With a market capitalization of $86.95 billion, O’Reilly Automotive, Inc. (ORLY) is one of the largest specialty retailers of automotive parts, tools, and accessories in the U.S. Headquartered in Springfield, Missouri, it operates thousands of stores serving both professional mechanics and do-it-yourself customers, offering everything from replacement parts to maintenance supplies.

O’Reilly’s stock has quietly turned into one of the market’s steady outperformers. Over the past 52 weeks, the company’s shares have gained 25% and they are up by 27% on a YTD basis. The stock has broadly outperformed the S&P 500 Index ($SPX), which has gained 11% and 12.3% over the same periods, respectively.

The stock has also outpaced the Consumer Discretionary Select Sector SPDR Fund (XLY), which has gained 4.9% over the past 52 weeks and marginally in 2025.

O’Reilly has outpaced the market largely because it continues to deliver steady, reliable growth backed by strong fundamentals. The company’s powerful cash flow engine and aggressive share repurchase program also play major roles, as ORLY consistently shrinks its share count each year, boosting earnings per share and supporting long-term stock appreciation.

Its Q3 results reinforced this trend, showing solid revenue expansion, margin improvement, and continued market-share gains. On Oct. 22, ORLY released its third-quarter earnings and delivered another steady, growth-driven performance. Revenue climbed 8% year over year to $4.71 billion, supported by a 5.6% increase in comparable store sales and continued market-share gains across its expanding store base. O’Reilly also showed disciplined cost control, improving its operating margin by 20 basis points and driving roughly 9% growth in both operating and net income. Earnings strength flowed through to shareholders as EPS rose 12% to $0.85, helped by the company’s ongoing share repurchase program. With nearly 6,540 stores in operation and guidance raised for full-year revenue and comps, the quarter reinforced O’Reilly’s ability to deliver consistent mid-single-digit growth, solid profitability, and dependable earnings momentum.

For the fiscal year 2025, ending in December 2025, Wall Street analysts expect O’Reilly’s EPS to grow 8.4% YOY to $2.97 on a diluted basis. The company has a mixed history of surpassing consensus estimates, topping them in three of the trailing four quarters and missing them on another occasion.

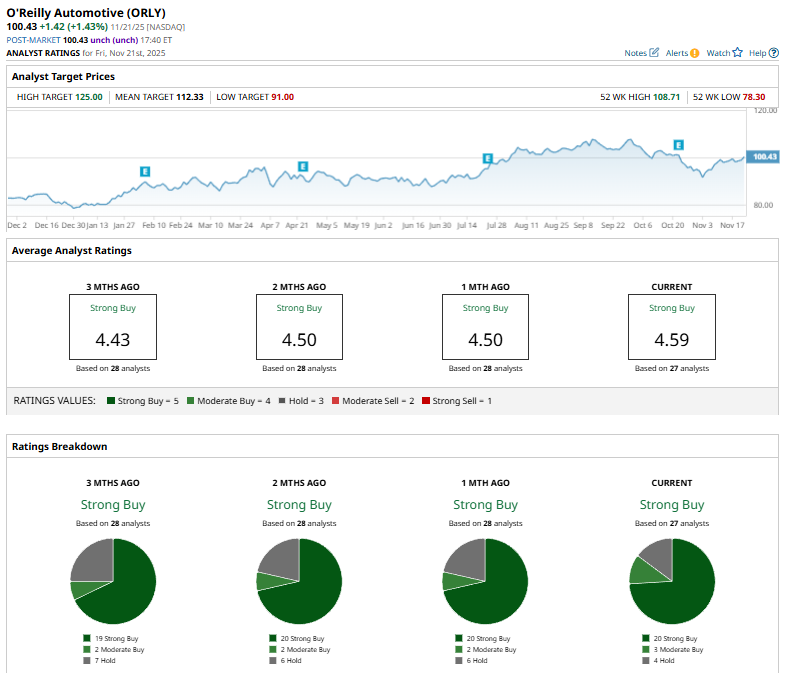

Among the 27 Wall Street analysts covering O’Reilly’s stock, the consensus is a “Strong Buy.” That’s based on 20 “Strong Buy” ratings, three “Moderate Buys,” and four “Hold” ratings.

The configuration is bullish than it was three months ago, with 19 “Strong Buy” ratings.

On Oct. 25, The Goldman Sachs Group, Inc. (GS) analyst Kate McShane reiterated her “Buy” rating on O’Reilly Automotive and raised the price target from $108 to $121, marking a 12% upward revision and signaling strengthened confidence in the company’s outlook.

O’Reilly’s mean price target of $112.33 indicates a 11.8% upside over current market prices. The Street-high price target of $125 implies a potential upside of 24.5%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart