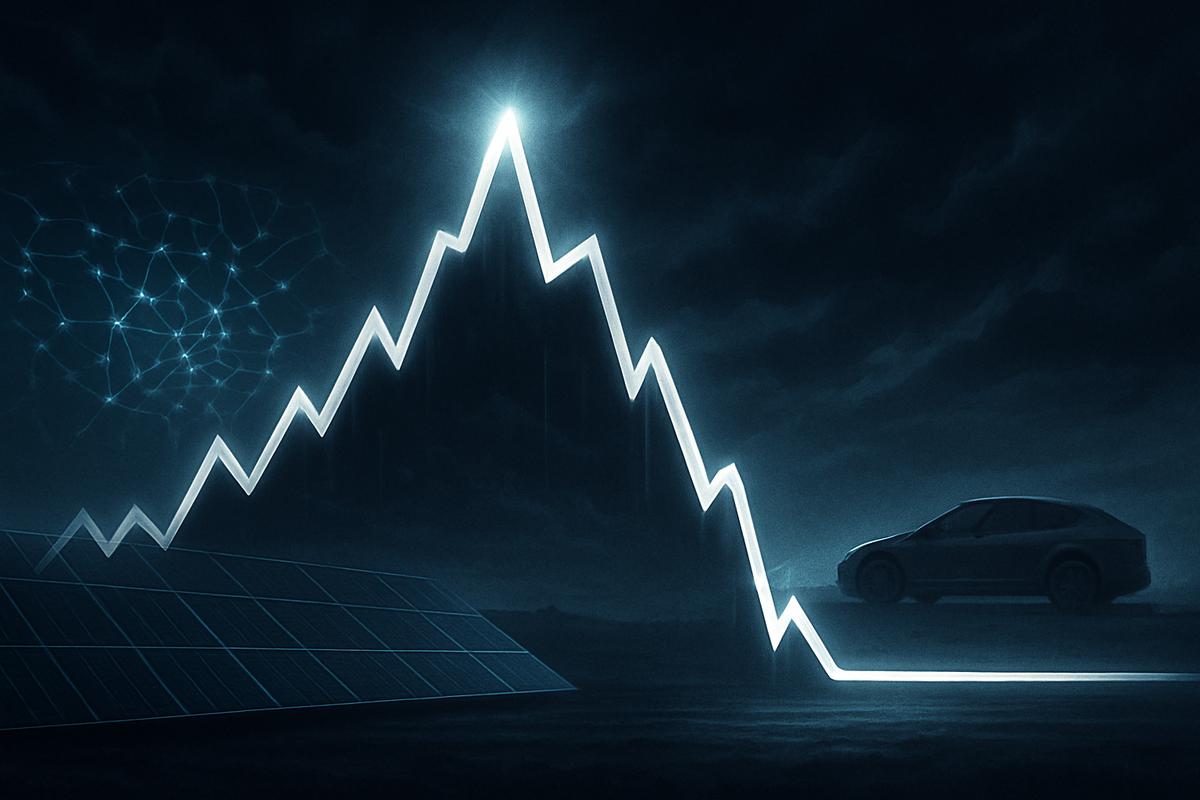

The global silver market has just survived the most "violent" price cycle in its history. In a span of less than eight weeks, the precious metal surged from its 2025 closing levels to a staggering peak of $121 per ounce, only to plummet 43% in a matter of days. As of today, February 20, 2026, the market appears to have found a tentative floor, with spot prices stabilizing around the $80 mark—a level that remains historically high but feels like a relief after the chaos of January.

This unprecedented volatility has rewritten the playbook for commodity traders and industrial end-users alike. The "silver squeeze" of 2026 was not merely a speculative frenzy; it was a collision between a massive "monetary fear" trade and an insatiable industrial appetite driven by the triple engine of Artificial Intelligence, solar energy, and electric vehicles. While the speculative froth has been largely purged, the underlying structural deficit suggests that the era of "cheap" silver is firmly in the rearview mirror.

The 'Warsh Shock' and the $121 Peak: A Timeline of Volatility

The ascent began in early January 2026, building on a massive 144% gain from the previous year. By the third week of the month, silver entered a parabolic "blow-off top," fueled by retail gamma squeezes and institutional panic. On January 26, silver hit an all-time high of $121.64 per ounce. At that moment, the gold-to-silver ratio collapsed to levels not seen in decades, as investors treated silver as "gold on steroids," hedging against a $38.5 trillion U.S. national debt and fears of persistent currency debasement.

However, the music stopped abruptly on January 30, 2026, an event now known in trading pits as the "Warsh Shock." The nomination of Kevin Warsh to succeed Jerome Powell as Federal Reserve Chair sent shockwaves through the "debasement trade." Warsh, perceived as a hawkish proponent of "Sound Money" and a smaller Fed balance sheet, signaled a definitive end to the era of unlimited liquidity. The reaction was instantaneous: silver futures suffered their worst one-day decline since 1980, plummeting over 30% in a single session. Prices eventually bottomed near $64.08 in early February before the current recovery to $80 took hold.

Initial market reactions were polarized. While bullion dealers reported record physical premiums during the crash, the paper markets saw a "massive forced rebalancing." Speculators who had entered at $100+ were liquidated, while industrial buyers, who had been sidelined by triple-digit prices, finally stepped back in to secure supply, providing the $64 floor that saved the market from a total collapse.

Miners and ETFs: Navigating the Storm

Among the primary beneficiaries and victims of this volatility is First Majestic Silver (NYSE: AG). As a "pure-play" silver producer, the company’s stock price has mirrored the metal’s erratic moves. Despite the price crash from $121, First Majestic has remained resilient due to its aggressive management of All-In Sustaining Costs (AISC). In late 2025, the company reported an AISC of approximately $20.90 per ounce. However, the 2026 guidance has shifted to a range of $26.15 to $27.91, reflecting the rising costs of labor and energy in a high-inflation environment.

First Majestic's management, led by President Mani Alkhafaji, has doubled down on its refusal to hedge its production, a move that allowed it to capture the full upside of the $121 peak but exposed it during the 43% drawdown. To appease shareholders, the company recently doubled its dividend policy to 2% of net revenue, a signal of confidence that $80 silver provides more than enough margin for sustained profitability. Conversely, the iShares Silver Trust (NYSE Arca: SLV) experienced a historic exodus. On January 30 alone, the ETF saw an estimated $3.5 billion in sell orders. As of mid-February, the fund has shed over $7.6 billion in assets under management, reflecting a pivot from speculative "paper" holdings back toward industrial-grade physical accumulation.

The Dual Drivers: AI, Green Tech, and Monetary Fear

The wider significance of silver’s current $80 stabilization lies in its dual identity. Unlike gold, which is primarily a monetary asset, silver is now 60% industrial. The 2026 surge was underpinned by a "structural deficit" that cannot be fixed by interest rate hikes alone. In the AI sector, silver has become a critical component for high-performance semiconductors and the massive data centers required to power generative AI. Global IT power capacity has exploded, and with it, the need for silver’s superior thermal and electrical conductivity.

Furthermore, the green energy transition has reached a tipping point. Solar demand now represents nearly 30% of industrial silver use. The shift to next-generation architectures like TOPCon and Heterojunction Technology (HJT) has increased the silver intensity per solar cell by up to 100%. Simultaneously, the EV market continues to exert pressure; a Battery Electric Vehicle (BEV) requires nearly 80% more silver than a traditional internal combustion engine. This "green" floor is what prevented silver from returning to its pre-2025 levels of $25-$30 during the recent crash.

The Road Ahead: Stabilization or New Base?

In the short term, the market is expected to remain in a consolidation phase between $75 and $85. The "monetary fear" trade has cooled following the Warsh nomination, but it has not disappeared. With the U.S. fiscal deficit remaining a structural reality, any sign of a Fed "pivot" or a return to quantitative easing could reignite the speculative fire. For miners like First Majestic, the challenge will be managing costs in an environment where the "easy" silver has already been mined, forcing a reliance on lower-grade ores that require higher prices to be economically viable.

Long-term, the industry may see a wave of consolidation. Smaller miners who cannot manage an AISC below $30 may become acquisition targets for larger players looking to secure physical reserves for industrial contracts. We may also see direct partnerships between tech giants and mining firms—a scenario where an AI chipmaker or an EV manufacturer takes a direct equity stake in a silver mine to guarantee its supply chain against future $120 price spikes.

Conclusion: A New Era for the 'Devil's Metal'

The "violent" price action of early 2026 has served as a wake-up call for the global financial system. Silver is no longer just a "poor man’s gold"; it is a strategic industrial metal essential for the 21st-century economy. The crash to $64 and the subsequent recovery to $80 suggest that the market has finally found a price that balances speculative interest with industrial reality.

Moving forward, investors should keep a close eye on the gold-to-silver ratio and the monthly AISC reports from major producers. While the triple-digit peaks of January may seem like a distant memory, the structural supply deficit remains. The "New Normal" of $80 silver is here, and for a world increasingly dependent on AI and renewable energy, the "Devil's Metal" has never been more heavenly—or more volatile.

This content is intended for informational purposes only and is not financial advice.