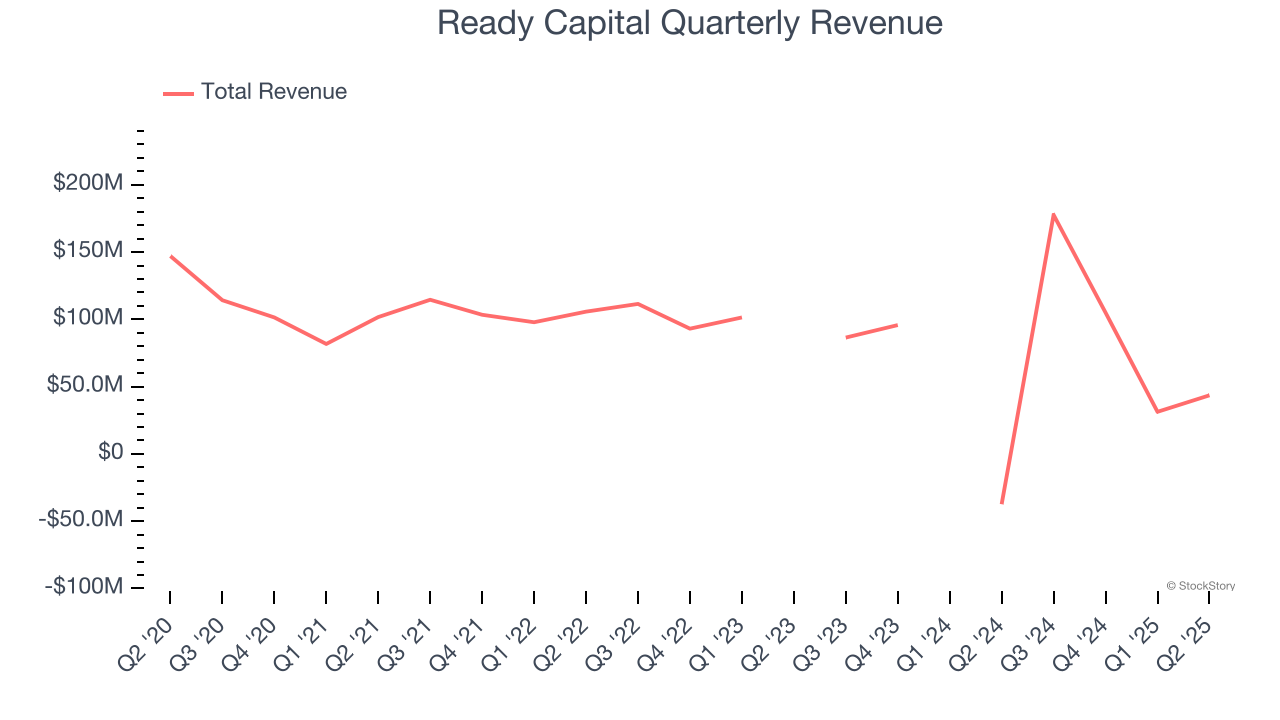

Real estate finance company Ready Capital (NYSE: RC) fell short of the market’s revenue expectations in Q2 CY2025, but sales rose 217% year on year to $43.57 million. Its GAAP loss of $0.14 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Ready Capital? Find out by accessing our full research report, it’s free.

Ready Capital (RC) Q2 CY2025 Highlights:

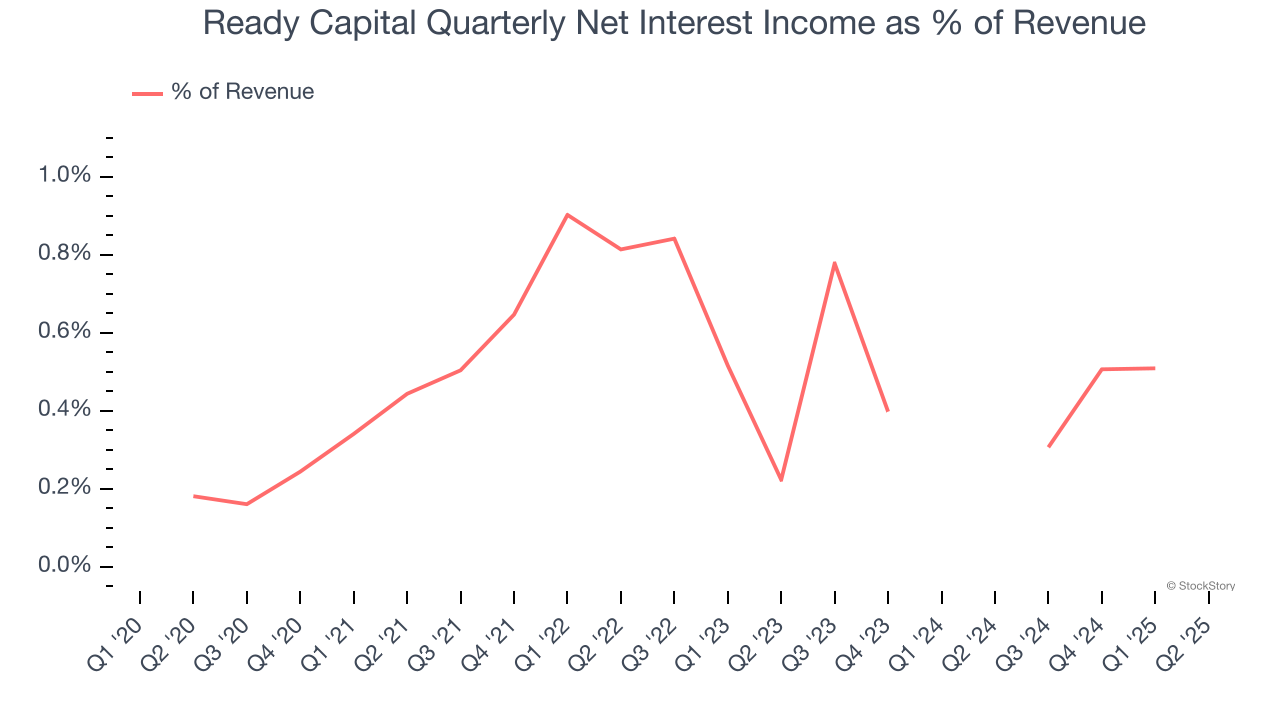

- Net Interest Income: $16.9 million vs analyst estimates of $53.73 million (3,479% year-on-year growth, 68.5% miss)

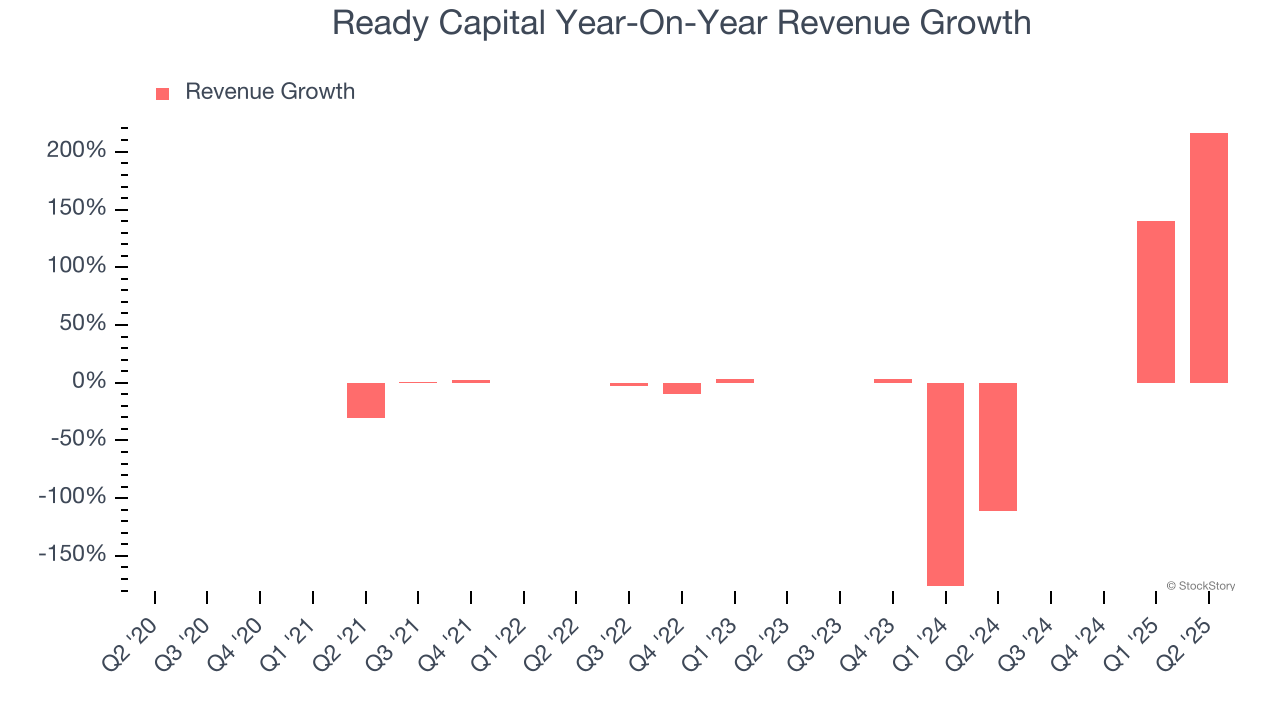

- Revenue: $43.57 million vs analyst estimates of $47.53 million (217% year-on-year growth, 8.3% miss)

- EPS (GAAP): -$0.14 vs analyst estimates of $0.05 (significant miss)

- Market Capitalization: $721.2 million

“As we begin to emerge from this CRE cycle, several items were completed since the first quarter which we believe will restore us to profitability”, said Thomas Capasse, Ready Capital’s Chairman and Chief Executive Officer.

Company Overview

Operating as one of only 17 non-bank Small Business Lending Companies with preferred lender status from the SBA, Ready Capital (NYSE: RC) is a multi-strategy real estate finance company that originates, acquires, and services commercial real estate loans, small business loans, and other real estate investments.

Sales Growth

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions.

Unfortunately, Ready Capital’s 1.2% annualized revenue growth over the last five years was tepid. This fell short of our benchmarks and is a poor baseline for our analysis.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Ready Capital’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 25.2% annually.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Ready Capital achieved a magnificent 217% year-on-year revenue growth rate, but its $43.57 million of revenue fell short of Wall Street’s lofty estimates.

Net interest income made up 2.4% of the company’s total revenue during the last five years, meaning Ready Capital is well diversified and has a variety of income streams driving its overall growth. Nevertheless, net interest income is critical to analyze for banks because they’re considered a higher-quality, more recurring revenue source by investors.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

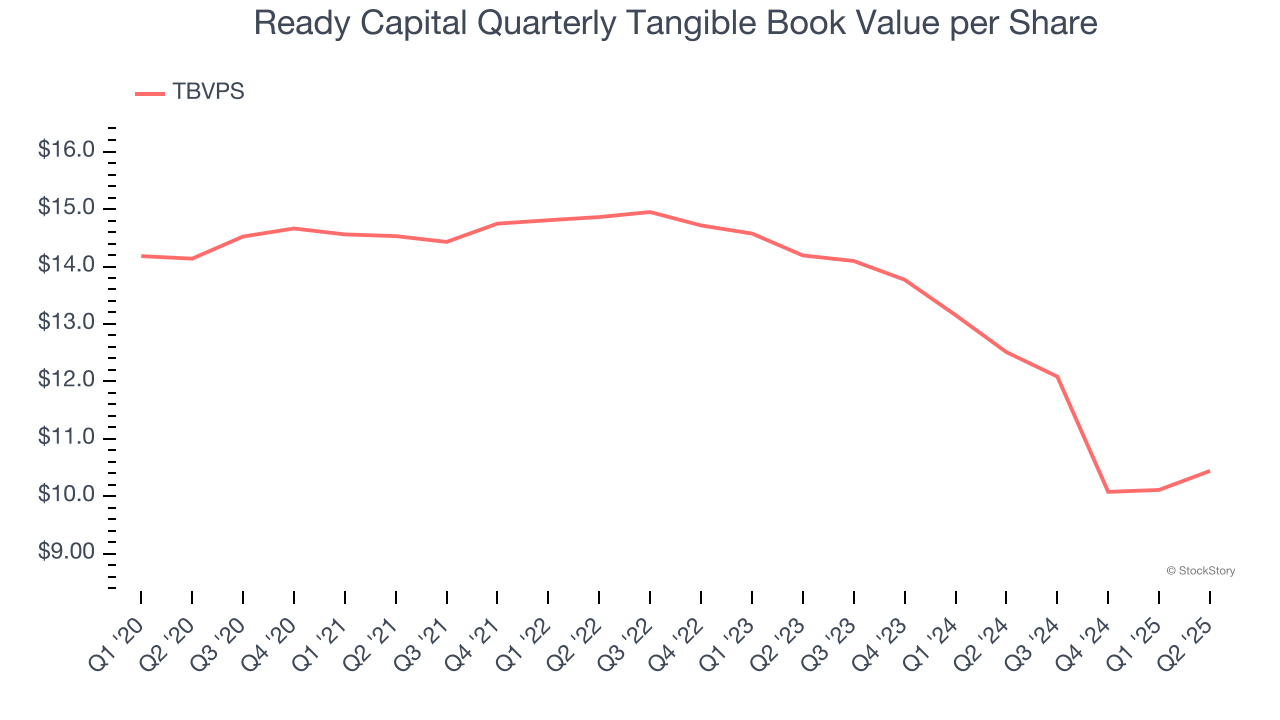

Tangible Book Value Per Share (TBVPS)

Banks profit by intermediating between depositors and borrowers, making them fundamentally balance sheet-driven enterprises. Market participants emphasize balance sheet quality and sustained book value growth when evaluating these institutions.

This explains why tangible book value per share (TBVPS) stands as the premier banking metric. TBVPS strips away questionable intangible assets, revealing concrete per-share net worth that investors can trust. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

Ready Capital’s TBVPS declined at a 5.9% annual clip over the last five years. A turnaround doesn’t seem to be in sight as its TBVPS also dropped by 14.2% annually over the last two years ($14.19 to $10.44 per share).

Over the next 12 months, Consensus estimates call for Ready Capital’s TBVPS to shrink by 1.2% to $10.31, a sour projection.

Key Takeaways from Ready Capital’s Q2 Results

We struggled to find many positives in these results. Its revenue missed and its net interest income fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2% to $4.16 immediately after reporting.

Ready Capital’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.