Semiconductor stocks have been on a tear lately, driven by booming artificial intelligence (AI) demand and data-center spending. In 2025 alone, Nvidia (NVDA) jumped about 30% and Intel (INTC) stock rose more than 80%. Specialized chip suppliers also saw eye-popping gains. Among the clear leaders has been Taiwan Semiconductor Manufacturing Company (TSM), the world’s largest contract chipmaker. The company is benefiting directly from accelerating AI adoption by key customers such as Nvidia and Apple (AAPL).

That sector-wide strength has flowed through the supply chain, boosting orders and revenues at leading foundries such as TSMC. Last week, Taiwan Semiconductor reported a robust 20% year-over-year (YOY) jump in fourth-quarter revenue, beating market expectations and reinforcing its growth narrative.

As momentum carries into 2026, investors are increasingly asking whether TSM stock still has room to run.

About TSMC Stock

Founded in 1987, Taiwan Semiconductor pioneered the pure-play foundry model and is now the world’s largest contract chipmaker. It produces advanced logic chips for customers such as Nvidia, Apple, and AMD (AMD) using leading-edge nodes like 3 nanometer (nm) and 5 nanometer, placing it at the center of the global AI and data-center supply chain.

That position is being reinforced by heavy investment. TSMC is reportedly planning NT$450 billion to NT$500 billion in Taiwan capex for 2026, including new fabs and advanced packaging sites to ease tight supply at 3nm and future nodes. The company has also started work on its first 1.4nm fab, targeted for production in 2028, while raising its 2025 capex guidance to $40 billion to $42 billion.

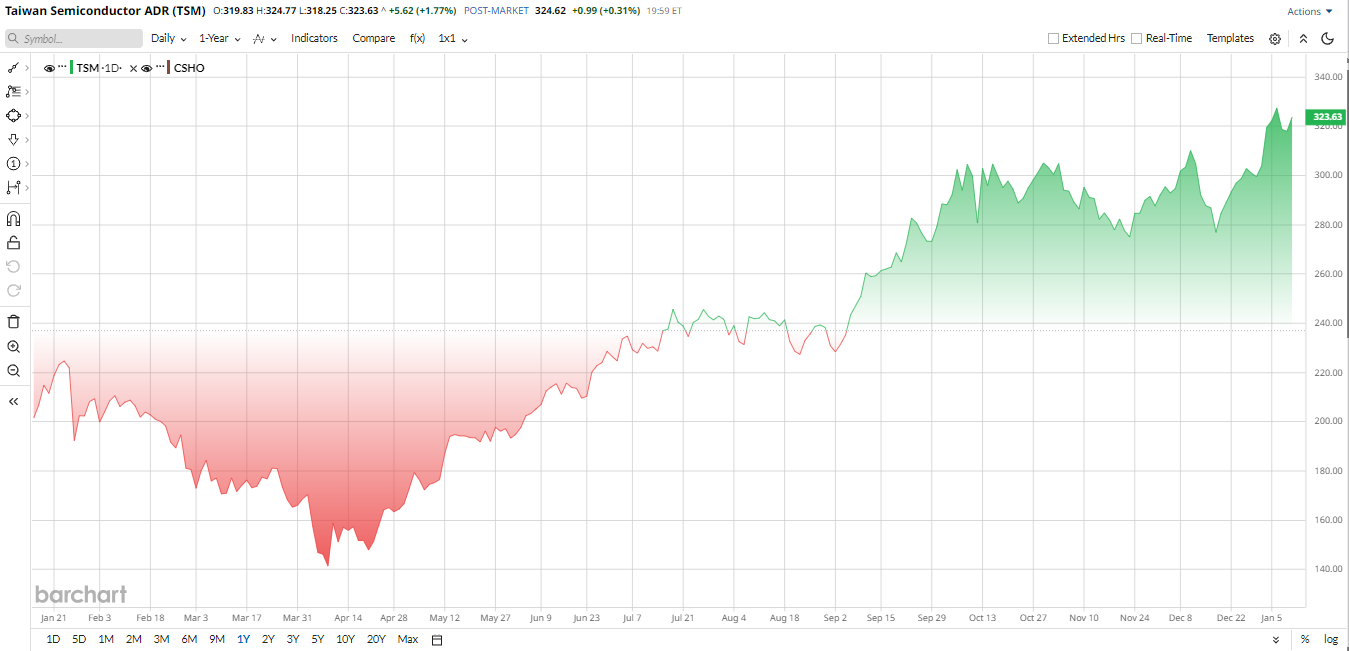

Demand trends remain supportive. Apple and AMD are said to be expanding wafer orders into 2025 and 2026, helping drive strong stock performance. Over the past year, shares have climbed 65%, far outpacing the S&P 500 ($SPX).

