The only constant in interest rates is change. So, how does one go about securing the best possible terms for one’s clients?

Start by understanding the interest rate landscape itself. Next up, dive into more advanced concepts and techniques for senior homeowners, like a reverse mortgage.

This article covers how mortgage professionals can navigate reverse mortgage rates and put practical strategies to work for securing the most favorable terms for their clients.

Understanding reverse mortgages and how they work

A reverse mortgage is a financial product designed for homeowners aged 62 and above. It works differently from standard mortgage loans, where homeowners make monthly payments to a lender and gradually build equity.

In a reverse mortgage, homeowners access their home equity as cash — either in a lump sum, a line of credit, or monthly payments. The loan typically must only be repaid once the homeowner passes away, sells the property, or moves out.

Seniors typically use reverse mortgages to:

- Pay off an existing mortgage and free up cash flow.

- Pay for home repairs and modifications.

- Supplement their retirement income.

- Pay for medical expenses.

- Consolidate debt. Credit card balances are among the most common debts seniors carry into retirement, and using home equity to pay them off can seem appealing. However, it’s worth seeking expert credit card advice before committing, since a reverse mortgage converts unsecured debt into a claim against the home.

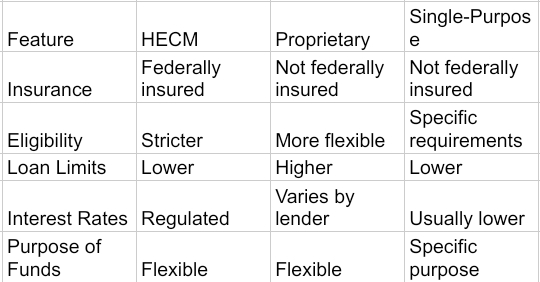

Types of reverse mortgages

Reverse mortgages come in various forms, each with its own features and benefits. Understanding these options helps brokers tailor solutions to their clients’ needs.

The following table summarizes the main types of reverse mortgages.

Let’s break them down.

Home Equity Conversion Mortgages (HECMs)

Home Equity Conversion Mortgages, or HECMs, are the most common type of reverse mortgage. They’re backed by the Federal Housing Administration (FHA) and come with consumer protections, including mandatory counseling. However, they often have stricter eligibility requirements and lower loan limits than proprietary options.

Non-HECM reverse mortgages

Non-HECM reverse mortgages aren’t insured by the FHA. They can appeal to borrowers who don’t meet HECM eligibility requirements or who want higher loan amounts or more flexible terms.

That said, they typically come with higher interest rates and may have different origination fees and servicing costs than HECMs. There are two main types:

- Proprietary reverse mortgages: These are private loans offered directly by lenders — banks, credit unions, or mortgage companies. Because they aren’t federally insured, lenders have more flexibility in setting eligibility requirements, loan terms, and interest rates. This can mean higher loan amounts, more flexible repayment options, and lower minimum credit score requirements than HECMs.

- Single-purpose reverse mortgages: These are offered by local governments, non-profit organizations, or housing authorities. They’re designed to address specific needs for senior homeowners, often focusing on low- and moderate-income borrowers. Single-purpose reverse mortgages typically have lower interest rates than other non-HECM options, but they restrict how the loan funds can be used.

Jumbo reverse mortgages

Jumbo reverse mortgages are a type of proprietary reverse mortgage designed for homeowners with high-value properties. They allow borrowers to access more home equity than HECMs, which have federally mandated loan limits.

Fixed- and variable-interest-rate reverse mortgages

Depending on the borrower’s risk tolerance and financial goals, they can choose between a fixed-rate loan and one with variable rates. Here’s a breakdown to help brokers guide their clients:

- Fixed-rate reverse mortgages: These offer predictability and stability. The interest rate stays constant throughout the loan term, so the borrower’s monthly payout and the amount of equity converted over time remain consistent.

- Adjustable-rate reverse mortgages (ARMs): ARMs can offer lower initial interest rates than fixed-rate options. However, the rate adjusts periodically based on a financial index, typically the LIBOR (London Interbank Offered Rate). They also carry a margin of 1.75% to 2.5% and a lifetime cap of 5% over the original rate.

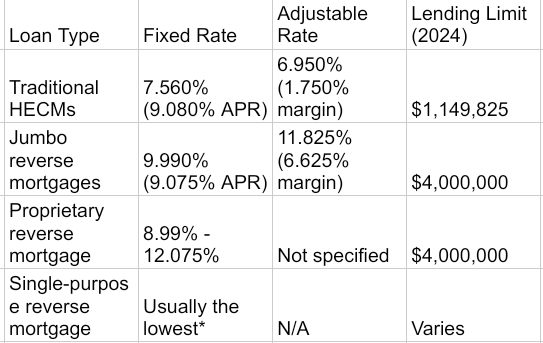

Reverse mortgage interest rates

Interest rates are one of the most important factors when determining a reverse mortgage’s total cost. The following table summarizes typical rates for the different types of reverse mortgage loans:

* Single-purpose reverse mortgage rates are typically lower than the other types, but the rate depends on the lender and the particular program. They’re also generally fixed-rate loans, not adjustable.

Factors that affect reverse mortgage rates

Understanding what influences reverse mortgage rates helps professionals guide clients toward the most cost-effective solutions. These factors break down into borrower-specific, loan-specific, and additional categories.

Borrower-specific factors

- Age: Older borrowers generally qualify for lower rates because of a shorter statistical life expectancy. This means a shorter loan term and less risk for the lender.

- Home value: Higher home values often lead to lower rates, as they provide more collateral for the lender.

- Loan amount: Smaller loan amounts might result in higher rates because fixed closing costs are spread over a smaller balance.

- Credit score: While not as critical as with traditional mortgages, a good credit score can help secure a slightly lower rate.

Loan-specific factors

- Type of reverse mortgage: HECM loans have regulated rates, while proprietary loans offer more flexibility but may come with higher rates. Single-purpose mortgages typically offer the lowest rates.

- Interest rate type: Fixed-rate loans offer stability at higher rates, while adjustable-rate loans can fluctuate with market conditions — potentially offering lower initial rates in exchange for more risk.

- Loan disbursement method: The method chosen — monthly payments, line of credit, or lump sum — can affect the interest rate structure and overall cost.

Additional factors

- Origination fees and closing costs: These can increase the loan’s overall expense and impact the effective interest rate. Brokers should negotiate these fees on behalf of their clients.

- Mortgage Insurance Premium (MIP): HECMs require an upfront and annual MIP, which is factored into loan costs.

- Prevailing interest rates: The broader economic landscape and Federal Reserve actions heavily influence rates.

How mortgage brokers can help their clients find the best rates

Mortgage brokers play a central role in helping clients work through the complexity of reverse mortgage rates. Here’s how they add value:

- Educate clients: Helping clients understand the factors that affect reverse mortgage rates lets them make informed decisions and see the trade-offs between different loan options.

- Leverage expertise and networks: Brokers have deep knowledge of the reverse mortgage market and established relationships with multiple lenders. Access to a broader network means access to a wider range of options and more competitive rates.

- Provide personalized service: Brokers take the time to understand each client’s financial situation and goals, which lets them recommend the most suitable reverse mortgage product and interest rate type.

- Negotiate with lenders: Brokers should make an effort to negotiate lower rates, reduced fees, or more favorable loan terms on behalf of their clients.

Running a lean practice matters too. Brokers who keep close track of their own business expenses — marketing, software subscriptions, licensing renewals, travel to property appraisals — can reinvest those savings into better client service and stronger lender relationships. Many independent brokers now use tools like corporate cards from Ramp to manage spending across these categories and identify areas where they can cut costs without sacrificing quality.

The bottom line: when is a reverse mortgage the right choice?

A reverse mortgage can work well for some seniors, but it isn’t for everyone. Whether it’s the right call depends on individual circumstances and financial goals.

If a senior homeowner needs to supplement their retirement income or cover unexpected expenses, a reverse mortgage can provide access to cash without requiring monthly payments. However, if they plan to sell their home, move soon, or have limited home equity, other options may make more sense.

Consulting with a knowledgeable mortgage broker is the best way to work through the complexities of reverse mortgage rates and terms. A good broker can walk clients through the process and make sure they get the best deal possible while making an informed decision about their financial future.