Valued at a market cap of $98.4 billion, United Parcel Service, Inc. (UPS) is one of the world’s largest package delivery and supply chain management companies. Headquartered in Atlanta, Georgia, UPS operates an integrated global logistics network spanning more than 200 countries and territories.

Companies valued at $10 billion or more are typically classified as “large-cap stocks,” and UPS fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the integrated freight & logistics industry. UPS’s competitive strength stems from its exceptionally dense U.S. ground delivery network and fully integrated global logistics system spanning air, ground, international shipping, and contract logistics.

This scale and network integration enable lower unit costs, high reliability, and premium pricing power versus many competitors. UPS further differentiates through advanced route optimization technology (ORION), a diversified SMB customer base, and leadership in high-margin healthcare and cold-chain logistics.

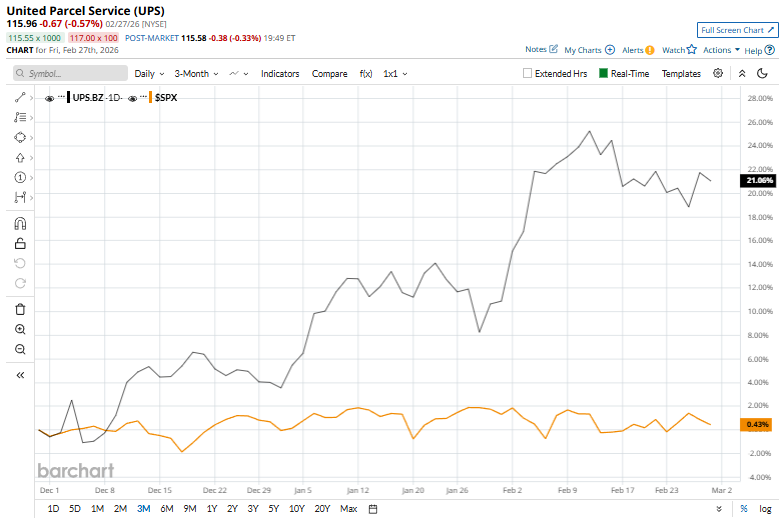

This freight and logistics company is currently trading 6.3% below its 52-week high of $123.70, reached on March 10, 2025. Shares of UPS have gained 21.2% over the past three months, exceeding the S&P 500 Index’s ($SPX) marginal rise.

UPS has surged 32% over the past six months but has declined 21.8% over the past year. In contrast, the SPX has soared 6.1% over the past six months and 17.4% over the past 52 weeks.

To confirm its recent bullish trend, UPS has been trading above its 50-day moving average since mid-October and over its 200-day moving average since mid-December.

On Jan. 27, UPS released its fiscal 2025 Q4 earnings and its shares dipped 3.3% in the next trading session. It posted a revenue of $24.5 billion, adjusted operating profit of $2.9 billion, and adjusted EPS of $2.38, which beat consensus estimates, reflecting pricing discipline and operational efficiency. However, the quarter still faced headwinds from reduced Amazon volumes and weak export demand. Additionally, the company approved a first-quarter 2026 dividend of $1.64 per share on all outstanding Class A and Class B shares, payable on March 5.

UPS has lagged behind its rival, FedEx Corporation (FDX), which has grown 49.7% over the past 52 weeks and 66.7% over the past six months.

The stock has a consensus rating of "Moderate Buy” from the 28 analysts covering it, and it currently trades above the mean price target of $115.15.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart