Tesla (TSLA) is facing a tough week, as its claim to be the global leader in electric vehicle (EV) sales no longer holds water. The company has been surpassed by Chinese EV maker BYD (BYDDY), which sold more than 2 million battery-powered vehicles in 2025. Meanwhile, Tesla sales dropped 9% from a year ago, falling to 1.64 million.

Michael Burry, the former hedge fund manager who bet against the housing market as documented in the film “The Big Short,” has said shares of Tesla are “ridiculously overvalued.” However, Burry said in a separate post that he’s not shorting TSLA stock.

Is Tesla a good long-term bet now? Or should investors be looking to take profits or embracing a short-term strategy?

About Tesla Stock

Tesla is facing a lot of heat — a study by economists at Yale University estimates that the carmaker lost at least 1 million sales from October 2022 to April 2025 because of CEO Elon Musk’s political activities. In addition, the company is being hurt by the expiration of the $7,500 federal tax credit on EV sales.

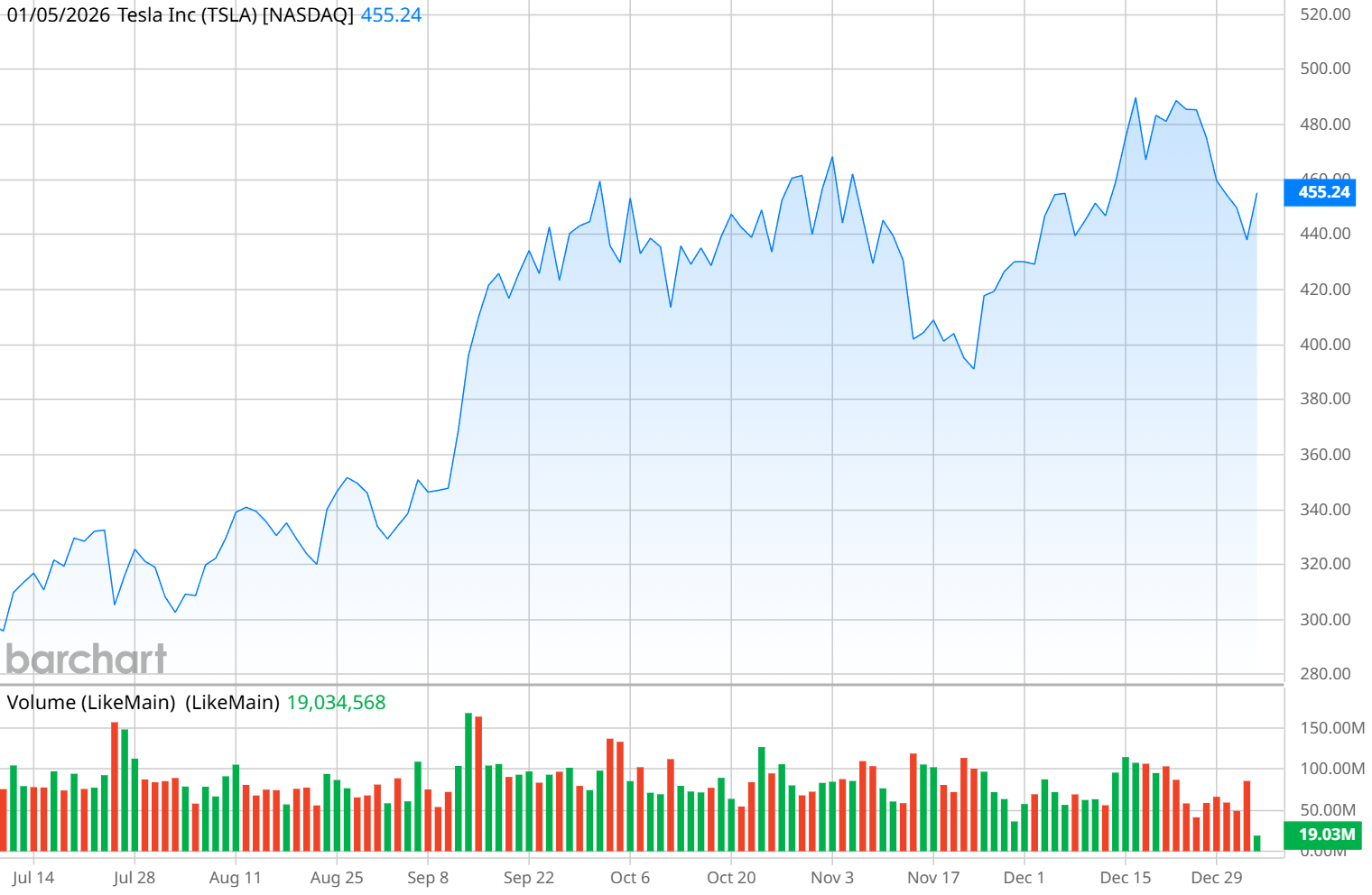

That tension is reflected in the company’s stock performance. Shares are up 5% in the last year, but that’s underperforming the S&P 500 ($SPX), which has seen a 16% gain in the last 12 months. That’s a troubling trend, particularly when you consider that Tesla is a member of the “Magnificent Seven” grouping of stocks, whose valuation makes up more than a third of the entire index. Members of that group historically outperform the index, but in the last year, Tesla has not carried its weight.

On top of that, Tesla has an eye-watering valuation, with its forward price-to-earnings (P/E) ratio currently at 251. Tesla has always been expensive, as there’s a lot of enthusiasm priced into TSLA stock, but even its hefty five-year P/E is a bargain compared to the current valuation.

Tesla Misses on Earnings

Tesla’s third-quarter earnings report was a mixed bag. On the one hand, revenue was a record at $28.1 billion, up from $25.2 billion a year ago. However, Tesla reported an earnings miss, as EPS of $0.50 per share was 4 cents lower than what analysts had expected.

The issue comes with margins. While Tesla set a record in Q3 for the number of vehicles delivered with 497,099 (attributed to buyers rushing to make purchases before the tax credit expired Sept. 30), its profit margin dropped from 10.8% a year ago to 5.8% in the quarter. Net income was also down.

In addition, Tesla announced last week that it delivered 418,227 vehicles, a sharp decline from 495,570 a year ago. For the full year, Tesla’s 1.63 million deliveries were down from 1.78 million in 2024.

The company plans to issue its financial report for the fourth quarter and full year after the market closes on Jan. 28. Tesla did not issue guidance for the fourth quarter, but analysts are expecting EPS of $0.34 per share, which would be down 48% from a year ago.

What Should You Expect From Tesla Stock?

Tesla is an interesting company. While it has made its mark as a maker of EVs, the company is much more than that — and that’s reflected in the valuation.

Tesla is developing its own Full Self-Driving (FSD) software as part of a comprehensive artificial intelligence (AI) platform that Musk believes will result in a fleet of self-driving cars. The company is making what it calls the Tesla Cybercab, which is a two-passenger self-driving EV that Musk plans to be fully autonomous. Its Robotaxi app is also now available to Tesla users in the U.S. and Canada, in hopes that Tesla will gain widespread approval for self-driving technology. Additionally, Tesla is developing the Optimus autonomous robot, which Musk claims will one day be capable of performing daily tasks in homes and factories.

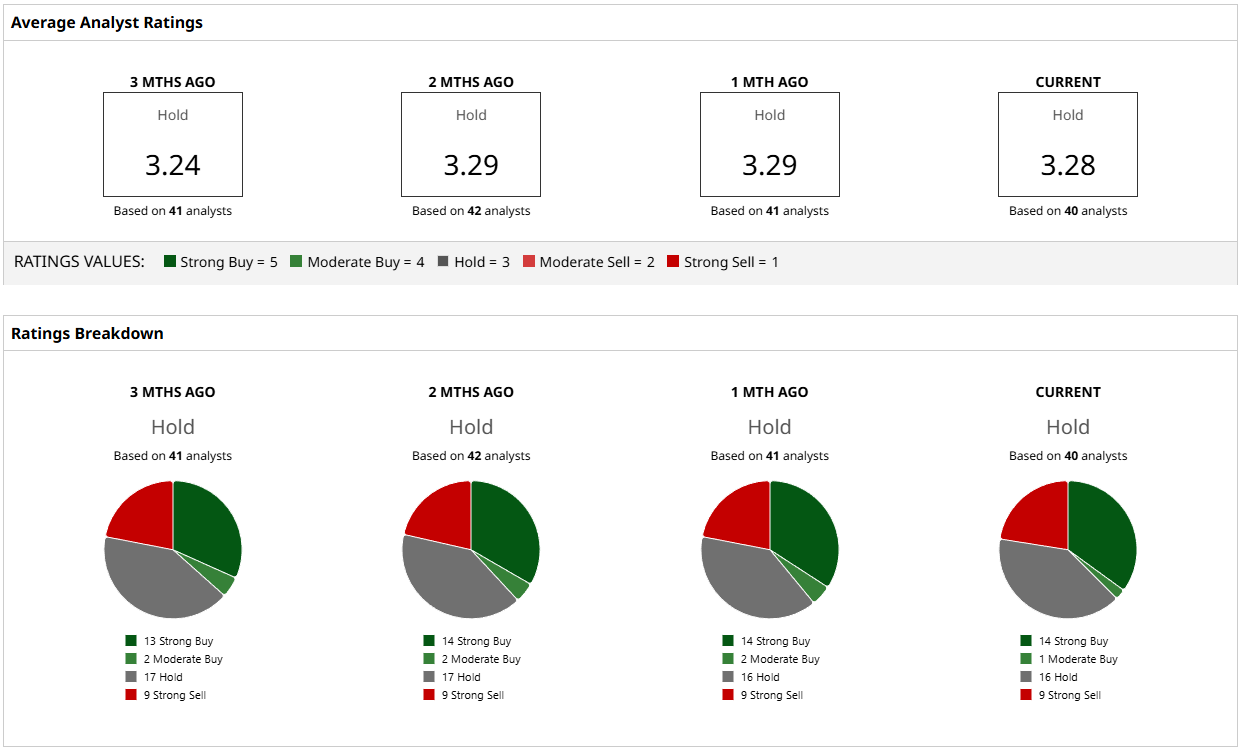

Both of these ideas are still a ways off, although Musk says the Cybercab will enter production later this year. All of this puts Tesla at a crossroads for investors. Analysts are split on the company’s prospects. Based on 40 analysts with coverage, 14 analysts have a “Strong Buy” rating, one analyst has a “Moderate Buy,” 16 suggest a “Hold” rating, and nine analysts have a “Strong Sell” rating.

Price targets for TSLA stock range from $120 to $600, with the low target signifying a potential 72% drop and the high target suggesting a gain of 39% from today’s prices.

The Bottom Line

In the end, investing in Tesla has more to do with the AI technology than with the number of vehicles it will deliver. Autonomous driving (AD) technology could be revolutionary, particularly if Tesla vehicles around the country also become able to operate as robotaxis. That’s why the stock continues to carry such a high P/E ratio — and why Burry calls it overvalued.

Now that Musk has left Washington and is back to running the company without distraction, Tesla has a much better chance of success. But investing in TSLA stock at this price has inherent risks. Investors should be mindful of their risk tolerance before taking a position.

On the date of publication, Patrick Sanders did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart