AppLovin (APP) has weathered short-seller storms before, rebounding from 2025 attacks by Fuzzy Panda, Culper Research, and Muddy Waters that questioned its financials and led to sharp but temporary drops of 12% to 20%. Those reports fizzled as the company pushed back and growth continued, with shares doubling over the year.

However, the latest report from CapitalWatch, released last month, accuses AppLovin of serving as a "digital laundromat" for transnational criminals, laundering billions through ad fees from illicit apps tied to Ponzi schemes and fraud rings. This one hit harder, sending shares down 32% in the week following the report.

On Feb. 4, APP stock tumbled another 16% to around $385, but the slide doesn't seem directly linked to the money-laundering claims, which the company has vehemently denied as “false” and "conspiratorial." Instead, broader market fears are at play, signaling deeper troubles for the ad-tech player beyond activist investor noise.

About AppLovin Stock

AppLovin is a mobile technology firm that builds software platforms to help app developers market, monetize, analyze, and publish their content. Its core offerings include MAX, an in-app bidding tool for optimizing ad inventory; AppDiscovery for matching advertiser demand with publisher supply; Adjust for app marketing analytics; and Wurl for connected TV advertising and content distribution.

Headquartered in Palo Alto, California, the company appears well-positioned for sustained growth through its end-to-end AI-driven solutions, expanding beyond mobile gaming into broader digital advertising and global audience scaling amid rising app economies.

However, 2026 has been brutal so far, with shares down 43% year-to-date (YTD), well-underperforming the S&P 500's ($SPX) less than 1% loss. This follows a stellar 2025 where APP stock doubled on strong revenue growth.

Valuation metrics paint a mixed picture: The trailing price-to-earnings (P/E) ratio stands at 56.9, above the software industry average of around 45 but below AppLovin's historical peaks during hype cycles, indicating premium pricing for its growth story. Meanwhile, the forward P/E of 30.4 suggests expectations of earnings expansion, while the forward price-to-sales (P/S) ratio of 21.1 times is elevated compared to the industry's 10-to-15 range. That reflects optimism in AppLovin's ad-tech dominance but vulnerability to slowdowns. Lastly, the PEG ratio of 1.5 implies the stock is fairly valued when accounting for projected growth rates of over 100% in earnings.

Overall, AppLovin appears neither grossly overvalued nor undervalued, but its high multiples leave little room for error in a volatile market.

The Market Thinks AppLovin Has Bigger Problems

While AppLovin's downward spiral might have started with CapitalWatch's report, the real catalyst hit on Jan. 29, when Alphabet's (GOOGL) Google unveiled Project Genie, an AI-powered platform for creating virtual reality games. Investors panicked, viewing it as a direct assault on the gaming ecosystem where AppLovin thrives. After all, the firm's mobile ad-tech business heavily relies on game developers for revenue through tools like MAX, which optimizes in-app ads. Shares plunged 17% in the following session alone, dragging peers like Unity Software (U), Roblox (RBLX), and Take-Two Interactive (TTWO) lower as well.

Analysts noted the overreaction, as Project Genie focuses on game creation rather than ad monetization, but the fear lingers. If AI democratizes game development, it could flood the market with low-quality apps, diluting ad inventory value and compressing margins for platforms like AppLovin.

This ties into a broader AI threat looming over ad-tech. As generative AI advances, it's reshaping software valuations by automating processes that once required human input, potentially disrupting AppLovin's core model. For instance, AI could enable more precise, automated ad targeting without intermediaries, eroding the need for auction-based systems like AppDiscovery.

Competitors like Meta Platforms (META) and Google are already integrating AI to refine their ad ecosystems, putting pressure on AppLovin's 83% to 84% EBITDA margins. The stock's 30% January drop — making it the S&P 500's worst performer — reflects this existential worry, compounded by sector-wide AI skepticism.

While AppLovin is pivoting toward AI-enhanced tools, such as its Axon algorithm for better ad personalization, the transition risks short-term revenue hits if developers shift to in-house or rival solutions. Market sentiment suggests these structural shifts, not just short-seller drama, are the true drivers sending shares careening, with potential for further volatility if fourth-quarter earnings disappoint or 2026 guidance underwhelms.

What Do Analysts Expect for AppLovin Stock?

