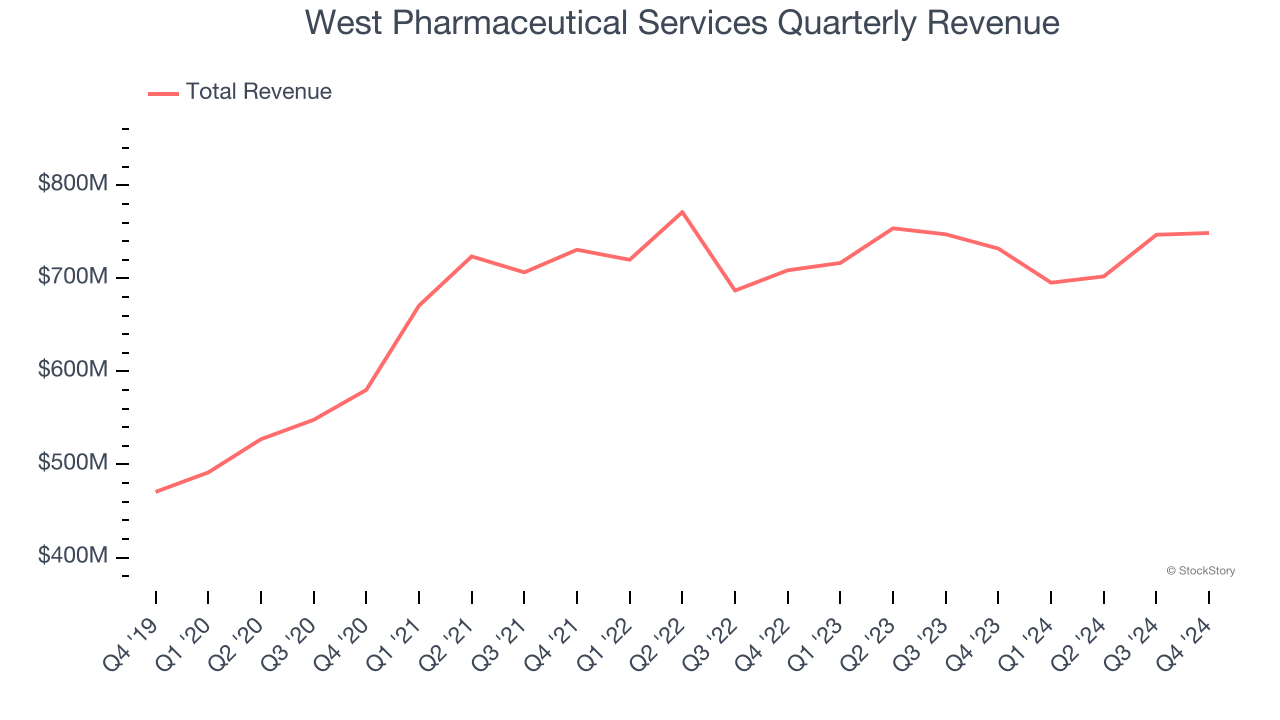

Healthcare products company West Pharmaceutical Services (NYSE: WST) reported Q4 CY2024 results topping the market’s revenue expectations, with sales up 2.3% year on year to $748.8 million. On the other hand, the company’s full-year revenue guidance of $2.89 billion at the midpoint came in 5% below analysts’ estimates. Its non-GAAP profit of $1.82 per share was 5.3% above analysts’ consensus estimates.

Is now the time to buy West Pharmaceutical Services? Find out by accessing our full research report, it’s free.

