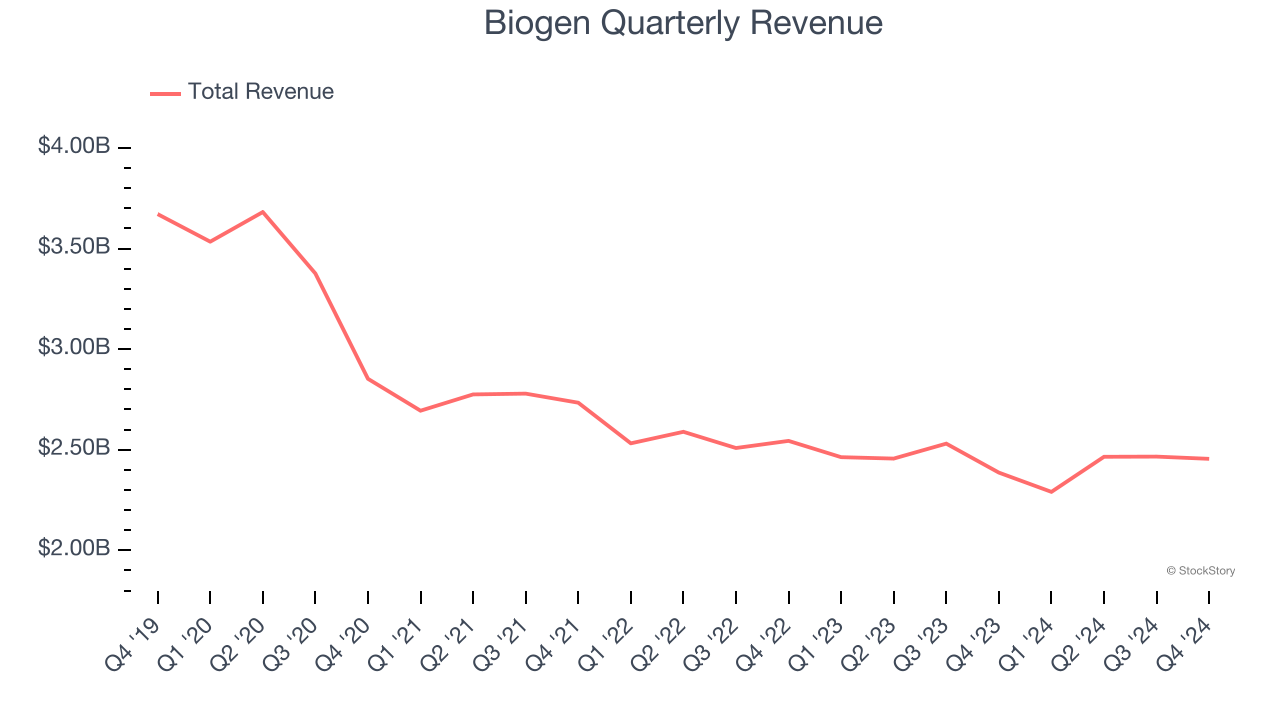

Biotech company Biogen (NASDAQ: BIIB) reported revenue ahead of Wall Street’s expectations in Q4 CY2024, with sales up 2.9% year on year to $2.45 billion. Its non-GAAP profit of $3.44 per share was 2.3% above analysts’ consensus estimates.

Is now the time to buy Biogen? Find out by accessing our full research report, it’s free.

Biogen (BIIB) Q4 CY2024 Highlights:

- Revenue: $2.45 billion vs analyst estimates of $2.41 billion (2.9% year-on-year growth, 1.8% beat)

- Adjusted EPS: $3.44 vs analyst estimates of $3.36 (2.3% beat)

- Adjusted EPS guidance for the upcoming financial year 2025 is $15.73 at the midpoint, missing analyst estimates by 3.1%