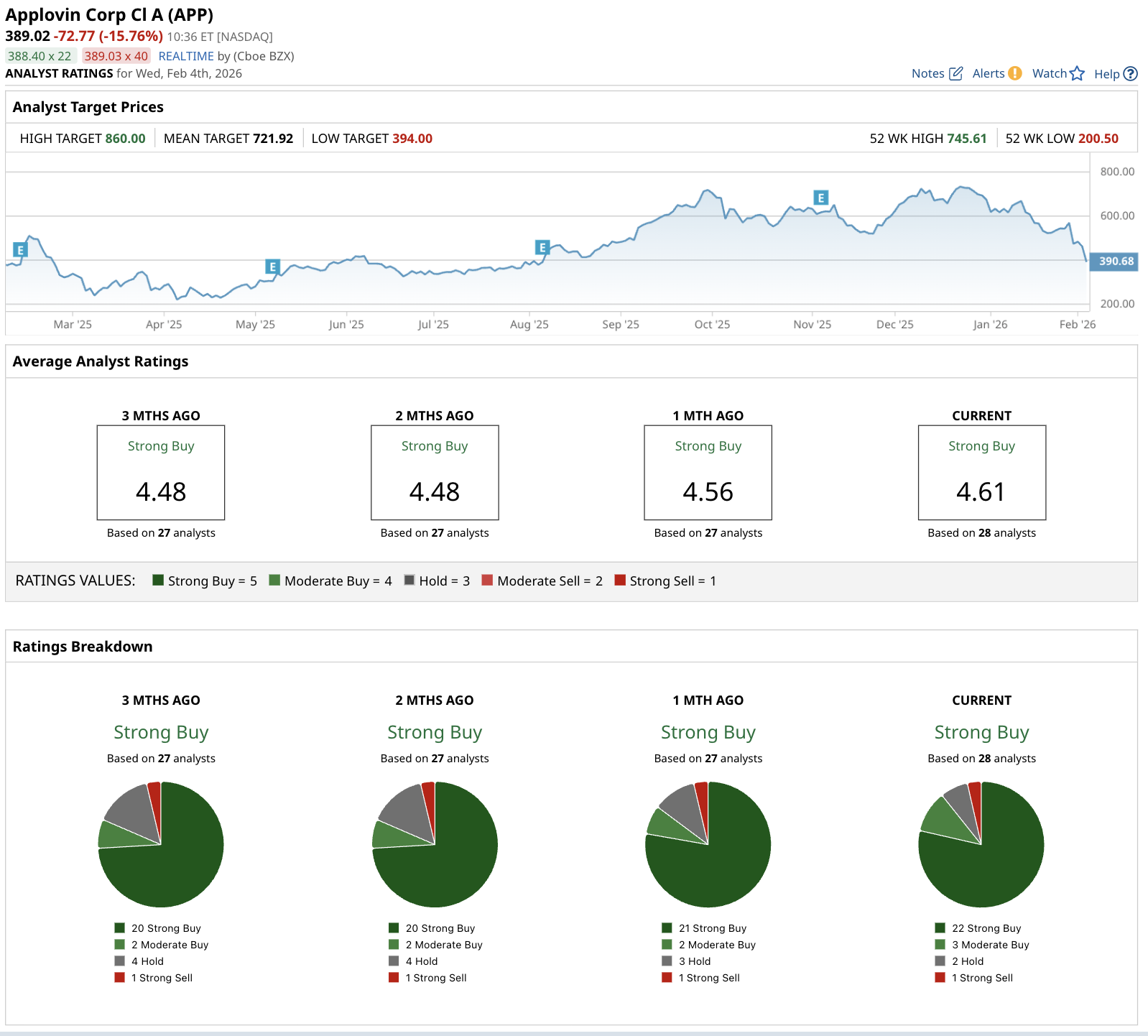

Despite the turmoil, Wall Street remains bullish on AppLovin. APP stock has a consensus rating of "Strong Buy" based on input from 28 analysts, with a breakdown of 22 "Strong Buy" ratings, three “Moderate Buy” ratings, two "Hold" ratings, and one "Strong Sell." This reflects optimism in the company's AI pivot and growth potential as one firm upgraded from "Hold" to "Moderate Buy" in January despite the AI and short-seller fallout. Overall, Wall Street's opinion has held steady, with upward revisions in earnings estimates over the past month.

The mean price target of $721.92 represents potential upside of 95%. At the current share price around $370, this implies that analysts see plenty of room for recovery if AppLovin delivers on Q4 results and navigates AI disruptions effectively.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Analysts Forecast 50% Upside, Is Now the Time to Buy the Dip in AMD?

- This Overlooked Biotech Giant Could Surprise Investors This Quarter

- Peloton Stock Just Plunged Into Oversold Territory. Should You Buy the Dip or Stay Far, Far Away?

- Josh D’Amaro Is the New Disney CEO. Should You Buy, Sell, or Hold DIS Stock Here?