Shares of software giant Oracle Corporation (ORCL) have been under pressure lately, with the stock sliding into double-digit losses in early 2026 as a growing list of concerns rattles investor confidence. Much of the scrutiny centers on Oracle’s massive $300 billion partnership with OpenAI, which has fueled debate on Wall Street about the scale and risks of the company’s aggressive artificial intelligence (AI) push.

Investor anxiety has intensified as Oracle ramps up capital expenditures to fund a massive AI infrastructure buildout, particularly through new data centers. But this aggressive spending spree has also pushed Oracle’s debt levels higher, raising fresh questions about how the company plans to fund its ambitions, and whether its cash flow can keep pace. In fact, the situation has become even more complicated as Oracle faces multiple securities fraud class-action lawsuits.

The complaints allege that the company and its executives misled investors about its AI infrastructure strategy, capital spending plans, and the risks tied to its massive data center investments, especially those linked to OpenAI contracts. At the same time, the rapid rise of AI agents is beginning to reshape the broader software industry, sparking fresh debate about the long-term durability of traditional software business models, an evolving shift that has only added to the pressure weighing on ORCL shares.

So, with legal scrutiny rising, capital spending climbing, and AI-driven industry disruption accelerating, is the recent pullback in Oracle shares a tempting buy-the-dip opportunity, or a sign of bigger challenges brewing ahead?

About Oracle Stock

Founded in 1977, Texas-based Oracle is one of the world’s leading enterprise technology companies. The company develops database software, cloud infrastructure, and AI-powered enterprise applications that help organizations manage data, run business operations, and build modern digital services. Today, Oracle’s technologies power everything from finance and supply chains to customer management and large-scale cloud computing for businesses and governments around the world.

Since fiscal 2012, Oracle has invested more than $90 billion in research and development and spent over $110 billion on more than 150 acquisitions, underscoring its aggressive push to expand its cloud and enterprise technology ecosystem. Its ecosystem is equally extensive, with five million registered members in its customer and developer communities and 469 independent user communities across 97 countries.

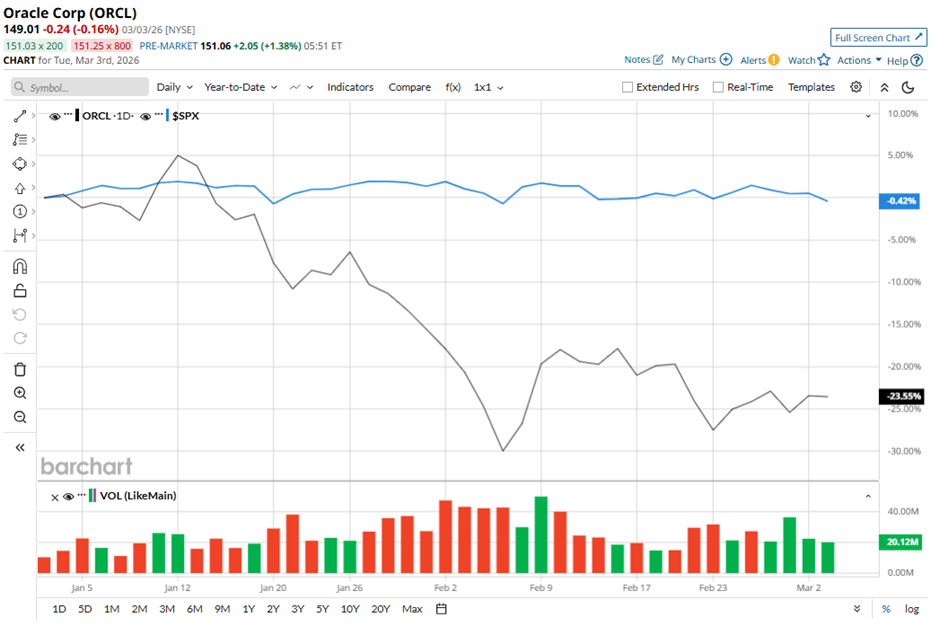

Currently valued at roughly $428.1 billion by market capitalization, shares of this software giant came under intense selling pressure this year. The stock has fallen nearly 21.83% in 2026 alone, weighed down by growing investor anxiety over the company’s heavy capital spending, rising debt used to finance those investments, and broader concerns about the impact of AI agents on the software industry.

For context, the broader S&P 500 Index ($SPX) has grown marginally during the same period, highlighting the magnitude of Oracle’s underperformance. After climbing to a 52-week high of $345.72 in September last year, the stock has since tumbled nearly 56% from that peak, underscoring the shift toward sharp sentiment around the tech giant.

Oracle Tanks After Q2 Earnings Release

Oracle’s fiscal 2026 second-quarter results, reported on Dec. 10, delivered a mixed picture that left investors with plenty to digest. On the surface, the numbers looked strong, but a closer look revealed why the market reacted negatively. Revenue grew 14% year-over-year (YOY) to $16.06 billion, yet it slightly missed Wall Street’s $16.15 billion estimate, prompting a swift market reaction that pushed the stock down 10.83% on Dec. 11.

