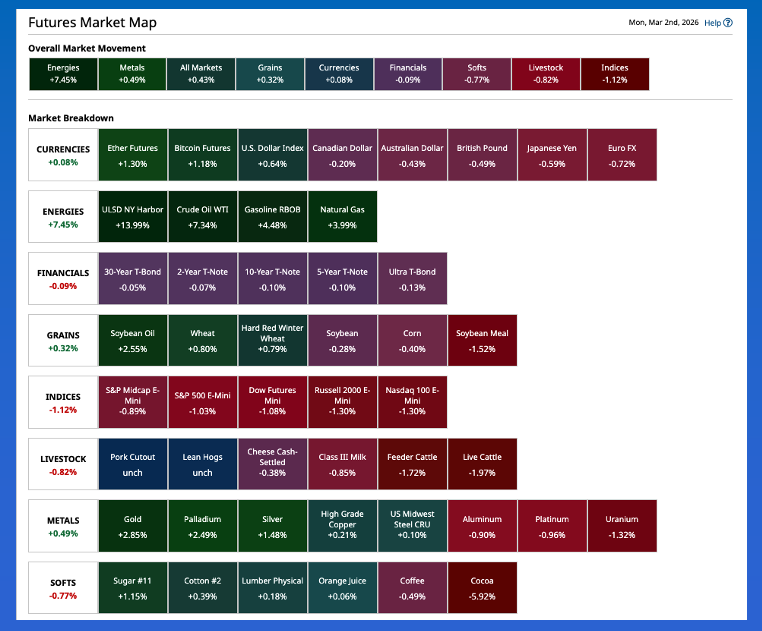

As expected, the Energies sector in the commodity complex exploded higher to start the week.

As expected, the Metals sector followed at a distance as investors continued to move money to safe-haven gold and silver.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.As expected, US stock index futures were under continued pressure due in part to the idea the next rate cut will be pushed back because of an inflation spike.

Morning Summary: Welcome to the first trading day of meteorological spring. This past weekend could’ve been made even more difficult if it included the annual “Spring Forward” event of losing an hour as daylight savings time begins. (This silliness begins next weekend.) Friday night into early Saturday morning, as the final hours of the Dog Days of Winter, also known as February, were set to wind down, the US president reportedly cried havoc and let slip the dogs of war. According to news reports quoting the president’s pre-made video, the US military had begun “major combat operations” in Iran. He added, “Our objective is to defend the American people by eliminating imminent threats from the Iranian regime, a vicious group of very hard, terrible people…”. The reality is a bit different. While the action is the same – what could be considered an illegal military move by the US against Iran – the objective is actually to raise the price of crude oil, the key commodity taken from Venezuela in early January.

Energies: All eyes were on the Energies sector heading into Sunday night’s open. Looking back at last week’s activity, we could tell something was brewing given the spot-month WTI contract closed $1.81 higher on buying from both noncommercial and commercial interests. When this week’s opening bell rang, the global Brent (QAK26) market jumped as much as $9.24 (12.7%) while WTI (CLJ26) exploded to a high of $75.33, up $8.31 (12.4%). As of early Monday morning, both have pulled back about $4. It’s no surprise trade volume was high with the spot-month WTI issue showing more than 405,000 contracts changing hands at this writing. Also not surprise, the backwardation in the market has strengthened through at least the September 2026 issue. Meanwhile, the spot-month distillates contract (HOJ26) added as much as 45.25 cents (17.4%) – Yes, you read that correctly. I’ve double and triple checked the numbers. - while RBOB gasoline (RBJ26) gained as much as 21.0 cents (9.2%). Given this intentional inflation spike, it makes sense the US dollar index ($DXY) firmed by as much as 0.96 because interest rates aren’t coming down any time soon.

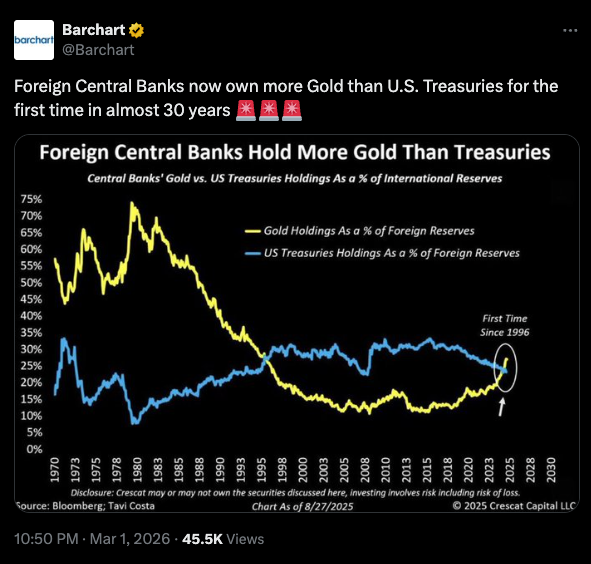

Metals: Speaking of rallying commodities in the face of a firmer dollar, Monday morning’s Barchart Futures Market Heat Map shows the Metals sector followed only Energies higher overnight, though trailed at a considerable distance of 7.5% to 0.5%. Still, markets were impressive overnight as safe-have King Gold (GCJ26) gained as much as $186.20 (3.5%) and was still sitting $150 (2.9%) higher at this writing. I’ve said it for months/years: We can’t apply technical or fundamental analysis to the gold market given it is the most reliable safe-haven market on the planet these days. (If you argue it should be bitcoin, we can’t be friends.) As I pointed out recently, Barchart has run a piece showing foreign central banks now own more gold than US Treasuries for the first time in almost 30 years. There’s a good reason for that: A lack of confidence in the United States as a global leader. End of story. But gold wasn’t alone overnight as silver (SIK26) added as much as $4.00 (4.3%) before cutting its rally in half over the course of Monday morning. Dr. Copper (HGK26) the economic indicator was actually sitting in the red at this writing after initially jumping as much as 3.6 cents (0.6%).

Equities: It should come as no surprise US stock index futures were lower overnight through the pre-dawn hours. Again, watching financial markets last week, we could see cracks starting to form in the three major US stock indexes. Based on analysis of long-term monthly charts, while both the S&P 500 and Dow Jones Industrial Average could still be classified in uptrends, both showed signs of change as February came to a close. The S&P was down 60.15 points for the month while the Dow opened the door to a discussion of the Horseshoe Proximity (Close is close enough) regarding a possible bearish spike reversal. (For the record, the Dow registered a new all-time high of 50,512.79 last month before closing at 48,977.92, up only 85.58 (0.2%)). A look at the quote screen early Monday finds S&P 500 futures (ESH26) down as much as 120.5 points (1.75%), Dow futures (YMH26) falling as much 834 points (1.7%), and Nasdaq futures (NQH26) off as much as 527.75 points (2.1%). Something to think about heading into this week is equity markets aren’t going to like the spike in inflation putting a stop to rate cuts indefinitely. Keep in mind the Fed fund futures forward curve had already pushed back the next move to July.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart