Valued at a market cap of $125.3 billion, The Progressive Corporation (PGR) is one of the largest U.S. personal lines insurers, best known for auto insurance but also offering commercial auto, property, and specialty insurance products. Headquartered in Mayfield Village, Ohio, Progressive operates through a data-driven, direct-to-consumer model complemented by independent agents.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and PGR fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the insurance - property & casualty industry. Progressive is a data-centric auto insurance leader distinguished by sophisticated risk pricing, direct distribution strength, and dominant commercial auto positioning. Its analytics-driven underwriting and scalable digital model support consistent profitability in U.S. personal and commercial auto insurance.

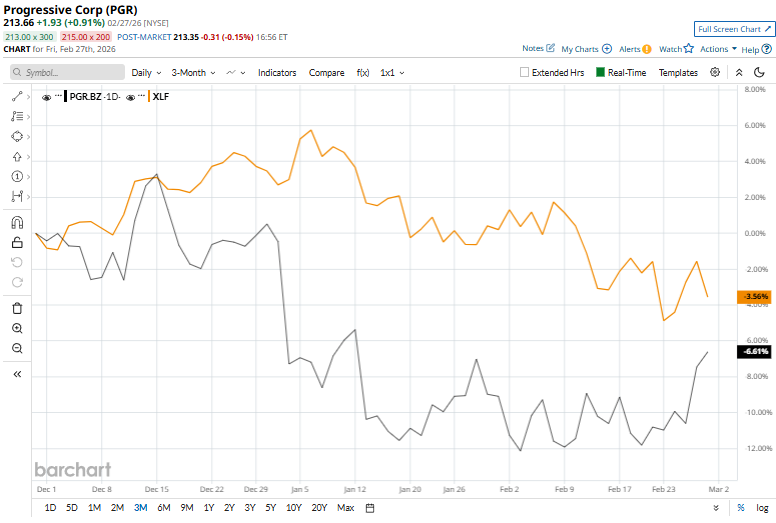

Despite its notable strength, this insurance giant has dipped 27.1% from its 52-week high of $292.99, reached on Mar. 17. Shares of PGR have declined 6.8% over the past three months, considerably underperforming the State Street Financial Select Sector SPDR Fund’s (XLF) 2.9% fall.

Progressive’s stock has slipped into a clear relative downtrend, falling 6.2% over the past year, trailing the XLF’s 4.4% decline. PGR is down 12.7% in six months while the sector ETF has edged marginally higher.

Technicals reinforce the cautious tone, with Progressive trading below its 200-day moving average since early July and under its 50-day since early June, signaling sustained bearish momentum despite minor bounces.

Progressive has trailed the broader market over the past year primarily due to pressure on underwriting profitability and investor concerns about the sustainability of recent earnings strength. Elevated auto claims severity, driven by higher vehicle repair costs, medical inflation, and litigation trends, has required aggressive rate increases that can temporarily slow policy growth and create competitive friction.

PGR has also underperformed its rival, The Allstate Corporation (ALL), which gained 10% over the past 52 weeks and 5.3% over the past six months.

Despite PGR’s recent underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 25 analysts covering it, and the mean price target of $247.48 suggests a 15.8% premium to its current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart