President Donald Trump's renewed push for nuclear energy at the World Economic Forum in Davos has sparked fresh optimism across the nuclear sector. The Trump administration plans to seek interest from states as soon as this week on storing nuclear waste in exchange for incentives to build new reactors, marking a significant shift in addressing one of the industry's biggest challenges.

The move tackles a critical bottleneck that has stalled nuclear expansion for decades. Radioactive waste currently sits in temporary storage at nuclear power plants across the country. A previous plan to centralize storage at Yucca Mountain in Nevada collapsed under President Barack Obama due to fierce local opposition.

At Davos, Trump emphasized that nuclear power can be developed at competitive prices while maintaining safety standards. Notably, the U.S. has outlined targets to quadruple U.S. nuclear capacity to 400 gigawatts by 2050.

Electricity demand is expected to surge over the next two decades, driven by the artificial intelligence (AI) megatrend and broader economic growth. Here are two companies that stand out as top-rated investment opportunities, given the nuclear energy market's expansion.

Is Encore Energy Stock a Good Buy?

Encore Energy (EU) is engaged in the acquisition, exploration, development, and extraction of uranium resource properties in the United States. Encore Energy has positioned itself as a pure-play domestic uranium producer at exactly the right moment.

The company operates extraction facilities in South Texas using proven in-situ recovery technology, with operations already underway at both the Rosita and Alta Mesa processing plants. This puts Encore ahead of most competitors still stuck in the exploration phase.

The Trump administration's aggressive nuclear expansion plans create a tailwind that could last decades. Two executive orders issued in January 2025 designated uranium as a critical mineral and an energy resource.

U.S. Secretary of Energy Chris Wright has signaled support for expanding the strategic uranium reserve. Moreover, the U.S. Department of Energy has launched a pilot program to accelerate advanced reactor development and strengthen domestic fuel supply chains.

The supply-demand fundamentals look compelling. The world's 439 operating nuclear reactors need roughly 175 to 180 million pounds of uranium oxide annually. The gap has been filled by dwindling stockpiles and secondary supplies that experts believe are running low.

Meanwhile, reactor recommissioning is accelerating in the United States. Plants like Palisades, Three Mile Island, and Diablo Canyon are returning to service after premature shutdowns, adding to baseline demand. Encore's development pipeline extends beyond Texas to projects in South Dakota and Wyoming, providing growth optionality as the market expands.

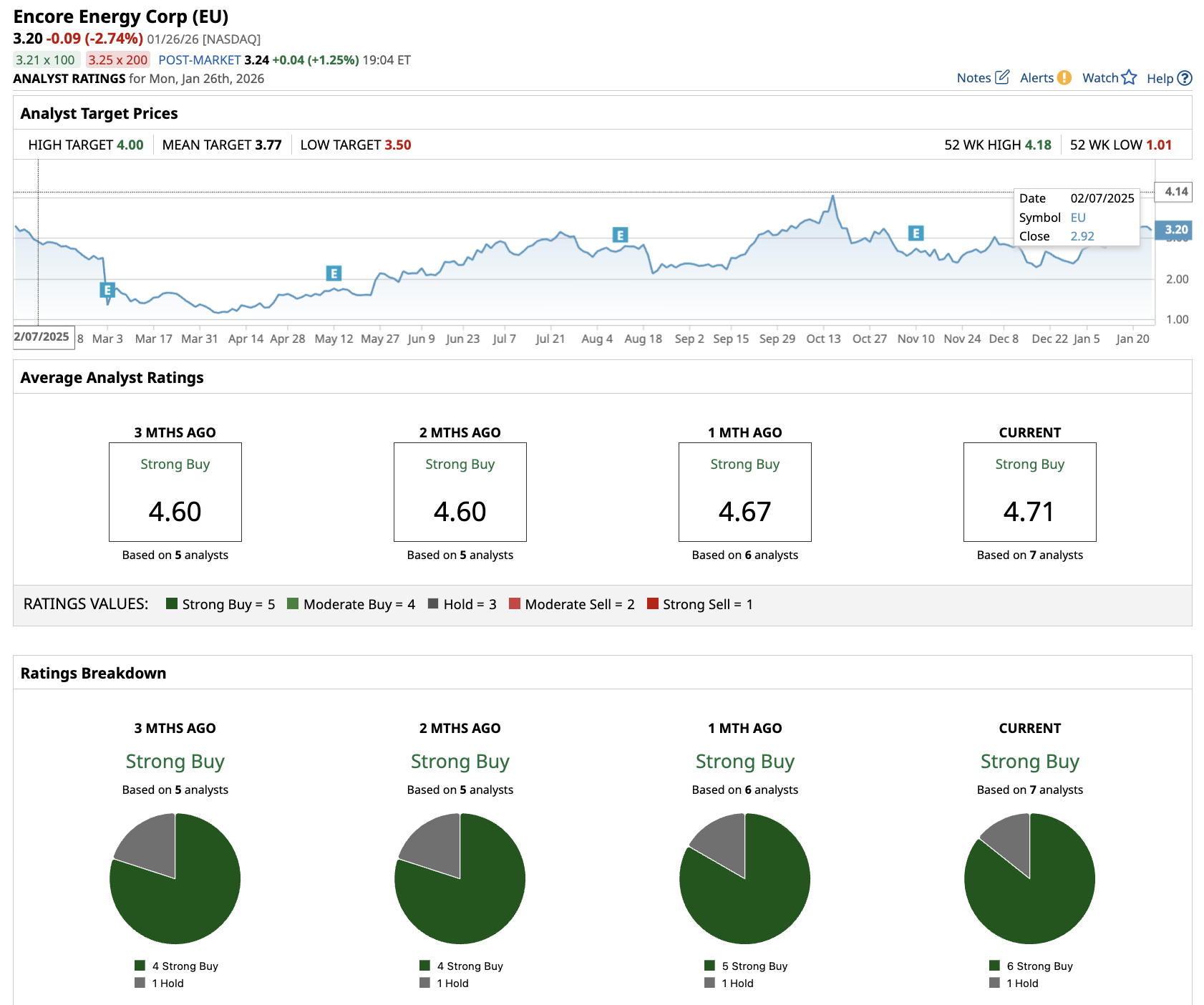

Out of the seven analysts covering EU stock, six recommend a “Strong Buy" rating while one recommends a “Hold” rating. The average Encore Energy stock price target is $3.77, which is slightly above the current price of $3.64.

Is ASP Isotopes Stock a Good Buy?

ASP Isotopes (ASPI) is a high-risk, high-reward investment in the nuclear energy sector, as commercial production is beginning to materialize. ASP began commercial operations at two enrichment facilities in South Africa during the first half of 2025. This marked a transition from the development stage to actual revenue generation. The first commercial shipment of enriched Carbon-12 is expected in the fourth quarter of 2025, followed by Silicon-28 in early 2026.

The company's proprietary technologies tackle a critical bottleneck in nuclear energy expansion. Its Aerodynamic Separation Process and Quantum Enrichment technology enable production of high-assay low-enriched uranium, the fuel needed for next-generation small modular reactors.

With the Trump administration pushing aggressive nuclear expansion and the Department of Energy launching pilot programs to expand domestic fuel production, ASP Isotopes sits at the center of efforts to reduce dependence on Russian uranium supplies.

The business model extends beyond nuclear fuel into high-value medical isotopes and semiconductor materials. ASP also produces Ytterbium-176 for cancer treatments and is developing Silicon-28 for quantum computing applications.

In the first nine months of 2025, ASP Isotopes reported net losses of $96.5 million, up from $23.2 million in the year-ago period. The company also raised more than $100 million via equity offerings last year to support cash burn rates.

Analysts tracking ASPI stock forecast revenue to increase from $9.2 million in 2025 to $513 million in 2029. The firm is forecast to report adjusted EPS of $1 in 2029, compared to a loss of $1.25 in 2025.

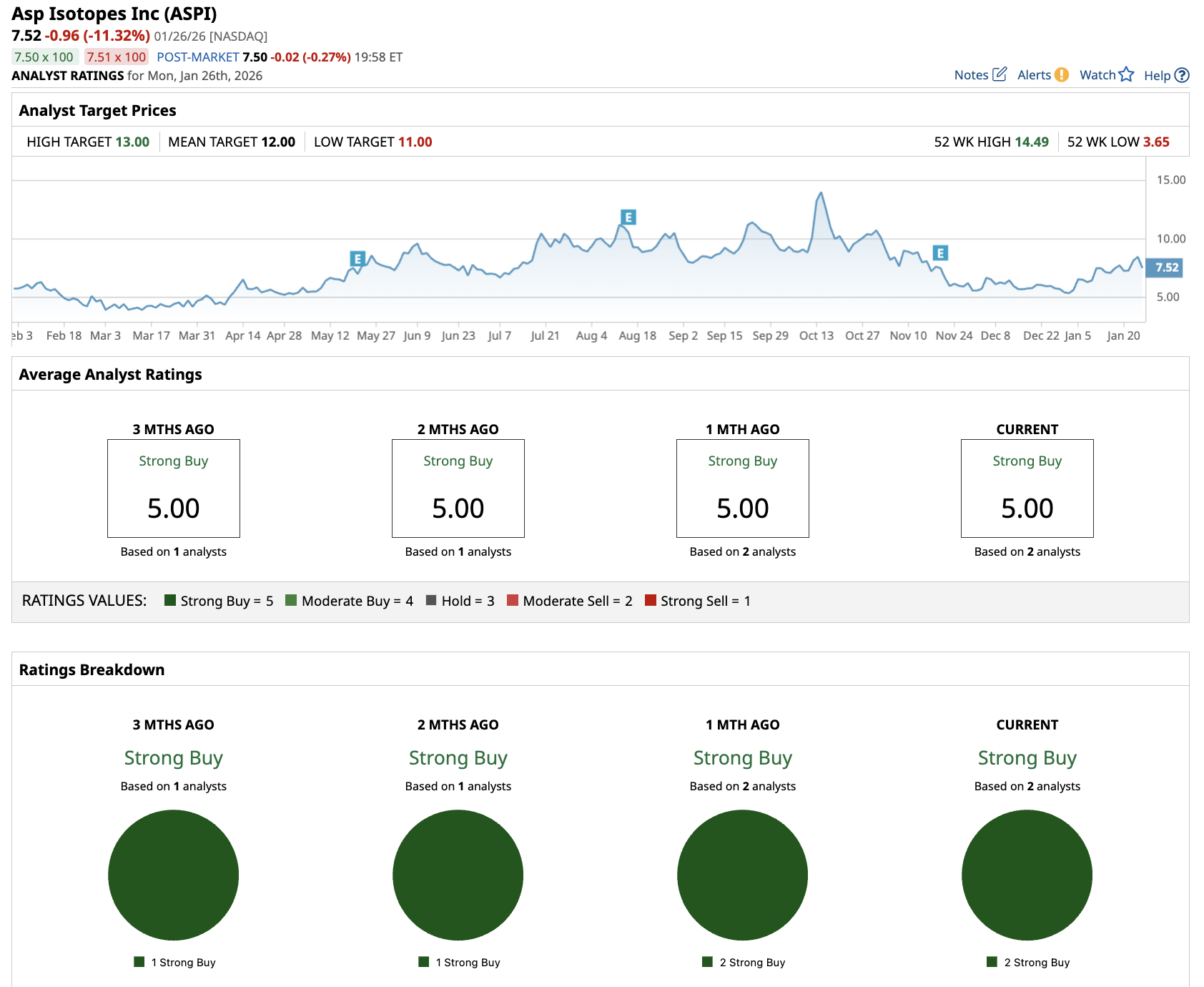

The two analysts tracking ASPI stock recommend a “Strong Buy" rating. The average ASPI stock price target is $12, indicating potential upisde of more than 50% from current levels.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Why the Smart Money is Pensive Ahead of Exxon Mobil’s (XOM) Q4 Earnings Report

- 2 Top-Rated Nuclear Energy Stocks to Buy as Trump Talks Nuclear Waste

- Natural Gas Prices Just Hit $6. How Much Higher Will They Go Here Amid Winter Storm Fern?

- Our Top Technical Strategist Explains How to Invest in the 'Age of Electricity'