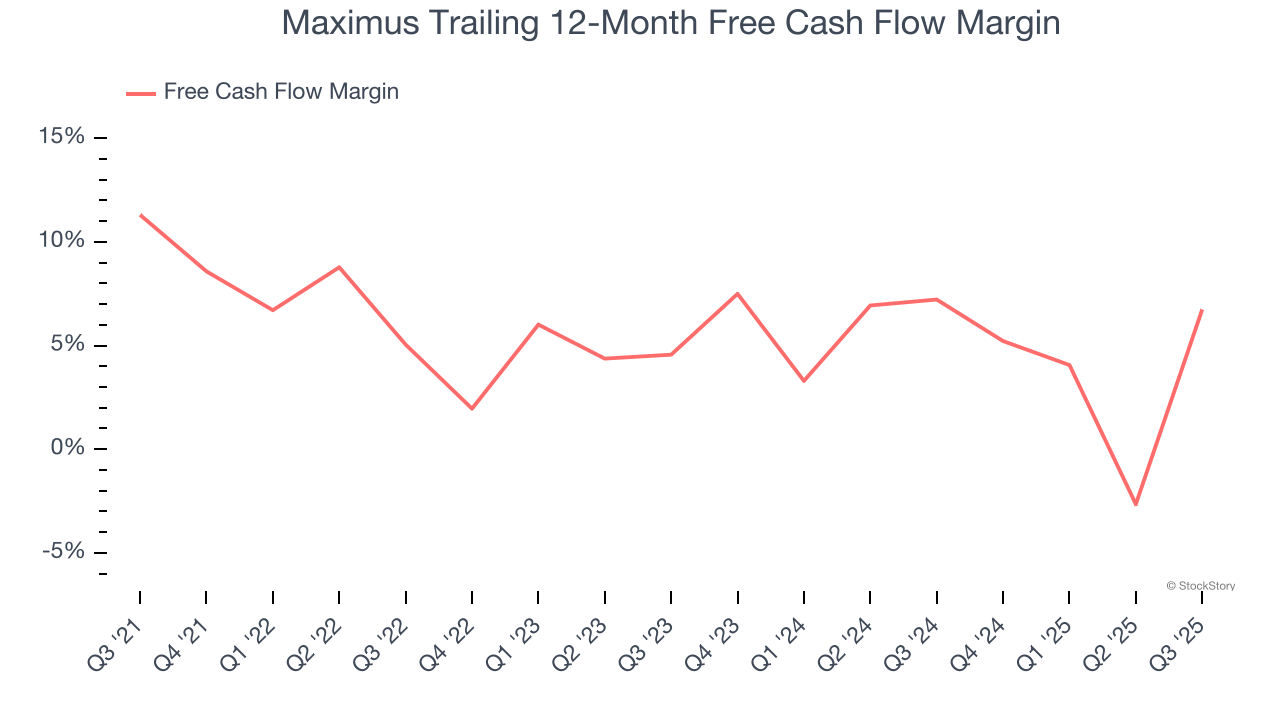

Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Maximus’s margin dropped by 4.6 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Maximus’s free cash flow margin for the trailing 12 months was 6.7%.

Final Judgment

Maximus has huge potential even though it has some open questions, and with its shares topping the market in recent months, the stock trades at 10.6× forward P/E (or $86.33 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free for active Edge members.

High-Quality Stocks for All Market Conditions

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.