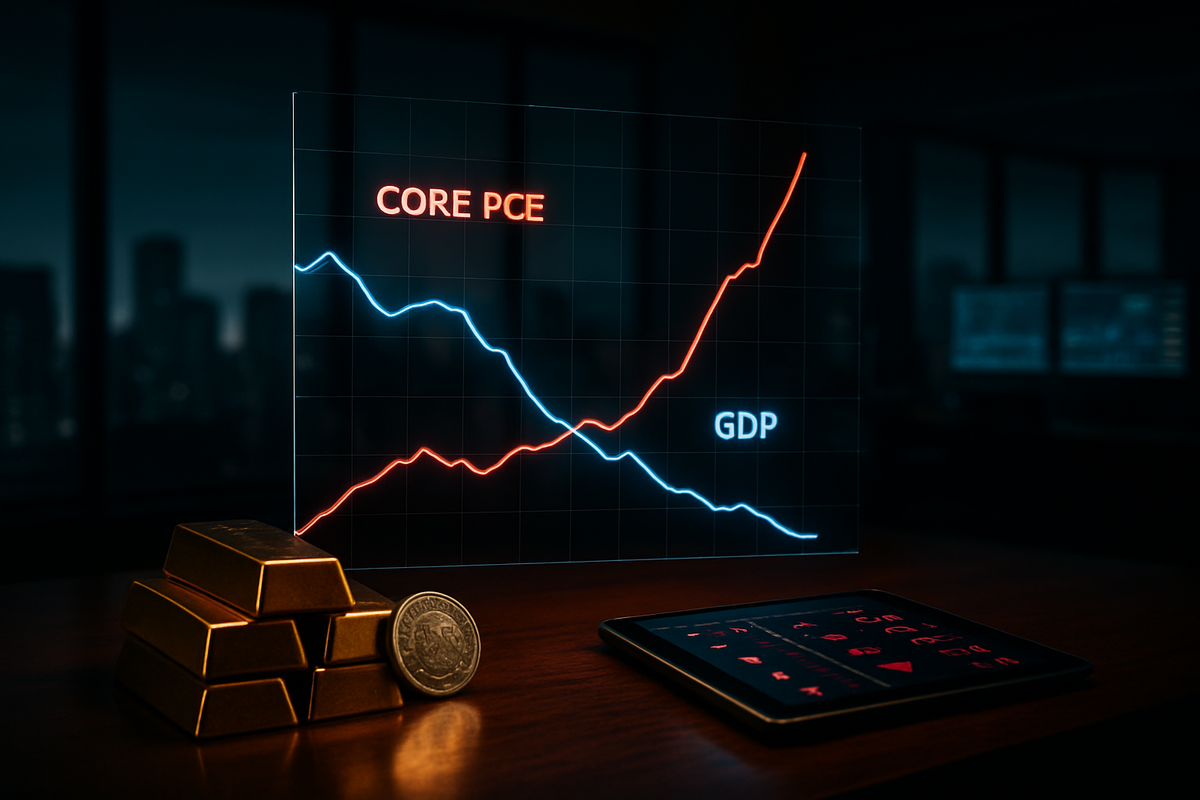

The financial markets are grappling with a "messy message" as the latest economic data reveals a widening gap between persistent price pressures and a cooling economy. In a dual-release shock that has upended expectations for 2026, the Department of Commerce reported that the Core Personal Consumption Expenditures (PCE) price index rose 0.4% month-over-month in December 2025. This acceleration represents the sharpest monthly increase in nearly a year, pushing the annual core rate to 3.0% and effectively stalling the Federal Reserve’s progress toward its 2% target.

Compounding the concern, the fourth-quarter Gross Domestic Product (GDP) growth for 2025 was revised down to a tepid 1.4% annualized rate—a dramatic deceleration from the 4.4% growth recorded in the third quarter. This combination of "sticky" inflation and stagnant output has revitalized the dreaded "stagflation" narrative, forcing investors to recalibrate their expectations for interest rate cuts and causing a visible shift in defensive market positioning. As of today, February 20, 2026, the specter of a 1970s-style economic malaise is no longer a fringe theory but a central pillar of Wall Street debate.

A "Messy Message" in the Numbers

The December 2025 Core PCE data, released in late January and thoroughly digested by the markets this month, caught analysts off guard. While consensus estimates had penciled in a modest 0.2% to 0.3% increase, the actual 0.4% print was driven by a surprising rebound in goods prices—largely attributed to the cumulative effect of trade tariffs—and a relentless rise in service-sector costs. This "sticky" inflation print arrived just as the Q4 GDP figures highlighted a sharp slowdown, exacerbated by a 43-day federal government shutdown that paralyzed government spending and dampened consumer sentiment late in the year.

The timeline leading up to this moment has been one of volatile transitions. Throughout mid-2025, the narrative was focused on a "soft landing," where inflation would fade without a significant hit to growth. However, by the time the Federal Open Market Committee (FOMC) met in late January 2026, the tone had shifted. While Fed Chair Jerome Powell initially described the inflation overshoot as "modestly positive" due to its concentration in temporary goods categories, the release of the FOMC minutes in mid-February revealed a far more hawkish internal debate. Several officials suggested that if inflation does not moderate in the first quarter of 2026, the Fed may be forced to consider interest rate hikes rather than the long-anticipated cuts.

Market reactions have been swift and cautious. The 10-year Treasury yield, often a bellwether for long-term economic expectations, has climbed toward the 4.19% mark as traders accept that the Fed will remain "on the sidelines for longer." Simultaneously, "stagflation hedges" have surged; gold (NYSE Arca: GLD) recently crossed the historic $5,000 per ounce threshold, while silver has seen double-digit percentage gains over the last month as investors seek refuge from the eroding purchasing power of the dollar in a low-growth environment.

Corporate America in the Crosshairs

The current economic climate has created a stark divide between sectors, with companies like Walmart Inc. (NYSE: WMT) emerging as "trade-down" beneficiaries. In its most recent earnings report, Walmart posted record fourth-quarter revenue of $190.7 billion, fueled significantly by high-income households (earning over $100,000) switching to value-oriented shopping. However, even the retail giant is wary; management issued cautious guidance for fiscal year 2027, citing an "unpredictable" consumer who is increasingly sensitive to price hikes in non-discretionary goods.

Conversely, the banking sector is facing "structural inflation" that threatens to eat into profit margins despite higher interest rates. JPMorgan Chase & Co. (NYSE: JPM) CEO Jamie Dimon has been a vocal critic of the optimistic "soft landing" consensus, warning that he "couldn't rule out" a stagflationary outcome. The bank recently projected a $9 billion to $10 billion increase in internal expenses for 2026, driven by rising labor and real estate costs. This "pessimistic pragmatism" from the nation’s largest bank has set a somber tone for the financial sector, as the benefit of higher lending rates is increasingly offset by rising operational costs and potential loan defaults in a slowing economy.

Technology stalwarts are also feeling the squeeze of rising input costs. Apple Inc. (NASDAQ: AAPL) reported record revenue of $143.8 billion for its first fiscal quarter of 2026, buoyed by the "AI supercycle" of the iPhone 17. Yet, the stock has slipped roughly 6% from its January highs. Investors are increasingly concerned about a global crunch in memory chip prices (NAND and DRAM), which threatens to compress margins just as the company tries to scale its expensive AI hardware. For growth companies, the combination of high "higher-for-longer" discount rates and rising supply chain costs represents a double-edged sword that could stifle innovation spending in the coming quarters.

The Global Significance and Historical Echoes

The re-emergence of stagflation concerns fits into a broader global trend of "deglobalization" and supply-side constraints. Economists at RBC Economics have coined the term "Stagflation Lite" to describe the current era, where service inflation remains anchored around 3% while GDP growth struggles to break 2%. This differs from the double-digit misery of the 1970s but presents a similar policy nightmare for central banks: traditional tools to fight inflation (higher rates) only further dampen the already fragile growth, while tools to stimulate growth (lower rates) risk reigniting the inflationary fire.

The potential ripple effects extend far beyond U.S. borders. If the Federal Reserve maintains a restrictive stance while growth slows, the U.S. dollar may remain unnaturally strong, exporting inflation to trading partners and placing immense pressure on emerging market debt. Furthermore, the 1.4% GDP growth rate highlights the vulnerability of the domestic economy to political shocks, such as the late-2025 government shutdown, which many analysts view as a self-inflicted wound that has left the U.S. with less "buffer" to withstand external shocks like energy price spikes or geopolitical instability.

Historically, periods of stagflation have led to a "K-shaped" corporate recovery, where companies with immense pricing power and low capital intensity outperform, while capital-heavy industries and those reliant on low-income discretionary spending fall behind. We are seeing a modern iteration of this as firms scramble to integrate Artificial Intelligence (AI) as a productivity hedge—attempting to automate their way out of the "labor-cost-push" inflation that is currently bedeviling the services sector.

What Lies Ahead: A Policy Deadlock?

In the short term, the Federal Reserve is likely to remain in a "wait-and-see" posture, effectively pausing the rate-cut cycle that markets had hoped would begin in early 2026. This "higher for longer" reality will test the resilience of the commercial real estate market and mid-sized regional banks, which are more sensitive to prolonged periods of high borrowing costs. Strategic pivots are already underway in the corporate world, with a renewed focus on "operational efficiency" and "margin preservation" replacing the "growth-at-all-costs" mentality of the early 2020s.

The long-term outlook depends heavily on whether the 0.4% PCE spike was a one-time "tariff hiccup" or the start of a new inflationary trend. If inflation remains above 3% throughout the first half of 2026, market participants should prepare for the possibility of a "terminal rate hike"—a final, aggressive move by the Fed to break the back of inflation, even at the risk of a technical recession. Conversely, if the GDP slowdown deepens into negative territory while prices remain high, the political pressure on the Fed to pivot regardless of inflation will become intense, creating a volatile environment for both bonds and equities.

Conclusion and Investor Takeaway

The December 2025 data serves as a stark reminder that the battle against inflation is rarely a linear progression. The 0.4% month-over-month Core PCE increase, coupled with a disappointing 1.4% GDP growth, has shattered the "immaculate disinflation" narrative. Investors must now navigate a landscape where the Federal Reserve is effectively boxed in, and the threat of stagflation is the primary driver of market volatility.

Moving forward, the focus will shift to first-quarter 2026 earnings and guidance. Investors should pay close attention to management commentary on "input cost pressures" and "consumer resilience." The key takeaways are clear: the era of easy money is not returning anytime soon, and the "quality" of a company’s balance sheet and its ability to pass on costs will be the primary determinants of success. In the coming months, watch for the "March Madness" of economic data—the next PCE release will either confirm a trend or reveal a statistical anomaly, and the market’s reaction will likely define the trajectory for the rest of 2026.

This content is intended for informational purposes only and is not financial advice.