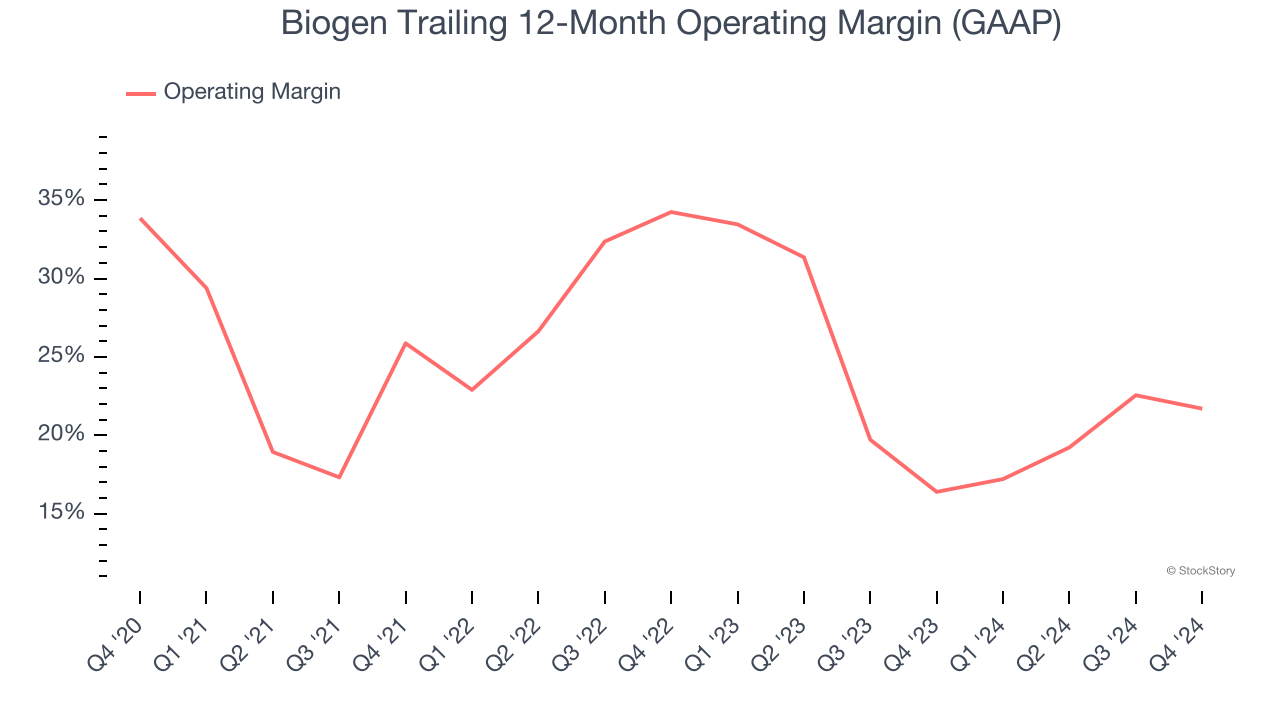

- Operating Margin: 11.9%, down from 15% in the same quarter last year

- Free Cash Flow was $800.2 million, up from -$52.7 million in the same quarter last year

- Market Capitalization: $20.31 billion

Company Overview

Founded in 1978 in Switzerland as one of the first biotech companies, Biogen today (NASDAQ: BIIB) discovers, develops, and sells therapies for neurological and neurodegenerative diseases like multiple sclerosis (MS) and Alzheimer’s disease.

Therapeutics

Over the next few years, therapeutic companies, which develop a wide variety of treatments for diseases and disorders, face strong tailwinds from advancements in precision medicine (including the use of AI to improve hit rates) and growing demand for treatments targeting rare diseases. However, headwinds such as rising scrutiny over drug pricing, regulatory unknowns, and competition from larger, more resourced pharmaceutical companies could weigh on growth.

Sales Growth

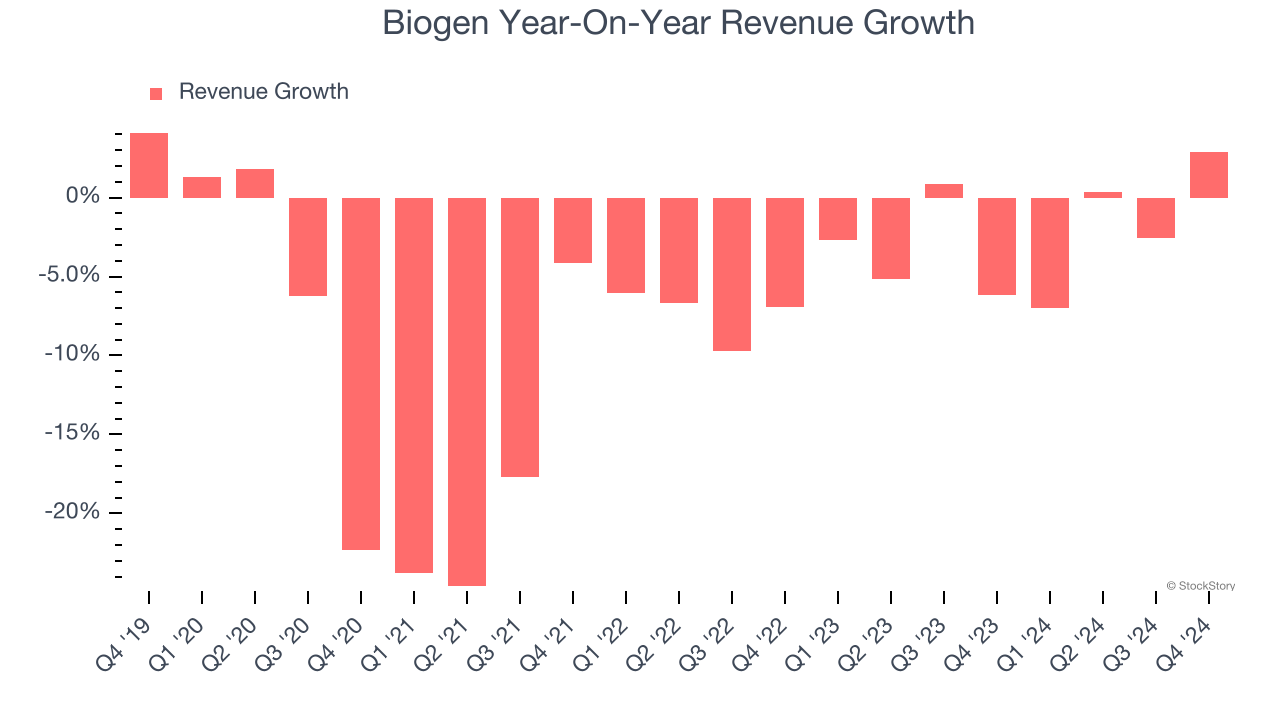

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Biogen’s demand was weak over the last five years as its sales fell at a 7.6% annual rate. This was below our standards and signals it’s a low quality business.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Biogen’s annualized revenue declines of 2.5% over the last two years suggest its demand continued shrinking.

