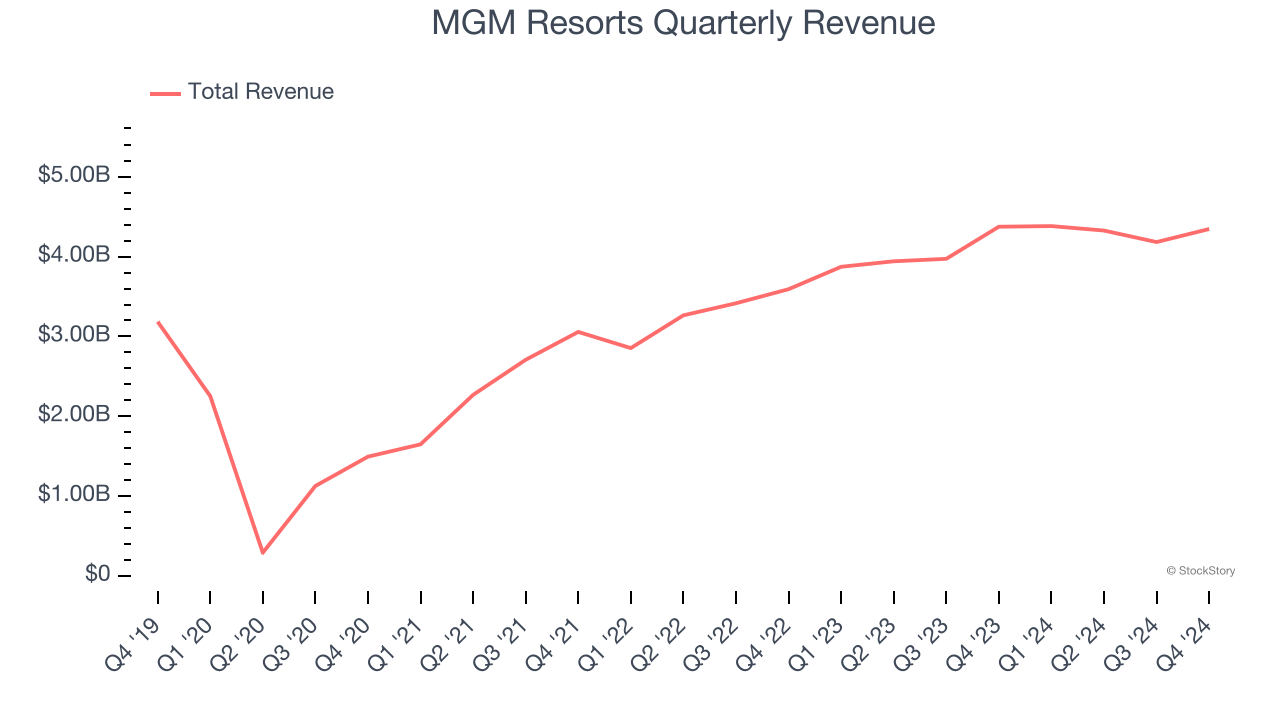

Hospitality and casino entertainment company MGM Resorts (NYSE: MGM) reported Q4 CY2024 results exceeding the market’s revenue expectations, but sales were flat year on year at $4.35 billion. Its non-GAAP profit of $0.45 per share was 33% above analysts’ consensus estimates.

Is now the time to buy MGM Resorts? Find out by accessing our full research report, it’s free.

MGM Resorts (MGM) Q4 CY2024 Highlights:

- Revenue: $4.35 billion vs analyst estimates of $4.29 billion (flat year on year, 1.3% beat)

- Adjusted EPS: $0.45 vs analyst estimates of $0.34 (33% beat)

- Adjusted EBITDA: $528.5 million vs analyst estimates of $1.08 billion (12.2% margin, 51.3% miss)

- Operating Margin: 6.7%, down from 9.6% in the same quarter last year

- Market Capitalization: $10.2 billion

"MGM Resorts is proud to report the best full-year consolidated net revenues in the history of the Company, driven by record performance from MGM China," said Bill Hornbuckle, Chief Executive Officer & President of MGM Resorts International.

Company Overview

Operating several properties on the Las Vegas Strip, MGM Resorts (NYSE: MGM) is a global hospitality and entertainment company known for its resorts and casinos.

Casino Operator

Casino operators enjoy limited competition because gambling is a highly regulated industry. These companies can also enjoy healthy margins and profits. Have you ever heard the phrase ‘the house always wins’? Regulation cuts both ways, however, and casinos may face stroke-of-the-pen risk that suddenly limits what they can or can't do and where they can do it. Furthermore, digitization is changing the game, pun intended. Whether it’s online poker or sports betting on your smartphone, innovation is forcing these players to adapt to changing consumer preferences, such as being able to wager anywhere on demand.

Sales Growth

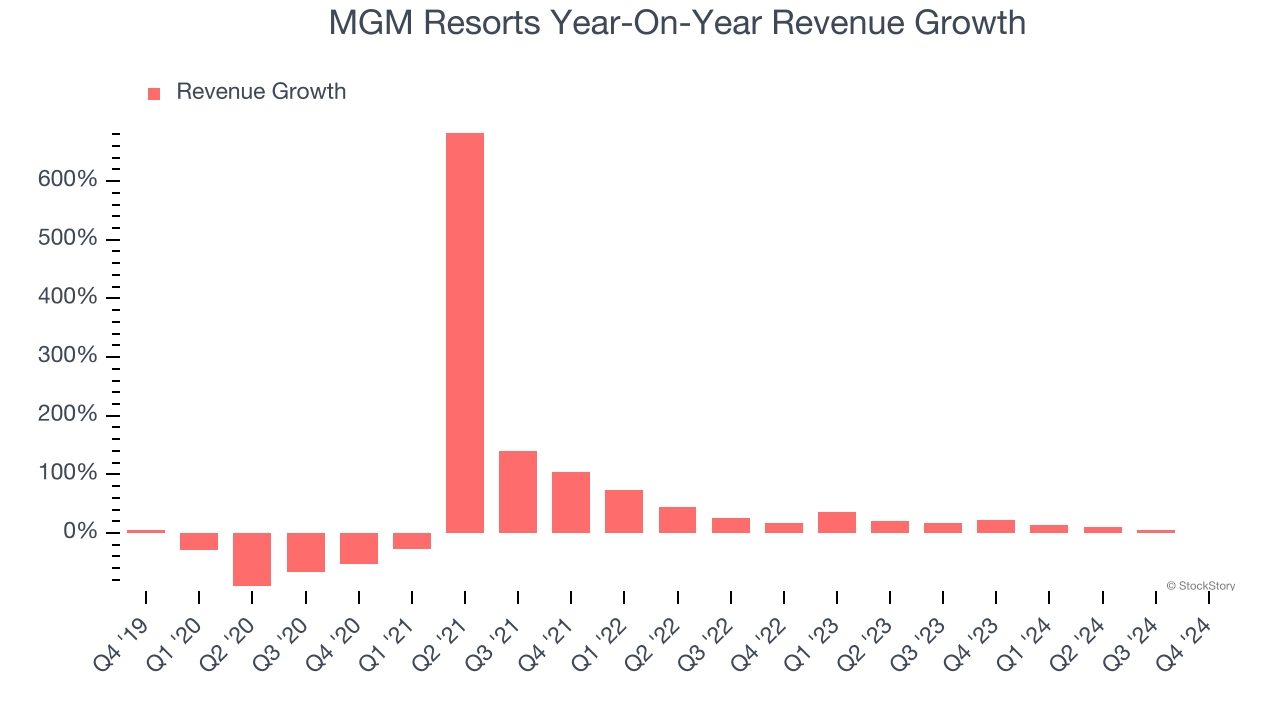

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, MGM Resorts grew its sales at a sluggish 6% compounded annual growth rate. This fell short of our benchmark for the consumer discretionary sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. MGM Resorts’s annualized revenue growth of 14.6% over the last two years is above its five-year trend, but we were still disappointed by the results. Note that COVID hurt MGM Resorts’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

We can dig further into the company’s revenue dynamics by analyzing its three most important segments: Casino, Hotel, and Dining, which are 50.9%, 21.7%, and 17.3% of revenue. Over the last two years, MGM Resorts’s revenues in all three segments increased. Its Casino revenue (Poker, sports betting) averaged year-on-year growth of 25.1% while its Hotel (overnight bookings) and Dining (food and beverage) revenues averaged 11.6% and 10.1%.

