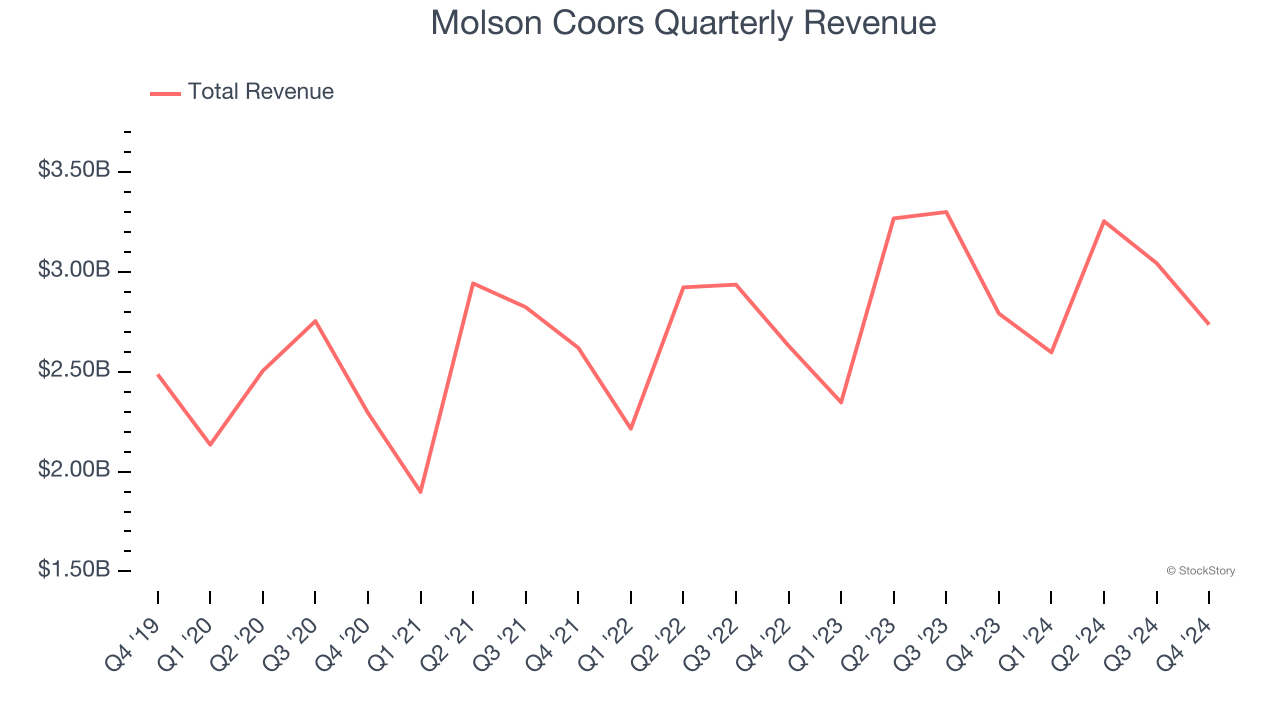

Beer company Molson Coors (NYSE: TAP) reported Q4 CY2024 results beating Wall Street’s revenue expectations, but sales fell by 2% year on year to $2.74 billion. Its non-GAAP profit of $1.30 per share was 15.3% above analysts’ consensus estimates.

Is now the time to buy Molson Coors? Find out by accessing our full research report, it’s free.

Molson Coors (TAP) Q4 CY2024 Highlights:

- Revenue: $2.74 billion vs analyst estimates of $2.71 billion (2% year-on-year decline, 1.1% beat)

- Adjusted EPS: $1.30 vs analyst estimates of $1.13 (15.3% beat)

- Adjusted EBITDA: $558.5 million vs analyst estimates of $549.7 million (20.4% margin, 1.6% beat)

- Operating Margin: 14.2%, up from 7.1% in the same quarter last year

- Free Cash Flow Margin: 14%, up from 10.8% in the same quarter last year

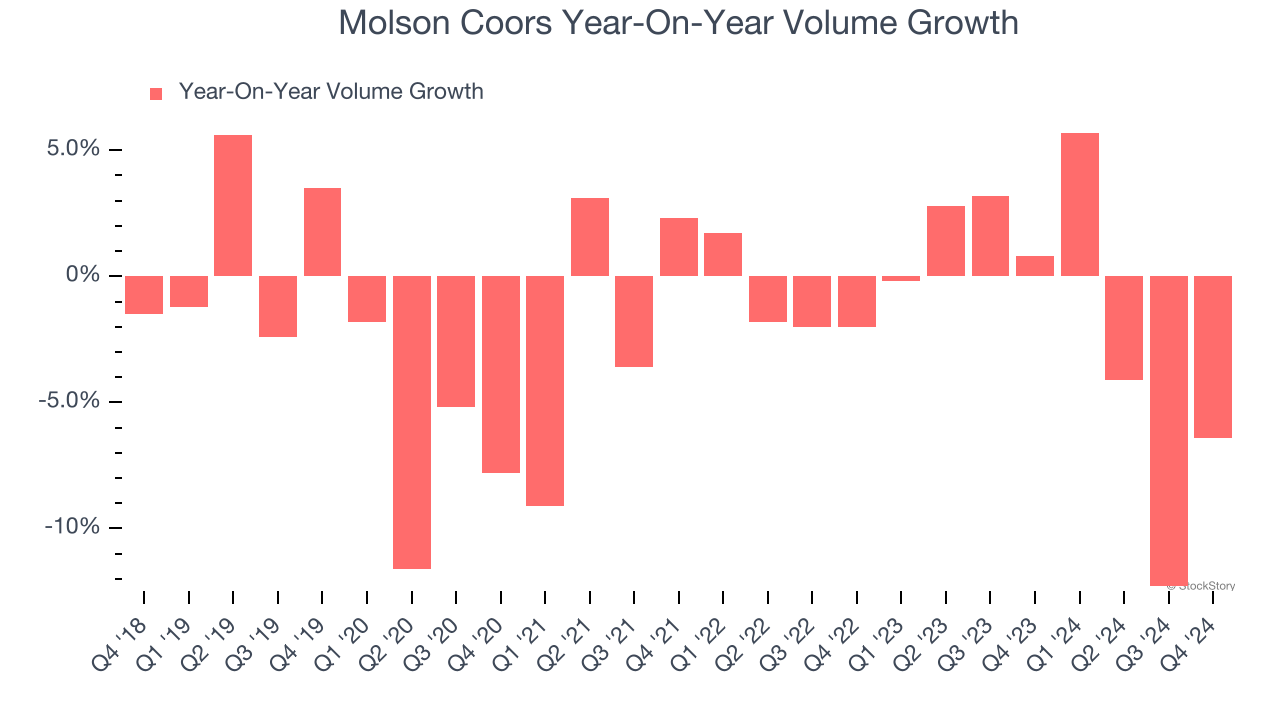

- Sales Volumes fell 6.4% year on year (0.8% in the same quarter last year)

- Market Capitalization: $11.01 billion

Company Overview

Sporting an impressive roster of iconic beer brands, Molson Coors (NYSE: TAP) is a global brewing giant with a rich history dating back more than two centuries.

Beverages, Alcohol, and Tobacco

These companies' performance is influenced by brand strength, marketing strategies, and shifts in consumer preferences. Changing consumption patterns are particularly relevant and can be seen in the rise of cannabis, craft beer, and vaping or the steady decline of soda and cigarettes. Companies that spend on innovation to meet consumers where they are with regards to trends can reap huge demand benefits while those who ignore trends can see stagnant volumes. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

Sales Growth

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $11.63 billion in revenue over the past 12 months, Molson Coors is one of the larger consumer staples companies and benefits from a well-known brand that influences consumer purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. To accelerate sales, Molson Coors must lean into newer products.

As you can see below, Molson Coors grew its sales at a sluggish 4.2% compounded annual growth rate over the last three years as consumers bought less of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, Molson Coors’s revenue fell by 2% year on year to $2.74 billion but beat Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and indicates its products will face some demand challenges.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Molson Coors’s average quarterly sales volumes have shrunk by 1.3% over the last two years. This decrease isn’t ideal because the quantity demanded for consumer staples products is typically stable.

In Molson Coors’s Q4 2024, sales volumes dropped 6.4% year on year. This result represents a further deceleration from its historical levels, showing the business is struggling to move its products.

Key Takeaways from Molson Coors’s Q4 Results

It was encouraging to see Molson Coors beat analysts’ EPS expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Overall, this quarter had some key positives. The stock traded up 5.1% to $56.20 immediately after reporting.

Sure, Molson Coors had a solid quarter, but if we look at the bigger picture, is this stock a buy? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.