This quarter, Biogen reported modest year-on-year revenue growth of 2.9% but beat Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to decline by 3.5% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its products and services will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Biogen has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 27%.

Looking at the trend in its profitability, Biogen’s operating margin decreased by 12.1 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 12.5 percentage points. This performance was poor no matter how you look at it - it shows operating expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Biogen generated an operating profit margin of 11.9%, down 3.2 percentage points year on year. This contraction shows it was recently less efficient because its expenses grew faster than its revenue.

Earnings Per Share

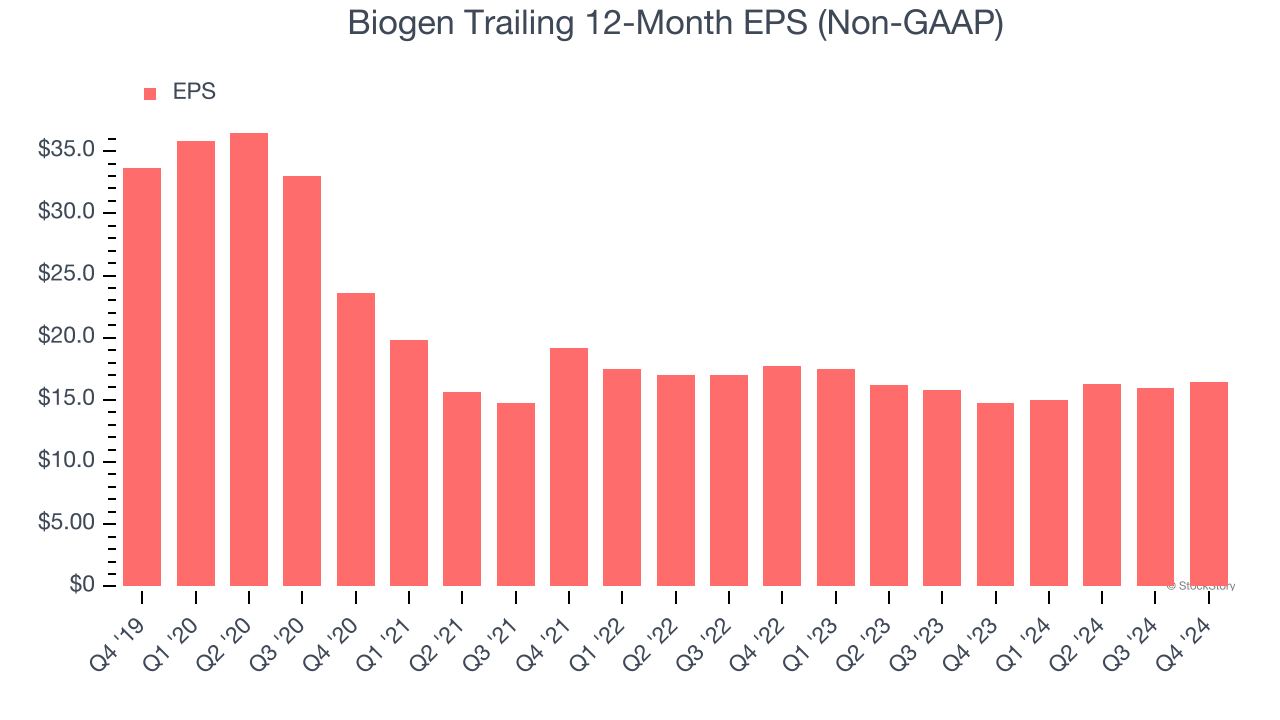

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Biogen, its EPS declined by more than its revenue over the last five years, dropping 13.3% annually. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

We can take a deeper look into Biogen’s earnings to better understand the drivers of its performance. As we mentioned earlier, Biogen’s operating margin declined by 12.1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Biogen reported EPS at $3.44, up from $2.95 in the same quarter last year. This print beat analysts’ estimates by 2.3%. Over the next 12 months, Wall Street expects Biogen’s full-year EPS of $16.47 to shrink by 1.9%.

Key Takeaways from Biogen’s Q4 Results

It was encouraging to see Biogen beat analysts’ revenue expectations this quarter. On the other hand, its full-year EPS guidance missed significantly and its EPS was in line with Wall Street’s estimates. Overall, this quarter was mixed. The stock remained flat at $139.70 immediately after reporting.

So should you invest in Biogen right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.