However, profitability told a very different story. Adjusted earnings per share jumped to $2.26, up an impressive 54% from the prior year, easily crushing analysts’ expectations of $1.63. However, investors were quick to note that much of the earnings boost came from a one-time $2.7 billion gain tied to the sale of Oracle’s stake in chipmaker Ampere.

Looking across the business segments, cloud remained Oracle’s primary growth engine, generating nearly $8 billion in revenue, up 34% YOY. Notably, Cloud revenue now accounts for half of Oracle's overall revenue. In contrast, the software segment declined 3% to $5.9 billion, while both the hardware and services divisions posted modest 7% annual growth.

The real standout metric in the report was Remaining Performance Obligations (RPO), a measure of contracted revenue yet to be recognized. This figure soared an astonishing 438% YOY to $523.3 billion, reflecting a massive backlog of future revenue. According to management, the surge was largely fueled by new commitments from industry giants such as Meta Platforms (META), Nvidia (NVDA), and OpenAI, underscoring Oracle’s growing role in the global AI infrastructure race.

Yet despite this enormous backlog, the market remained uneasy. The key concern was Oracle’s spending trajectory. During the Q2 earnings call, management shocked Wall Street by raising its fiscal 2026 capital expenditure guidance by $15 billion mid-year, pushing total expected capex to roughly $50 billion for the entire year.

The company has already elevated capital spending, aimed at aggressively expanding its AI infrastructure, which has begun to weigh on cash generation. In the latest quarter, free cash flow swung to roughly negative $13.2 billion. Further, the company’s newly raised capex guidance has heightened investor concerns that Oracle may be stretching its balance sheet too aggressively in its push to secure a leading position in the fast-evolving AI infrastructure race.

Nevertheless, investors will soon get another update when Oracle releases its fiscal 2026 third-quarter results on Tuesday, Mar. 10, after market hours. For the upcoming quarter, management expects total cloud revenue to grow between 37% and 41% in constant currency, while overall revenue is projected to increase between 16% and 18%. Meanwhile, non-GAAP EPS is forecast to grow between 12% and 14%, reaching a range of $1.64 to $1.68 in constant currency.

How Are Analysts Viewing Oracle Stock?

