Netflix (NFLX) is a leader in the streaming space. While the company continues to deliver solid operating performance, its stock has lagged the broader market over the past year.

Over the past 12 months, Netflix shares have lagged the broader market, falling roughly 20% while the S&P 500 ($SPX) gained more than 14%. The stock is also trading about 39% below its 52-week high of $134.12, reflecting a sharp pullback.

Valuation has been a concern, particularly after the strong run-up that preceded the recent decline. Further, the uncertainty surrounding Netflix’s potential acquisition of Warner Bros. Discovery (WBD) has weighed on the stock price. More recently, the stock came under pressure after management flagged higher spending in 2026.

During the fourth-quarter earnings call, Netflix outlined plans to broaden its entertainment offerings while investing further in product and commerce capabilities. Although these initiatives will drive long-term revenue growth, a higher expense forecast adversely impacted its share price.

Despite the challenges, Netflix’s underlying fundamentals remain intact. The company continues to execute well operationally, retaining its leadership position in streaming, steadily growing its subscriber base, and expanding its advertising business. With that in mind, here are three reasons why NFLX stock is a buy now.

Netflix Stock Entered Oversold Territory

Netflix's stock has slipped into what technical analysts call “oversold territory.” Oversold conditions are typically identified using the Relative Strength Index, or RSI, which indicates whether a stock is overbought or oversold. When the RSI falls below 30, it generally signals that selling pressure has been excessive.

In Netflix’s case, the weekly RSI has dropped to 26.8, placing the stock firmly in oversold territory. This contrasts with peers such as Walt Disney (DIS), whose RSI currently sits at 48.2.

An RSI reading at these levels suggests that a large portion of the negative sentiment may already be reflected in the stock price. While oversold conditions do not guarantee an immediate rebound, they can indicate that downside momentum is weakening. For investors, this setup may signal that selling pressure is becoming exhausted, potentially opening the door to a period of stabilization or renewed buying interest.

Netflix to Deliver Strong Earnings

Netflix is set to deliver another year of strong earnings growth in 2026, even as management continues to invest in content and product. The company’s fundamentals remain compelling, supported by rising membership, pricing power, and a rapidly scaling advertising business.

Viewer engagement remains robust, driven by a strong slate of original programming and a broader mix of licensed titles. High engagement will support subscriber growth and help improve retention. Pricing remains another key lever. With a loyal and engaged audience, Netflix continues to demonstrate pricing power, which should translate into higher revenue and profit.

At the same time, advertising is emerging as a meaningful growth engine. Ad revenue surged to $1.5 billion in 2025, and management is targeting roughly $3 billion in ad sales in 2026.

Importantly, Netflix is investing in growth opportunities while expanding margins. The company is targeting operating margins of 31.5% in 2026, up 200 basis points, while keeping content spend growing more slowly than revenue. This approach supports margin expansion and strong profit growth.

Management forecasts 2026 revenue of $50.7 billion to $51.7 billion, implying 12% to 14% growth, while analysts expect earnings per share to rise more than 23%.

Netflix’s Valuation Looks Reasonable

The pullback in NFLX stock has eased valuation concerns. The stock trades at roughly 26.3 times forward earnings, which is justified considering more than 23% EPS growth is forecast for 2026, followed by another increase of over 21% in 2027.

At the same time, the company’s advertising-supported tier is gaining traction, opening up a meaningful new revenue stream. Moreover, Netflix’s proven ability to raise prices without significantly impacting demand points to sustained earnings momentum.

The Bottom Line on NFLX Stock

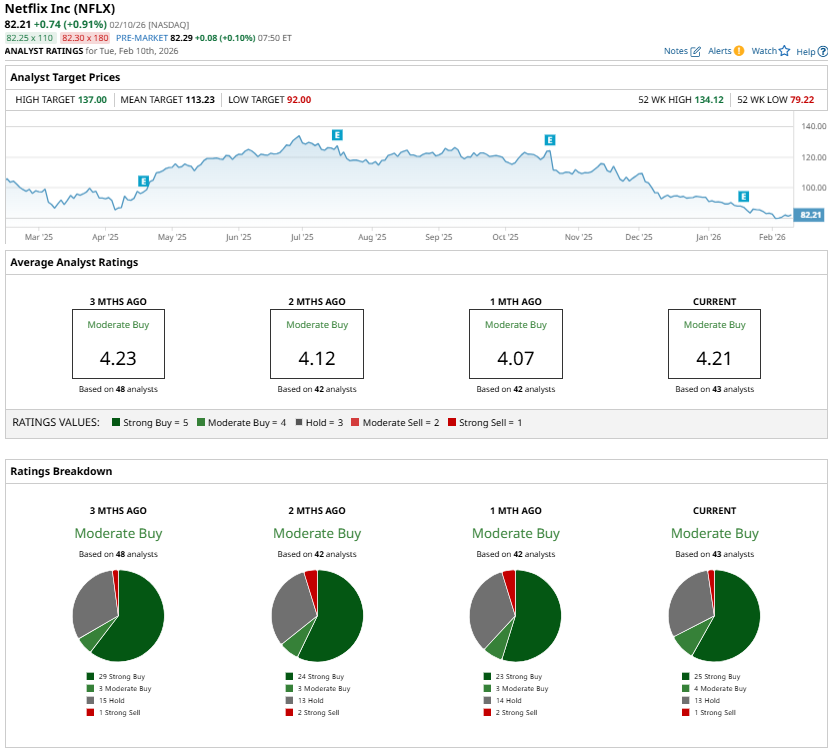

Analysts maintain a “Moderate Buy” consensus rating on NFLX stock. However, with the stock in oversold territory, earnings growth expected to remain strong, and a reasonable valuation, Netflix’s risk-reward looks attractive.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Astera Labs Plunges Below Key Support Levels. Should You Buy the Dip in ALAB Stock?

- Can a New CEO Save Workday Stock from the Software Apocalypse?

- A Crypto Collapse Sends Robinhood Stock Back into Oversold Territory. Should You Buy the Dip?

- Unity Software Stock Is Back in Oversold Territory. Is There Any End in Sight for the Bloodshed in U Shares?