The Woonsocket, Rhode Island-based CVS Health Corporation (CVS) is an integrated healthcare enterprise that connects insurance, pharmacy benefit management, and retail pharmacy services under one roof. The company delivers medical and government-sponsored health plans, manages prescription drug benefits for employers and public programs, and runs a nationwide network of pharmacies and specialty care centers.

With a market cap of approximately $101.6 billion, CVS stock sits in the “large-cap” territory, a bracket reserved for companies valued above $10 billion. Its scale signals diversified revenue streams, entrenched relationships with payors and providers, and meaningful leverage in a healthcare system that rewards integration and efficiency.

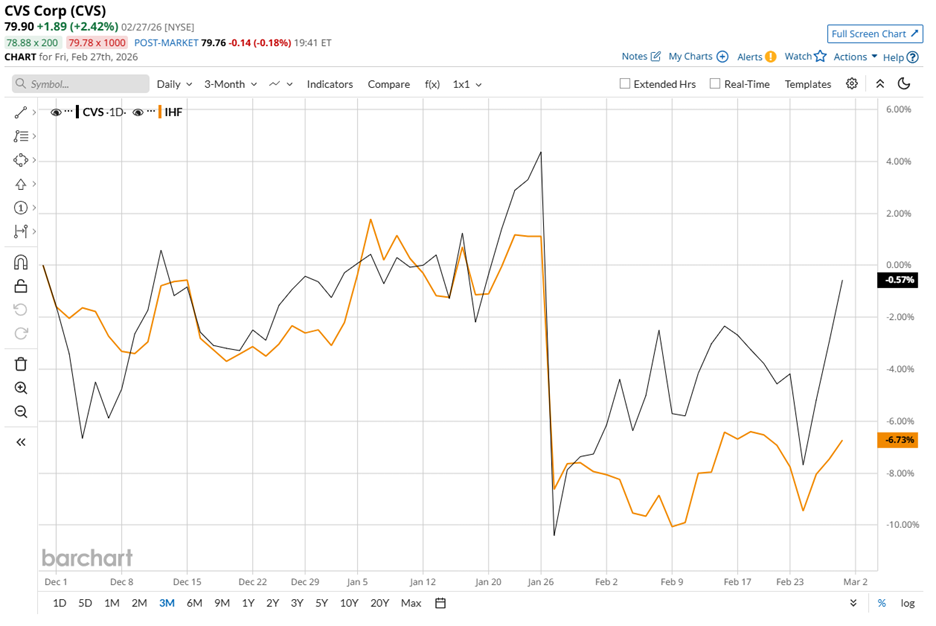

CVS stock currently trades 6.2% below its 52-week high of $85.15 reached in October 2025. Shares have edged higher over the past three months, while the iShares U.S. Healthcare Providers ETF (IHF) declined 8.8% during the same period, reflecting CVS Health’s outperformance.

Over the past 52 weeks, CVS stock has advanced 23.9%, a sharp contrast to the 8.8% decline posted by the ETF during the same period. Year-to-date (YTD), CVS stock remains modestly higher, again outperforming the benchmark’s 3.8% drop and signaling sustained relative strength within the healthcare space.

Technically, the chart reinforces the improving tone. The stock traded above its 50-day moving average in late December before pulling back in late January. It has since regained momentum and now trades above the 50-day moving average of $78.33. More importantly, CVS has held above its 200-day moving average of $73.03 since August 2025.

Fundamentals continue to underpin the stock’s upward bias. On Feb. 11, CVS Health shares rose 1.7% after the company released its Q4 2025 results just a day earlier.

Revenue increased 8.2% year over year to $105.7 billion, ahead of analyst expectations of $103.7 billion. Adjusted EPS came in at $1.09, down 8.4% but surpassed the $1 analyst estimate, reinforcing confidence in near-term earnings stability.

Management pointed to stronger operational efficiency and a sharper customer experience as central drivers. In a cost-sensitive healthcare environment, incremental efficiency gains often translate directly into margin durability, and CVS Health appears to be capturing that leverage.

To put CVS Health’s performance into a clearer perspective, its rival, Centene Corporation (CNC), has fallen 22.9% over the past 52 weeks, though the stock rebounded 9.1% YTD, reflecting a partial recovery that still trails CVS’s stronger longer-term momentum.

Wall Street’s tone remains constructive. CVS holds a “Strong Buy” overall rating from 24 analysts. The mean price target of $94.96 implies potential upside of 18.8% from current levels, signaling that analysts see room for expansion.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart