As the Q4 earnings season wraps, let’s dig into this quarter’s best and worst performers in the branded pharmaceuticals industry, including Pfizer (NYSE: PFE) and its peers.

The branded pharmaceutical industry relies on a high-cost, high-reward business model, driven by substantial investments in research and development to create innovative, patent-protected drugs. Successful products can generate significant revenue streams over their patent life, and the larger a roster of drugs, the stronger a moat a company enjoys. However, the business model is inherently risky, with high failure rates during clinical trials, lengthy regulatory approval processes, and intense competition from generic and biosimilar manufacturers once patents expire. These challenges, combined with scrutiny over drug pricing, create a complex operating environment. Looking ahead, the industry is positioned for tailwinds from advancements in precision medicine, increasing adoption of AI to enhance drug development efficiency, and growing global demand for treatments addressing chronic and rare diseases. However, headwinds include heightened regulatory scrutiny, pricing pressures from governments and insurers, and the looming patent cliffs for key blockbuster drugs. Patent cliffs bring about competition from generics, forcing branded pharmaceutical companies back to the drawing board to find the next big thing.

The 11 branded pharmaceuticals stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 1.3%.

While some branded pharmaceuticals stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.4% since the latest earnings results.

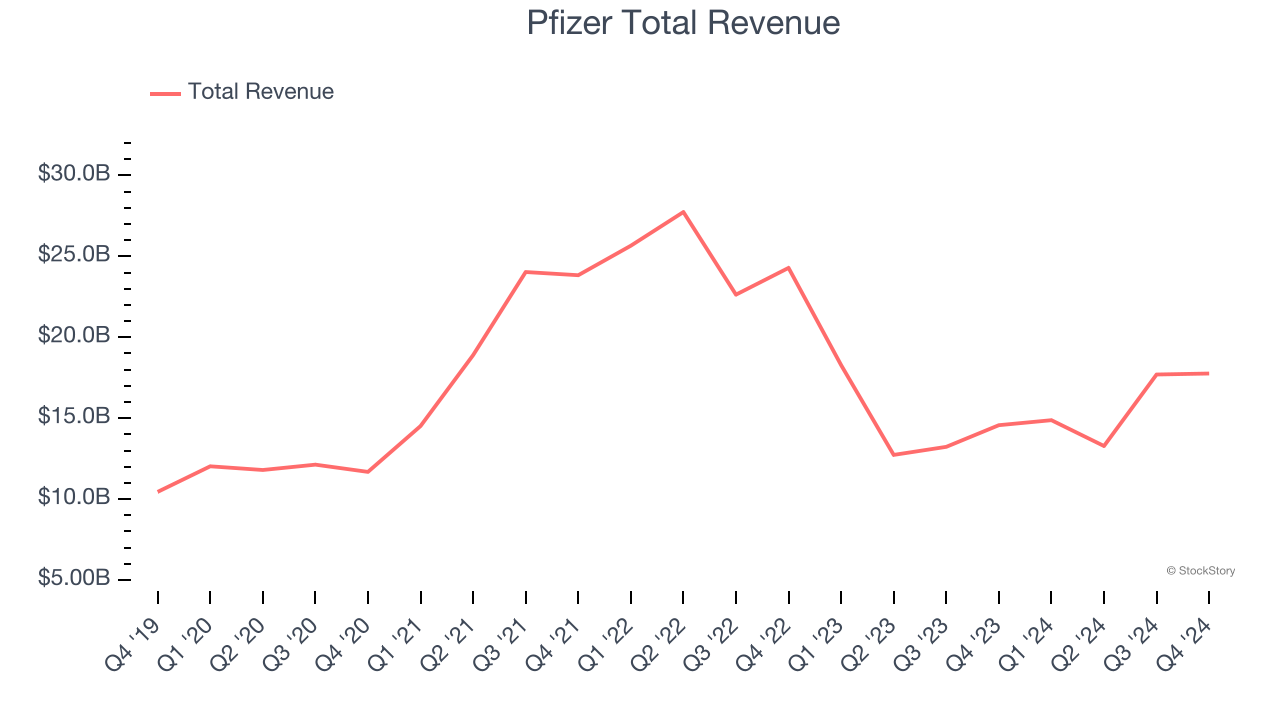

Pfizer (NYSE: PFE)

With roots dating back to 1849 when two German immigrants opened a fine chemicals business in Brooklyn, Pfizer (NYSE: PFE) is a global biopharmaceutical company that discovers, develops, manufactures, and sells medicines and vaccines for a wide range of diseases and conditions.

Pfizer reported revenues of $17.76 billion, up 21.9% year on year. This print exceeded analysts’ expectations by 3%. Overall, it was a strong quarter for the company with a solid beat of analysts’ organic revenue and EPS estimates.

The stock is down 3.8% since reporting and currently trades at $25.22.

Is now the time to buy Pfizer? Access our full analysis of the earnings results here, it’s free.

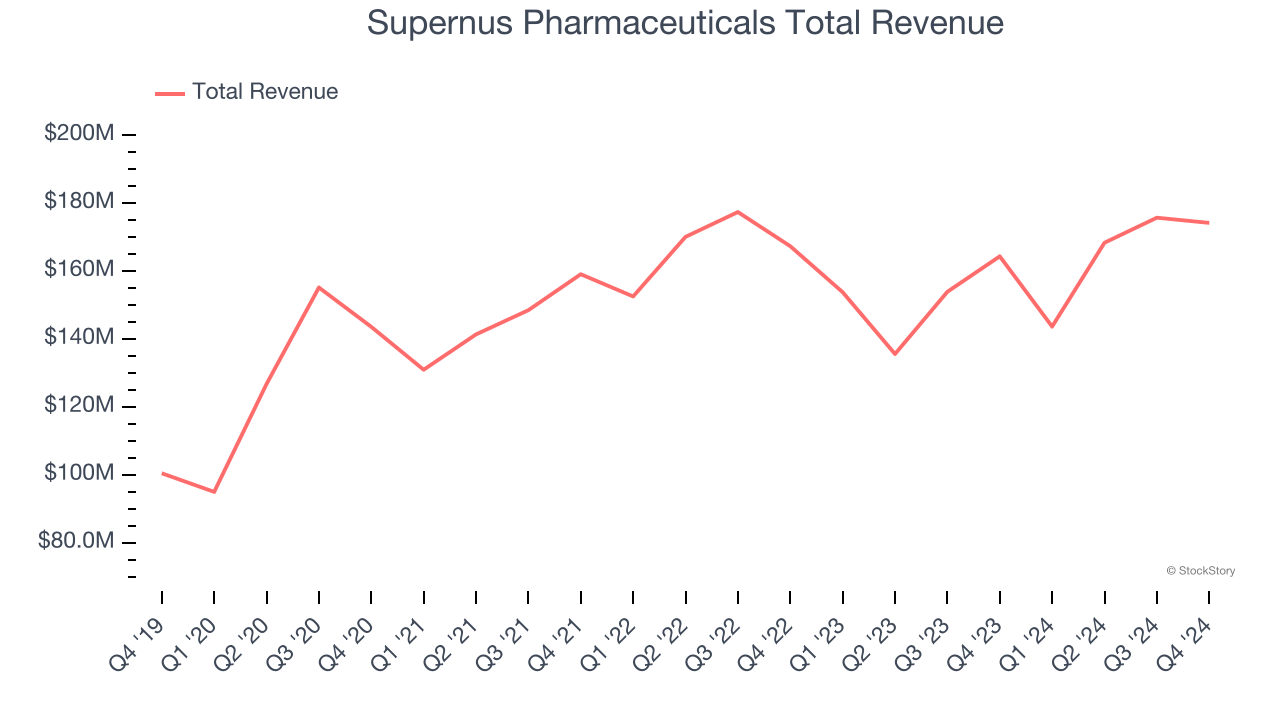

Best Q4: Supernus Pharmaceuticals (NASDAQ: SUPN)

With a diverse portfolio of eight FDA-approved medications targeting neurological conditions, Supernus Pharmaceuticals (NASDAQ: SUPN) develops and markets treatments for central nervous system disorders including epilepsy, ADHD, Parkinson's disease, and migraine.

Supernus Pharmaceuticals reported revenues of $174.2 million, up 6% year on year, outperforming analysts’ expectations by 12.2%. The business had a very strong quarter with an impressive beat of analysts’ EPS estimates and full-year operating income guidance topping analysts’ expectations.

Supernus Pharmaceuticals scored the biggest analyst estimates beat among its peers. However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $32.79.

Is now the time to buy Supernus Pharmaceuticals? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Zoetis (NYSE: ZTS)

Originally spun off from Pfizer in 2013 as the world's largest pure-play animal health company, Zoetis (NYSE: ZTS) discovers, develops, and sells medicines, vaccines, diagnostic products, and services for pets and livestock animals worldwide.

Zoetis reported revenues of $2.32 billion, up 4.7% year on year, in line with analysts’ expectations. It was a softer quarter as it posted a significant miss of analysts’ full-year EPS guidance estimates.

As expected, the stock is down 7.1% since the results and currently trades at $161.61.

Read our full analysis of Zoetis’s results here.

Bristol-Myers Squibb (NYSE: BMY)

With roots dating back to 1887 and a transformative merger in 1989 that gave the company its current name, Bristol-Myers Squibb (NYSE: BMY) discovers, develops, and markets prescription medications for serious diseases including cancer, blood disorders, immunological conditions, and cardiovascular diseases.

Bristol-Myers Squibb reported revenues of $12.34 billion, up 7.5% year on year. This print surpassed analysts’ expectations by 6.6%. Zooming out, it was a mixed quarter as it also produced an impressive beat of analysts’ EPS estimates but a significant miss of analysts’ full-year EPS guidance estimates.

The stock is flat since reporting and currently trades at $59.20.

Read our full, actionable report on Bristol-Myers Squibb here, it’s free.

Organon (NYSE: OGN)

Spun off from Merck in 2021 to create a company dedicated to addressing unmet needs in women's health, Organon (NYSE: OGN) is a global healthcare company focused on improving women's health through prescription therapies, medical devices, biosimilars, and established medicines.

Organon reported revenues of $1.59 billion, flat year on year. This number topped analysts’ expectations by 0.9%. However, it was a slower quarter as it logged full-year revenue guidance missing analysts’ expectations significantly.

Organon had the slowest revenue growth among its peers. The stock is flat since reporting and currently trades at $14.80.

Read our full, actionable report on Organon here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.