This quarter, MGM Resorts’s $4.35 billion of revenue was flat year on year but beat Wall Street’s estimates by 1.3%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Cash Is King

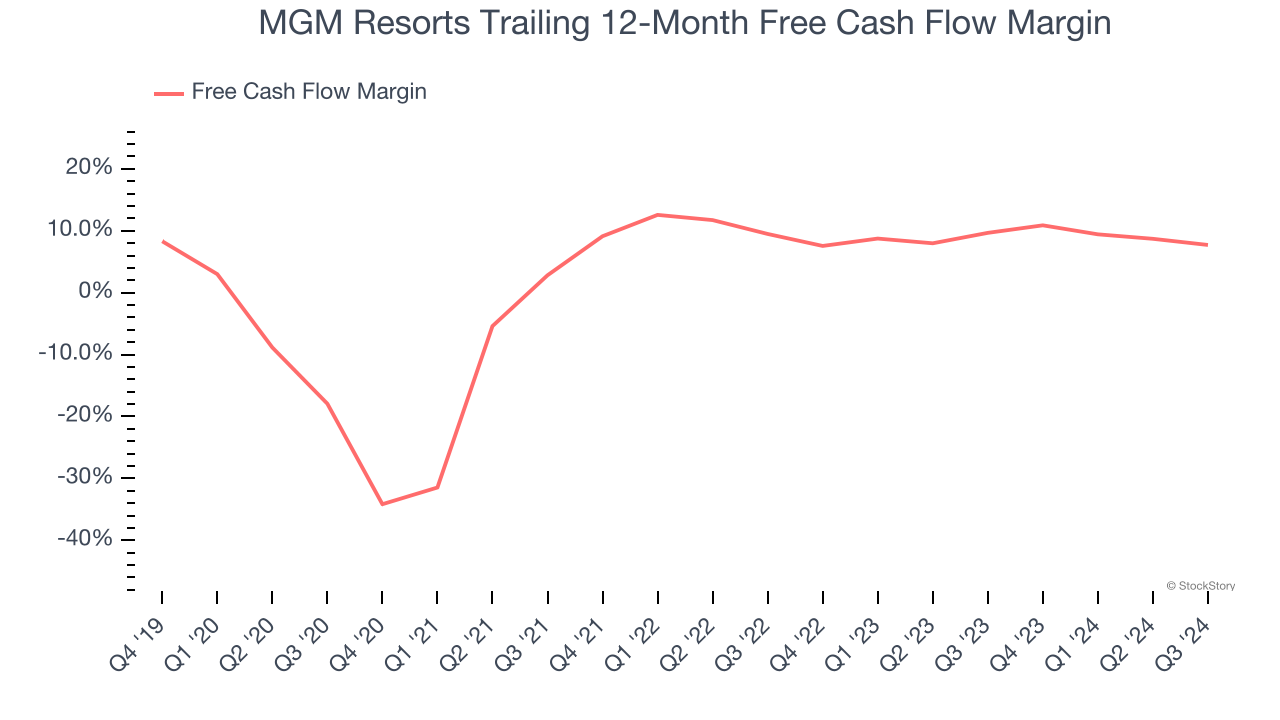

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

MGM Resorts has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 9.3%, subpar for a consumer discretionary business.

Key Takeaways from MGM Resorts’s Q4 Results

We were impressed by how significantly MGM Resorts blew past analysts’ EPS expectations this quarter on a small revenue beat. Zooming out, we think this was a solid quarter. The stock traded up 8.4% to $37.25 immediately after reporting.

Is MGM Resorts an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.