TSMC is not a bargain, however. Its current forward price-to-earnings (P/E) ratio is at 26 times and the EV/EBITDA multiple is around 16 times. These multiples are high by broad industry standards, reflecting TSMC’s premium positioning and growth prospects. For context, many semiconductor peers trade in the mid-teens on a forward P/E basis. In other words, TSM stockk’s valuation is roughly in line with, or slightly above, the sector median. That said, the stock looks fairly valued given its dominant market share and growth runway, rather than deeply cheap.

TSMC Q4 Revenue Jump and Outlook

Just a few days ago, TSMC gave investors a solid preview of its fourth-quarter performance. The company said that Q4 revenue reached NT$1.046 trillion, or about $33.1 billion, up 20% from a year earlier. That result beat consensus expectations and landed squarely within management’s prior guidance range.

According to the company, surging demand for AI chips more than offset lingering weakness in consumer electronics. The strong update prompted several analysts to lift their 2026 revenue forecasts, shifting attention to the Jan. 15 earnings call for updated guidance.

Profitability should also look healthy. Analysts expect Q4 earnings to rise meaningfully, supported by gross margins near 60%. Free cash flow remains a major strength, with roughly $28 billion generated over the past 12 months and a cash-rich balance sheet that supports heavy investment and shareholder returns.

Looking ahead, Wall Street expects conservative but upbeat Q1 guidance and strong full-year 2026 growth, driven by AI demand. CEO C.C. Wei has repeatedly emphasized that AI demand remains stronger than expected, a message investors will be listening for again on Jan. 15.

Analyst Commentary and Targets for TSMC

Wall Street has turned sharply bullish on TSM stock. Notably, Goldman Sachs boosted its price target by 35% to NT$2,330 in early January, calling AI “a multi-year growth engine” for TSMC. JPMorgan followed with a raise to NT$2,100, forecasting roughly 30% revenue growth in 2026 thanks to AI demand.

Morgan Stanley also upgraded its view on Dec. 18, hiking its target to NT$1,888 and reaffirming an “Overweight” rating. Morgan Stanley analysts noted that higher wafer prices and strong AI chip orders should drive better-than-normal Q1 2026 revenues.

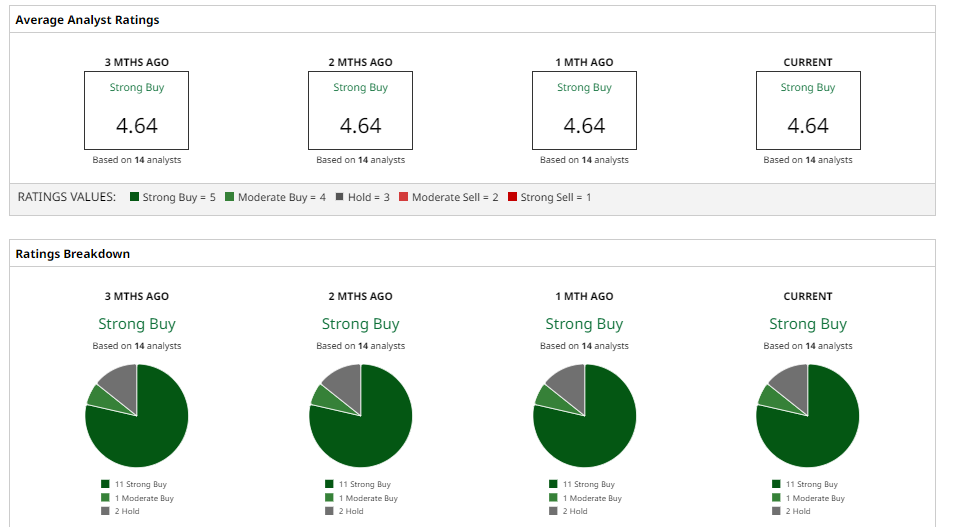

Analysts emphasize TSMC’s dominant node leadership, improving margins and long cycle of capex from AI. That is a contrast to peers like Intel, which is lagging in advanced process technology. Across the board, the consensus among 14 analysts tracked by Barchart is a “Strong Buy." The mean price target is $352.67, which implies about 6% upside potential.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Up 32% in the Past Year, Can Microchip Technologies Stock Keep Zooming Higher?

- Worried About Nvidia’s China Business? CEO Jensen Huang Says This Is the Top Indicator to Watch.

- Revenue Keeps Growing at Taiwan Semi. Should You Load Up on TSM Stock for 2026?

- As Goldman Sachs Issues a Warning on Super Micro Computer Stock, Should You Risk Buying the Dip?