Based in Springfield, Missouri, O'Reilly Automotive, Inc. (ORLY) ranks among the premier automotive aftermarket retailers. Valued at approximately $78.3 billion, it equips professional repair shops and do-it-yourself customers with replacement parts, maintenance supplies, tools, equipment, and private-label products

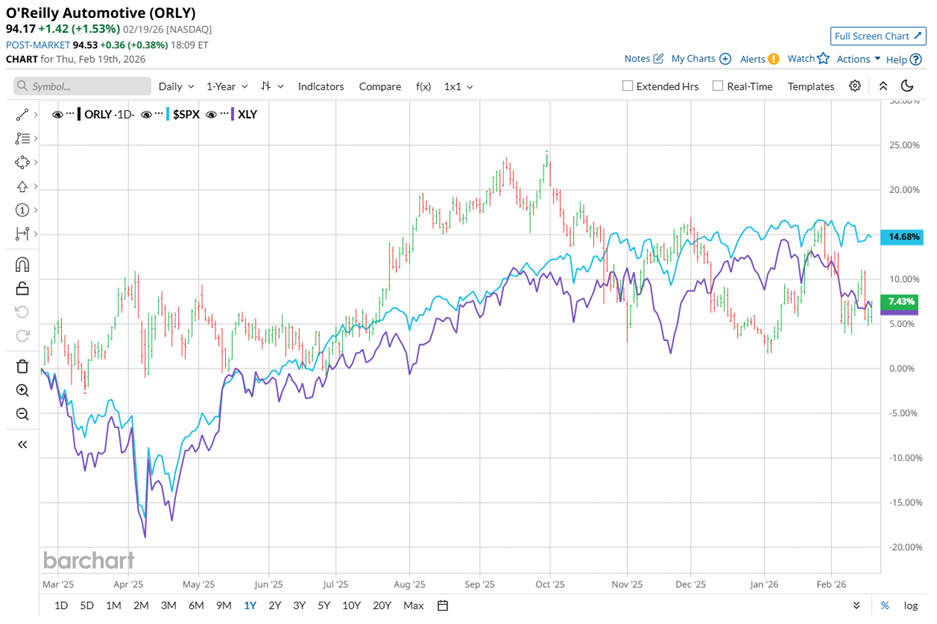

Over the past 52 weeks, O'Reilly’s shares have risen nearly 9%, slightly trailing the S&P 500 Index ($SPX), which gained 11.7% over the same period. Year-to-date (YTD), the stock has climbed 3.3%, neatly outpacing the broader index’s modest uptick.

Compared with its sector, the State Street Consumer Discretionary Select Sector SPDR ETF (XLY) climbed 2.8% over the last 52 weeks but dropped 2.7% YTD, highlighting O'Reilly's relative stability amid sector volatility.

On Feb. 4, ORLY stock edged lower and then slid another 4% the next day after O'Reilly posted its Q4 fiscal 2025 earnings results. During the quarter, revenue rose 7.8% year over year to $4.41 billion, essentially in line with the $4.39 billion analyst estimate. EPS came in at $0.71, just shy of the $0.72 estimate. However, it grew 12.7% from the year-ago period.

Still, the quarter carried more muscle than the headline suggested. Comparable store sales rose a robust 5.6% in Q4, pushing full-year 2025 comps to 4.7%, which reached the high end of revised guidance.

Management also set a confident tone for fiscal 2026, guiding EPS to a range of $3.10 to $3.20, which implies 6.1% growth at the midpoint over 2025. Growth does not stop at earnings. The company plans to open 225 to 235 net new stores in 2026, including expansion into Canada.

For the full fiscal year 2026, ending in December, analysts expect diluted EPS to grow 8.1% year over year to $3.21. While O'Reilly beat EPS estimates in two of the past four quarters and missed in the other two, it has consistently operated within a close range of expectations.

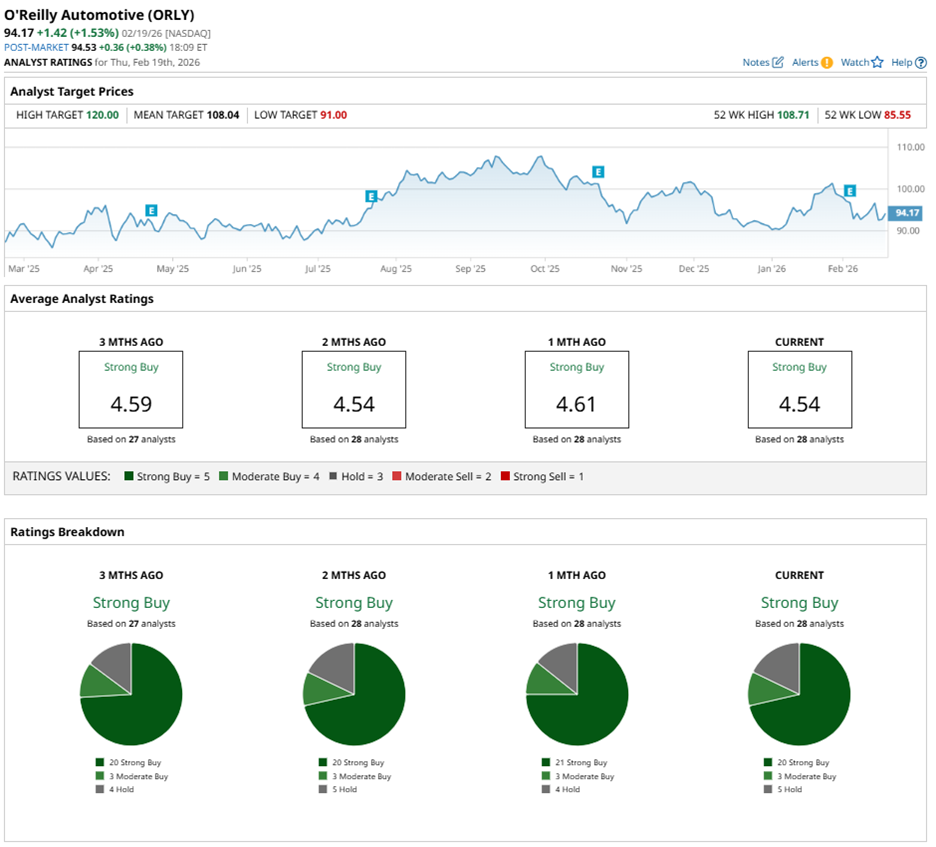

Wall Street continues to assign ORLY stock an overall rating of “Strong Buy.” Of the 28 analysts covering the stock, 20 recommend “Strong Buy,” three suggest “Moderate Buy,” while five call for “Hold.”

Sentiment has remained mostly unchanged from three months ago, when 20 analysts also assigned the stock a “Strong Buy” rating.

Recent analyst actions add further texture. On Feb. 6, Michael Baker of DA Davidson reiterated his “Buy” rating and maintained a $110 price target, underscoring continued faith in execution.

On Feb. 10, Steven Zaccone of Citigroup Inc. (C) also maintained a “Buy” rating, though he trimmed the price target from $114 to $110, signaling a slightly more cautious valuation stance while preserving confidence in the company’s trajectory.

Importantly, upside potential still frames the broader narrative. ORLY’s average price target of $108.04 represents potential upside of 14.7%. Meanwhile, the Street-high target of $120 suggests a gain of 27.4% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Kraft Heinz Pauses Its Breakup Plans. Should You Buy the High-Yield Dividend Stock Here?

- Nvidia Dumped Recursion Pharmaceuticals Stock. Should You?

- Etsy Stock Breaks Above Its 20-Day Moving Average on Depop Sale. Does That Make ETSY a Buy Here?

- As Apple Tests AI Devices, Should You Buy AAPL Stock Here?