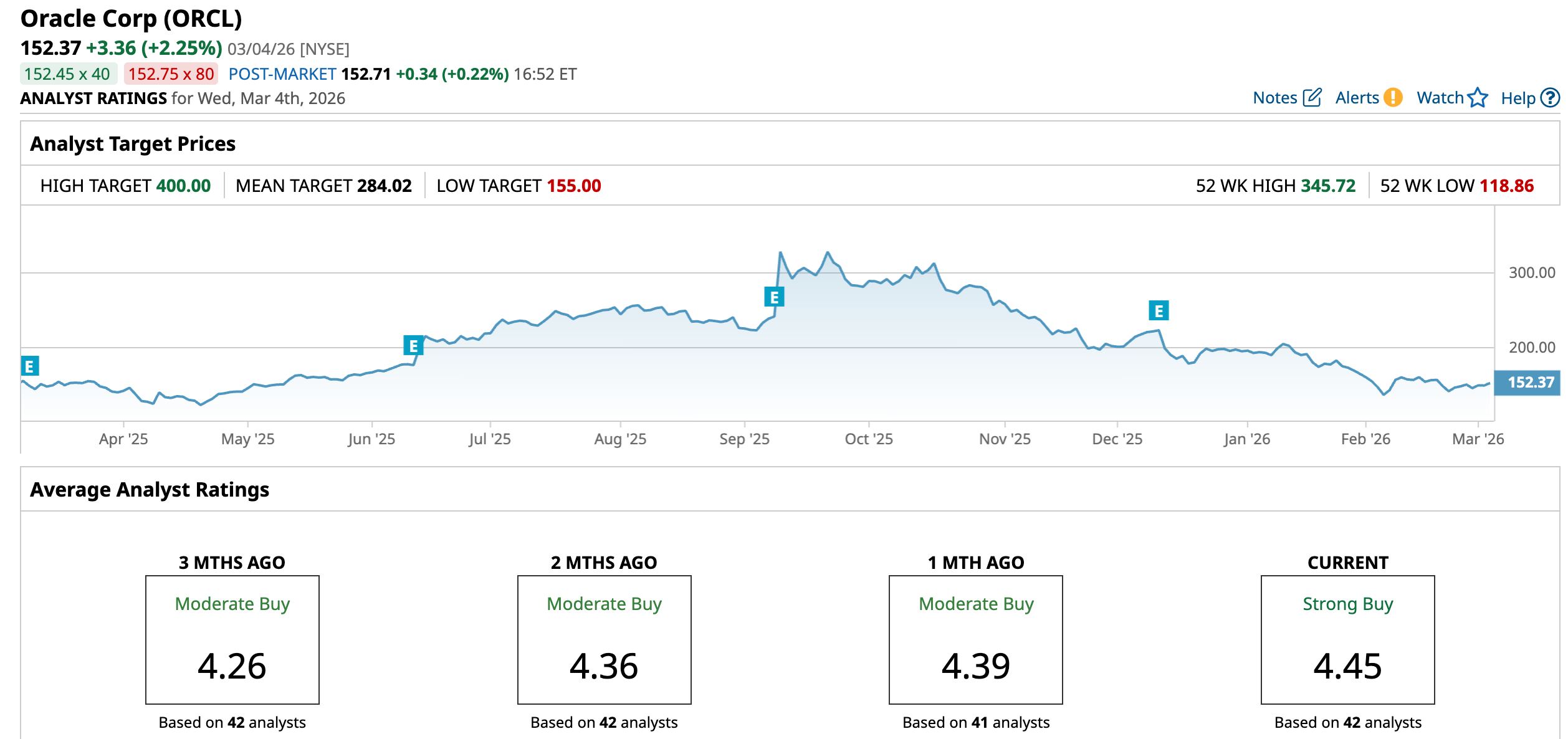

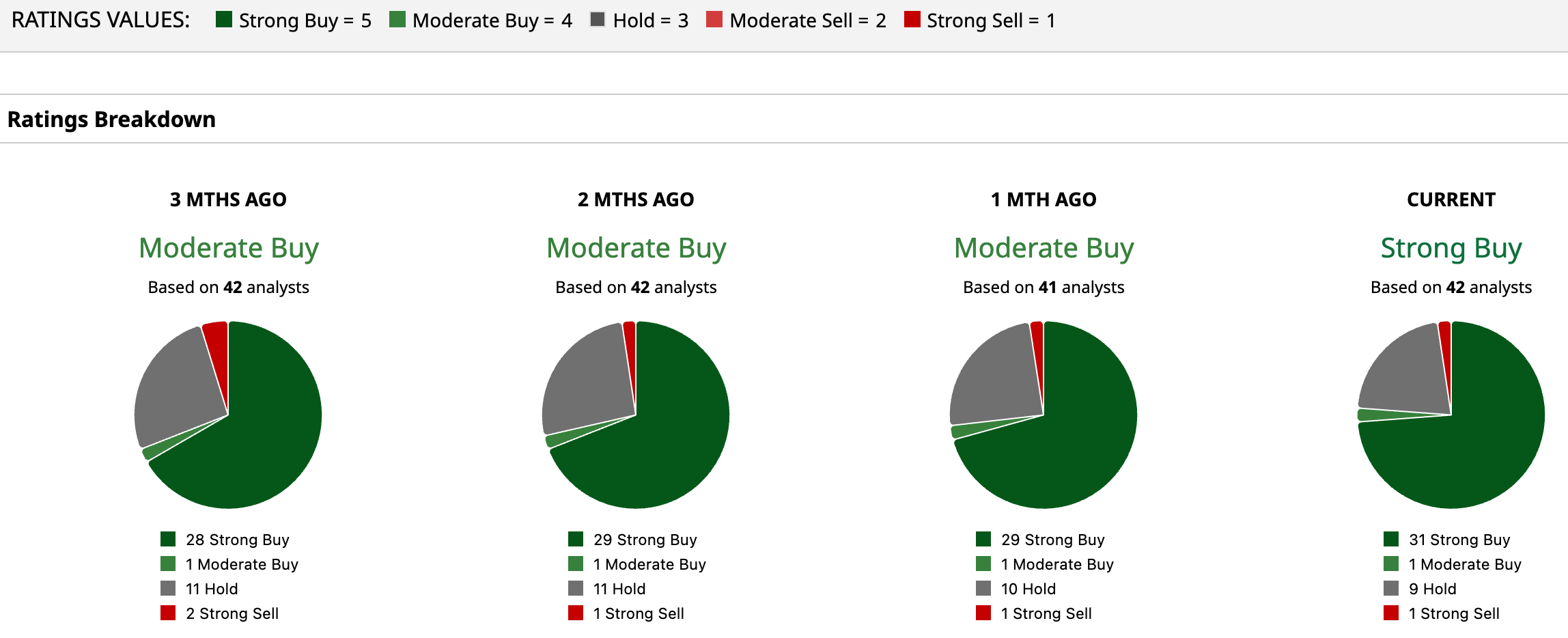

Despite the recent selloff, Wall Street still appears firmly optimistic about Oracle, with the stock carrying a consensus “Strong Buy” rating overall. Among the 42 analysts covering the company, 31 recommend “Strong Buy,” one suggests “Moderate Buy,” nine remain cautious with “Hold,” and only one analyst holds a bearish “Strong Sell” view.

Price targets also signal significant upside potential. The average target price of $284.02 implies that the stock could climb about 86% from current levels, while the Street-high target of $400 suggests a potential rally of as much as 162.5% if bullish expectations play out.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Target Profits Between $165 and $175 with a Broken Wing Butterfly on Nvidia Stock

- 3 ‘Strong Buy’ Dividend Kings That Wall Street Loves Most in 2026

- As Nebius Gets the Green Light for a Massive AI Factory, Should You Buy NBIS Stock?

- Coinbase Stock Just Broke Above Its 50-Day Moving Average on Trump Support. Should You Buy COIN Here?