Over the past few months, mega-cap tech stocks have been caught in an unusual tech tug-of-war: investors are thrilled about AI growth but jittery about how much it will cost to build the infrastructure needed to deliver that AI future. Big names like Alphabet (GOOG) (GOOGL) and Microsoft (MSFT) have seen share prices dip after eye-popping capital expenditure plans flooded into the market alongside earnings reports.

In this climate, Amazon’s (AMZN) latest quarterly report triggered its own selloff, not because the business is faltering, but because the company plans $200 billion in capex for 2026, far above Street expectations and well ahead of its peers’ recent guidance. That shocked the market so much that even famed bull Dan Ives trimmed his price target to $300, despite saying management’s guidance might be too conservative. AWS revenue is still growing about 24%, and high-margin ads and services are accelerating. The big question remains: will Amazon’s record spending dent near-term profit or fuel future growth?

Amazon's AI Deals Accelerate

Amazon is the world’s largest online retailer and the No. 2 cloud provider (AWS). Its unparalleled scale and technology moat, spanning e-commerce, subscription services, ad platforms, and AI-powered cloud, give it a unique market position. That breadth increasingly matters as investors focus on which tech giants can turn AI spending into durable profits.

Amazon has been aggressively expanding its AI and cloud initiatives. Recent highlights include AWS signing new major deals with OpenAI, Visa (V), the NBA, BlackRock (BLK), Perplexity, Lyft (LYFT), and more, reflecting broad enterprise demand. Importantly, Reuters reports Amazon is in talks to invest up to $50 billion in OpenAI, a move that would cement its ties to leading AI infrastructure.

On the product side, AWS’s custom chips are surging: Amazon says Trainium and Graviton now exceed $10 billion in annual revenue and are growing at triple-digit rates. These developments, from cloud contracts to chip innovation, reinforce Amazon’s AI focus and could drive AWS growth and profits over the next few years.

Despite that strategic momentum, Amazon’s stock performance has been far less exciting. Over the past 52 weeks, Amazon’s stock has been roughly down 12%. Shares rallied early on strong AWS growth and better retail sales, but gains were choppy thereafter. Rising expenses and the looming capex outlay kept a lid on performance, leaving shares near flat overall, a lackluster outcome amid market volatility.

That divergence between fundamentals and performance brings valuation into focus. At about 29× earnings and 3.7× sales, AMZN stock trades at typical tech multiples. That P/E is well above the 18× median for traditional retailers. But Amazon’s net margin of 11% tops the industry average, showing its profitable cloud/ads business. Overall, the valuation isn’t cheap on a standalone basis, but it’s roughly in line with its high-growth peers.

CapEx Shock & Impact

However, Wall Street first panicked at the announcement, leading to a heavy selloff. Amazon insists the CapEx surge is a strategic investment, not a panic move. CEO Andy Jassy stressed he expects a “strong long-term return on invested capital” from the spending. Analysts note the heavy outlay will slash free cash flow in 2025 FCF, just $11.2 billion vs. $38.2 billion a year earlier, and press margins. Indeed, Q1 guidance of about $174 billion in sales and $16.5 to 21.5 billion in income implies only modest profit growth, even after factoring in $1 billion of new satellite costs. In short, investors see the guidance shock as evidence that Amazon is front-loading AWS and innovation spending. That will likely weigh on 2026 earnings, but it could strengthen Amazon’s long-run cloud leadership.

Amazon Smashes Q4 Earnings Estimates

Amazon closed the fourth quarter of 2025 with revenue of $213.4 billion, up 14% from a year earlier, as AWS revenue jumped 24%. Operating income reached $25.0 billion, or $27.4 billion excluding one-time items, while net income rose to $21.2 billion, or $1.95 a share, compared with $20 billion, or $1.86, a year earlier. Gross margin held near 48%, and operating margin stood at about 12%, reflecting continued strength in cloud and advertising.

Cash generation told a more mixed story. Operating cash flow over the trailing twelve months climbed nearly 20% to $139.5 billion, but free cash flow fell sharply to $11.2 billion, down roughly 70%, as capital spending accelerated.

Looking ahead, Amazon guided first-quarter 2026 net sales of $173 billion to $179 billion, implying only mid-single-digit operating income growth. Management plans to spend about $200 billion in 2026 on infrastructure, largely tied to AWS AI chips, data centers, and logistics capacity. CEO Andy Jassy described the spending as essential to supporting long-term demand in AI and cloud services. The message is clear: Amazon is leaning into investment even if near-term profits and cash flow come under pressure.

For full-year 2025, Amazon generated $716.9 billion in revenue, up about 12% year-over-year (YoY), and net income of $77.7 billion, compared with $59.2 billion in 2024. Capital expenditures totaled roughly $128.3 billion, a 62% increase from the prior year.

The results show a familiar trade-off for investors: strong growth and record profits, paired with unprecedented investment that tempers short-term cash returns.

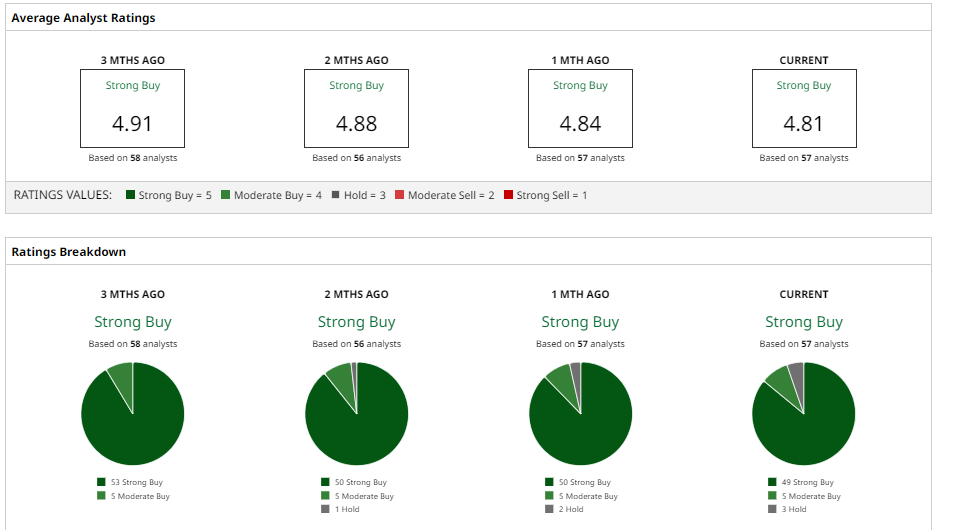

What Do Analysts Say About AMZN Stock?

Wall Street is largely positive on Amazon, although short-term expenditure has a negative impact on mood. Wedbush Morgan Securities analyst Dan Ives maintained an “Outperform” rating with a $300 price target, citing a pickup in AWS pace and rising efficacy in retail stores. Morgan Stanley's Brian Nowak also set a target of $300, citing higher cloud demand and improved discipline in costs in the core of the retail business.

Goldman Sachs raised its target to $300 and retained a “Buy” rating, saying AI and cloud catalysts exceed near-term retail and margin headwinds.

RBC Capital Markets seconded that opinion, repeating an “Outperform” rating and a target of $300. The company noted the fast pace of AWS increase and an increasing backlog as among the supports to the investment case, despite capex remaining elevated.

Generally, analysts are mostly bullish with a holding consensus “Strong Buy” rating with a mean price target around $297, which implies a 40% upside case.

So, in my opinion, the current selloff is the golden opportunity to buy in because Amazon’s long-term investments in AWS, AI infrastructure, and logistics should convert into durable revenue and margin expansion as capacity is monetized over the next several years.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Analyst Has Finally Had Enough of AI CapEx at Microsoft. Should You Be Done with MSFT Stock Too?

- The Shocking Reason This Analyst Says Michael Saylor and MicroStrategy Stock Will Take Bitcoin Prices to $0

- Google Gemini Is Just Getting More Popular. Does That Make GOOGL Stock a Buy Here?

- Should You Buy the Post-Earnings Dip in Amazon Stock?