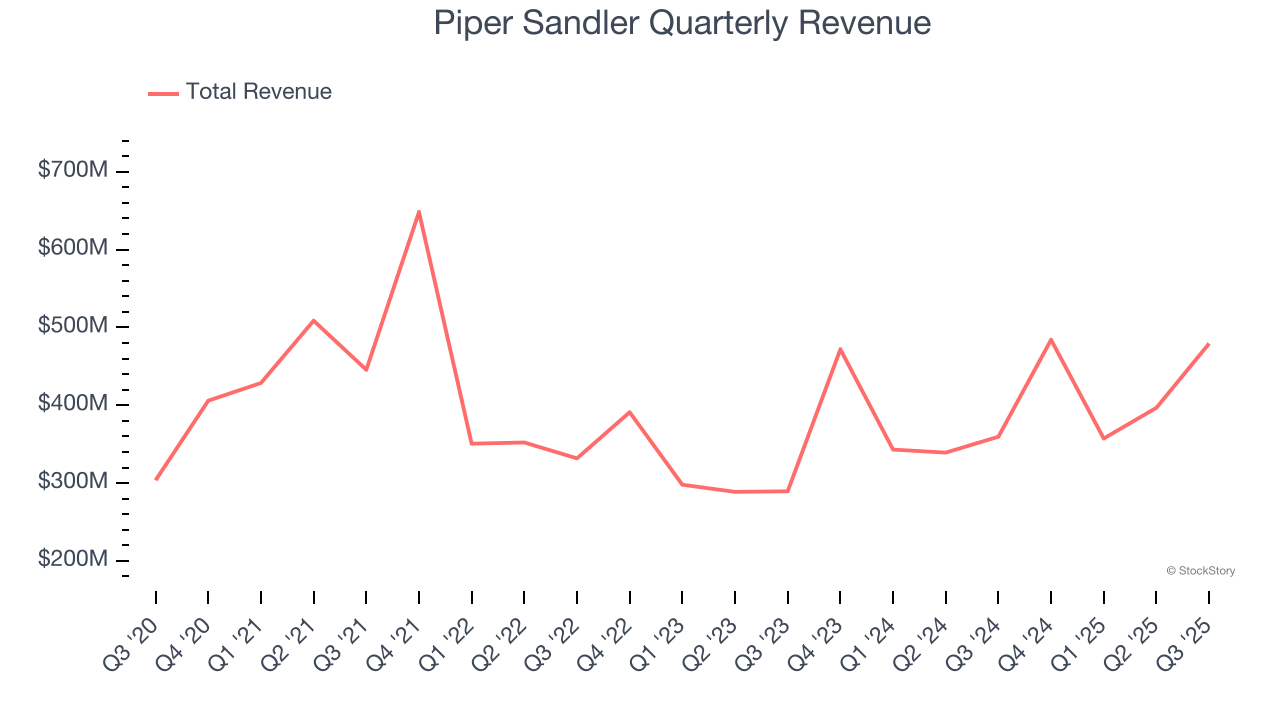

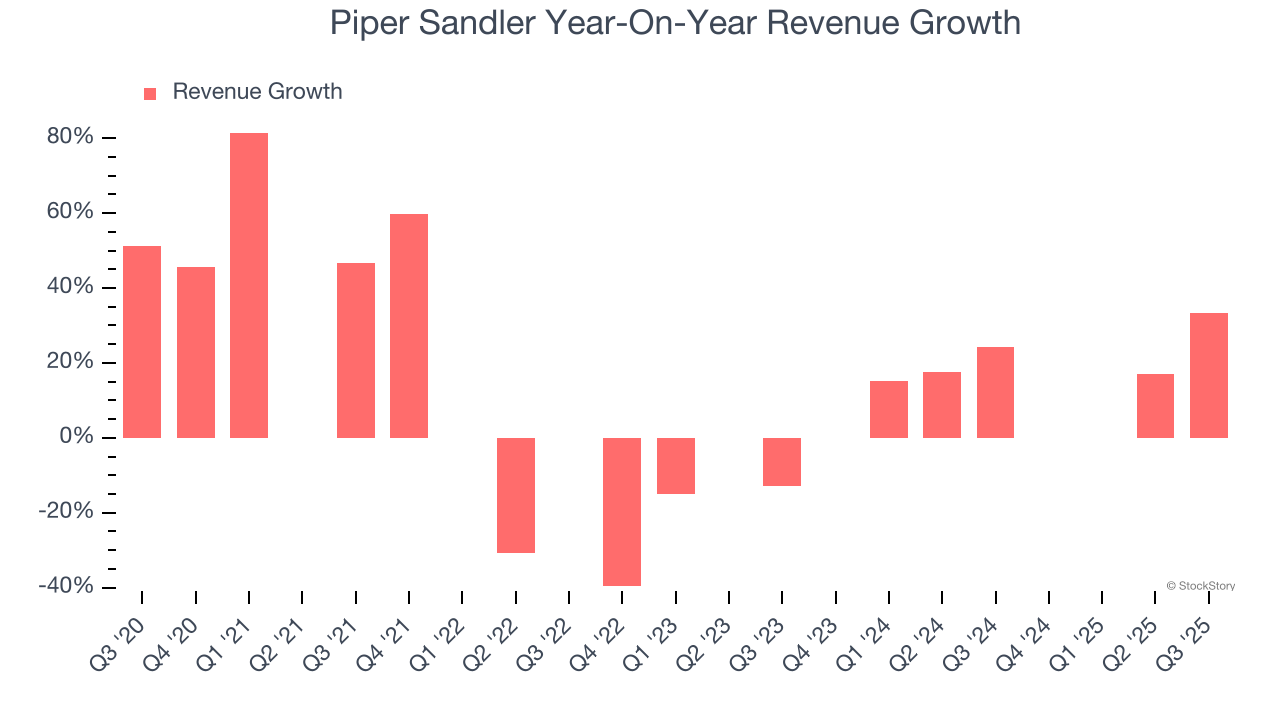

Investment banking firm Piper Sandler (NYSE: PIPR) reported revenue ahead of Wall Streets expectations in Q3 CY2025, with sales up 33.3% year on year to $479.3 million. Its non-GAAP profit of $3.82 per share was 16.7% above analysts’ consensus estimates.

Is now the time to buy Piper Sandler? Find out by accessing our full research report, it’s free for active Edge members.

Piper Sandler (PIPR) Q3 CY2025 Highlights:

- Revenue: $479.3 million vs analyst estimates of $436.7 million (33.3% year-on-year growth, 9.8% beat)

- Pre-tax Profit: $107.4 million (22.4% margin, 93.2% year-on-year growth)

- Adjusted EPS: $3.82 vs analyst estimates of $3.27 (16.7% beat)

- Market Capitalization: $5.79 billion

Company Overview

Tracing its roots back to 1895 and rebranded from Piper Jaffray in 2020, Piper Sandler (NYSE: PIPR) is an investment bank that provides advisory services, capital raising, institutional brokerage, and research for corporations, governments, and institutional investors.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Piper Sandler’s revenue grew at a decent 9.1% compounded annual growth rate over the last five years. Its growth was slightly above the average financials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Piper Sandler’s annualized revenue growth of 16.4% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Piper Sandler reported wonderful year-on-year revenue growth of 33.3%, and its $479.3 million of revenue exceeded Wall Street’s estimates by 9.8%.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Key Takeaways from Piper Sandler’s Q3 Results

We were impressed by how significantly Piper Sandler blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 1.3% to $331.08 immediately after reporting.

Piper Sandler had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.