West Pharmaceutical Services (WST) Q4 CY2024 Highlights:

- Revenue: $748.8 million vs analyst estimates of $740.2 million (2.3% year-on-year growth, 1.2% beat)

- Adjusted EPS: $1.82 vs analyst estimates of $1.73 (5.3% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $2.89 billion at the midpoint, missing analyst estimates by 5% and implying -0.1% growth (vs -1.9% in FY2024)

- Adjusted EPS guidance for the upcoming financial year 2025 is $6.10 at the midpoint, missing analyst estimates by 17.8%

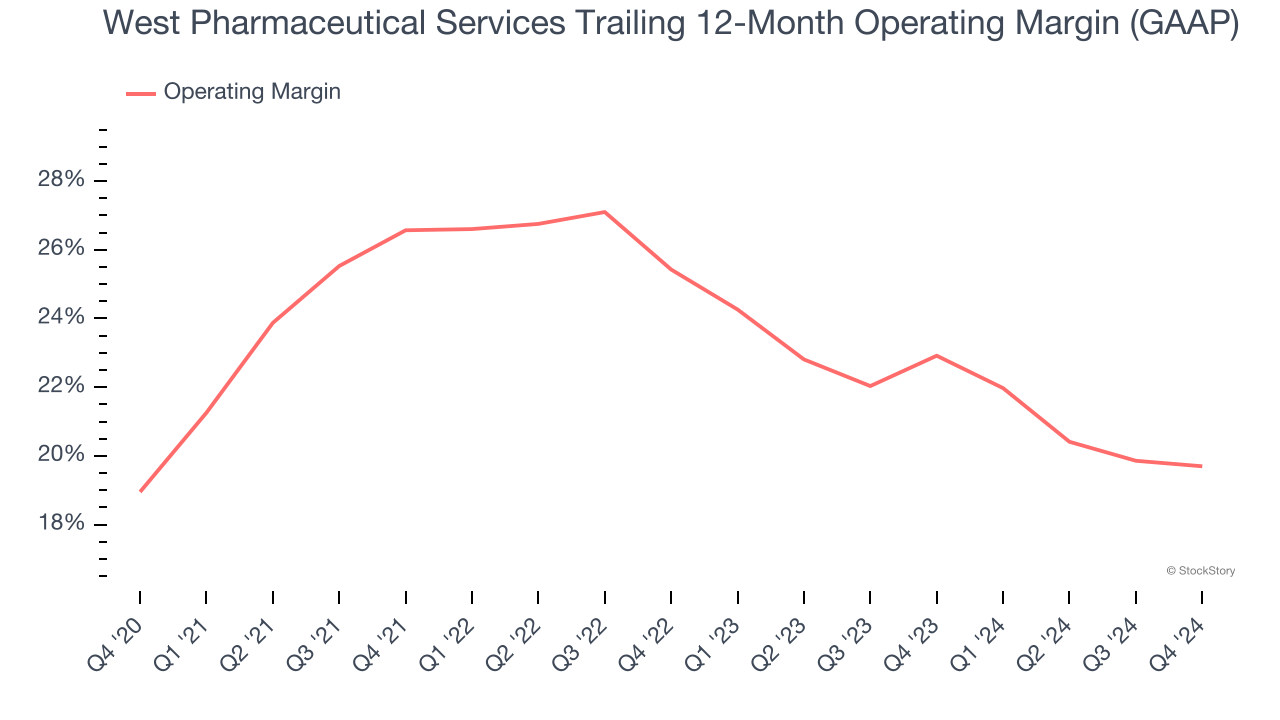

- Operating Margin: 21.3%, in line with the same quarter last year

- Market Capitalization: $23.34 billion

Company Overview

Founded in 1923, West Pharmaceutical Services (NYSE: WST) develops innovative injectable drug packaging and delivery solutions, focusing on safe and effective medication containment.

Drug Development Inputs & Services

Companies specializing in drug development inputs and services play a crucial role in the pharmaceutical and biotechnology value chain. Essential support for drug discovery, preclinical testing, and manufacturing means stable demand, as pharmaceutical companies often outsource non-core functions with medium to long-term contracts. However, the business model faces high capital requirements, customer concentration, and vulnerability to shifts in biopharma R&D budgets or regulatory frameworks. Looking ahead, the industry will likely enjoy tailwinds such as increasing investment in biologics, cell and gene therapies, and advancements in precision medicine, which drive demand for sophisticated tools and services. There is a growing trend of outsourcing in drug development for nimbleness and cost efficiency, which benefits the industry. On the flip side, potential headwinds include pricing pressures as efforts to contain healthcare costs are always top of mind. An evolving regulatory backdrop could also slow innovation or client activity.

Sales Growth

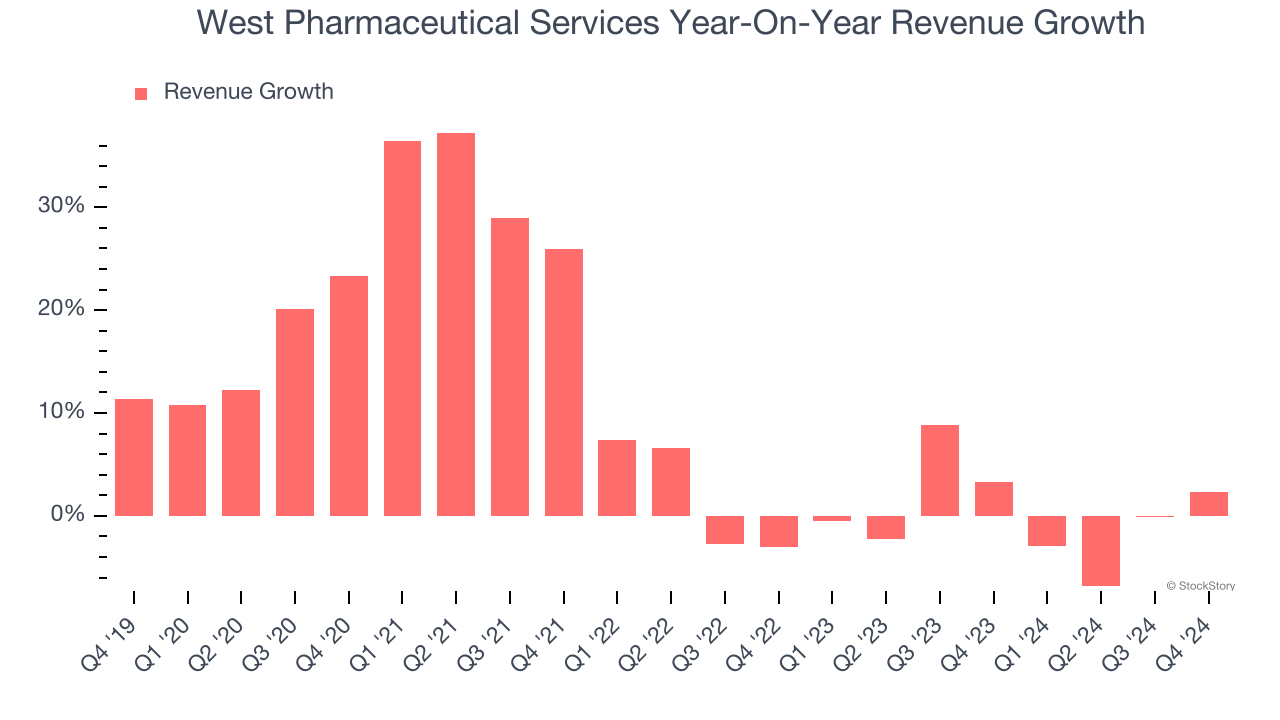

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, West Pharmaceutical Services grew its sales at a decent 9.5% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. West Pharmaceutical Services’s recent history shows its demand slowed as its revenue was flat over the last two years.

This quarter, West Pharmaceutical Services reported modest year-on-year revenue growth of 2.3% but beat Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to grow 5% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and implies its newer products and services will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

West Pharmaceutical Services has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 22.9%.

Analyzing the trend in its profitability, West Pharmaceutical Services’s operating margin of 19.7% for the trailing 12 months may be around the same as five years ago, but it has decreased by 5.7 percentage points over the last two years. This dynamic unfolded because it struggled to adjust its fixed costs while its demand plateaued.

This quarter, West Pharmaceutical Services generated an operating profit margin of 21.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

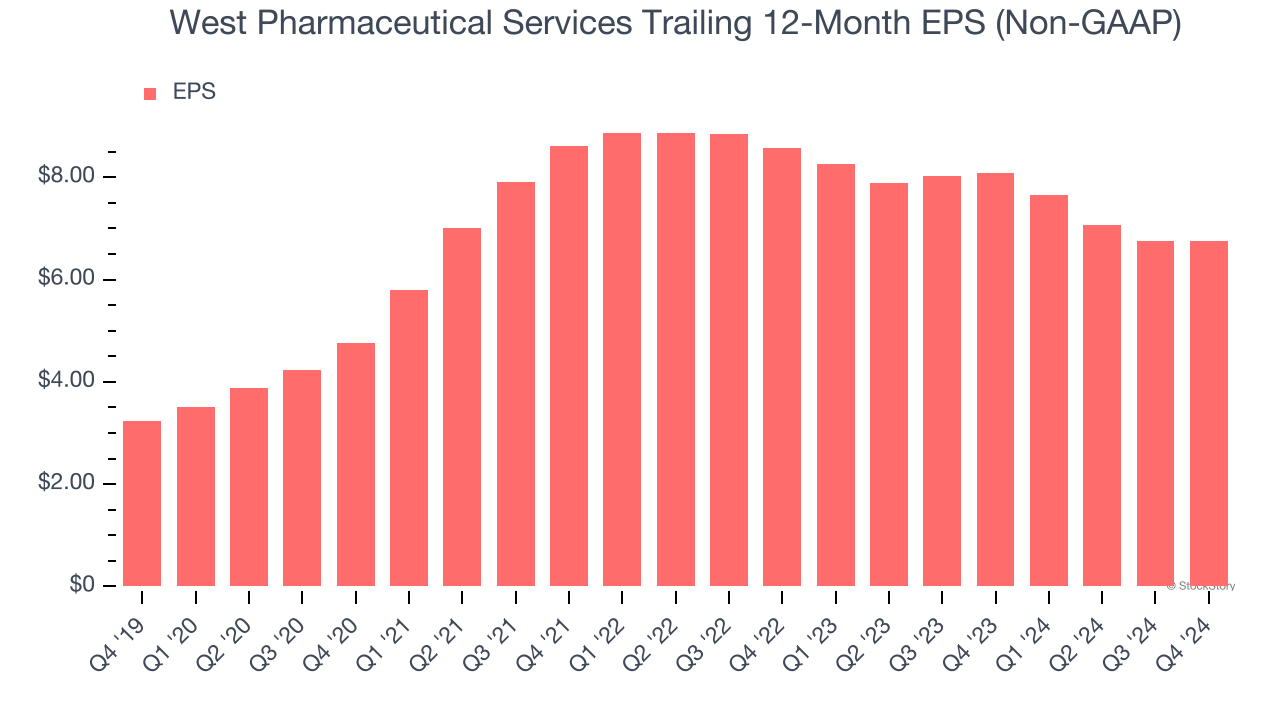

West Pharmaceutical Services’s EPS grew at an astounding 15.8% compounded annual growth rate over the last five years, higher than its 9.5% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t expand.

Diving into the nuances of West Pharmaceutical Services’s earnings can give us a better understanding of its performance. A five-year view shows that West Pharmaceutical Services has repurchased its stock, shrinking its share count by 3.2%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, West Pharmaceutical Services reported EPS at $1.82, down from $1.83 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 5.3%. Over the next 12 months, Wall Street expects West Pharmaceutical Services’s full-year EPS of $6.75 to grow 9.1%.

Key Takeaways from West Pharmaceutical Services’s Q4 Results

It was good to see West Pharmaceutical Services narrowly top analysts’ revenue expectations this quarter. On the other hand, its full-year revenue guidance missed significantly and its full-year EPS guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 8.3% to $296 immediately following the results.

The latest quarter from West Pharmaceutical Services’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.