Plug Power (PLUG) has been no stranger to volatility, but the stakes just got a lot higher. After years of ambitious expansion plans, the hydrogen fuel-cell company has decided to suspend work on six U.S. green hydrogen plants—projects that formed the backbone of its long-term growth strategy and were tied directly to a massive $1.6 billion loan guarantee from the U.S. Department of Energy. That loan, awarded in the final days of the Biden administration, was expected to support the construction of green hydrogen facilities across multiple states and help Plug transition from aspiration to scale.

But now, as the company abruptly pauses development and shifts its focus toward data centers, investors are left wondering whether this pivot represents smart strategic realignment. Losing access to low-cost federal financing could be a major blow, especially for a company already burning substantial amounts of cash and facing pressure to prove that its business model can eventually turn profitable.

Against this backdrop, the question becomes unavoidable: with so much uncertainty hanging over Plug Power, should investors buy, hold, or sell PLUG stock here?

About Plug Power Stock

Plug Power is a notable player in the green hydrogen industry, specializing in hydrogen fuel cell technologies. The company is building a comprehensive green hydrogen ecosystem, spanning production, storage, delivery, and energy generation, to support its customers’ business objectives and contribute to economy-wide decarbonization. Its offerings include the GenDrive fuel cell system for material handling vehicles such as forklifts, GenSure stationary fuel cells for grid support, and ProGen fuel cell engines designed for a range of applications. It also offers GenFuel, a comprehensive solution for hydrogen production, storage, and dispensing. PLUG has a market cap of $2.94 billion.

Shares of the hydrogen fuel cell solutions provider have dropped 16.2% year-to-date, with the stock in a steep decline since mid-October.

What’s Driving Plug Power’s Sharp Selloff?

On Wednesday, PLUG shares tumbled more than 11% after the company priced $375 million in senior convertible notes. Notably, Plug intends to use about $245.6 million of the proceeds to fully repay its outstanding principal balance.

Last week, PLUG shares logged their sharpest weekly drop in more than three months, sliding over 15%, after the company opted to suspend activities tied to a Department of Energy (DOE) loan while intensifying its focus on data centers. The stock extended its steep slide on Monday, dropping another 7% and overshadowing news of a significant contract win in the United Kingdom.

Plug Power’s $1.6 Billion DOE Loan in Jeopardy

Well, let’s take a look at what happened with the DOE loan and add some context. In the final days of the Biden administration, the DOE’s Loan Programs Office granted a $1.66 billion loan guarantee for Plug Power to build several hydrogen facilities across the U.S. More precisely, the loan facility was intended to support the development of up to six green hydrogen plants in the U.S. However, U.S. clean energy projects have been dealt a setback as President Trump halted all funding activities and ordered a review. After months of engaging with the DOE, Plug Power decided to suspend activities tied to the loan in November, including “projects previously contemplated in New York and Texas,” according to a filing with the Securities and Exchange Commission.

It’s worth noting that those six facilities were designed to produce and liquefy zero- or low-carbon hydrogen. And the hydrogen produced at the facilities was meant to supply fuel cell electric material-handling equipment, as well as serve the transportation and industrial sectors. However, Plug announced earlier this year a hydrogen-supply agreement to support AI power needs with an unspecified “leading” industrial gas company, a move that “reduces the need for near-term self-deployment of new plants.” Essentially, Plug concluded that buying hydrogen was more cost-effective than taking on a government loan to produce it themselves.

That said, suspending activities on the projects could lead the DOE to revoke its loan-guarantee commitment if it determines Plug Power is no longer meeting the required conditions or expected milestones. Notably, the company has already invested $250 million in the $800 million Texas project and had planned to fund $400 million of it with the DOE loan. “Our decision to temporarily suspend activities related to the DOE loan could adversely affect our access to low-cost capital, delay project execution, and expose us to potential termination or modification of the DOE loan guarantee,” the company said in an SEC filing.

Since halting the activities, Plug Power has announced a series of deals aimed at boosting liquidity and reducing its reliance on federal support. The move that drew the most praise from Wall Street analysts was its plan to sell electricity rights in New York and one other location to energy-hungry AI data centers. Plug will also work with data centers to deliver backup power solutions. This is expected to bring in over $275 million in cash.

Oppenheimer’s Colin Rusch described the deal as a “clever use of assets,” highlighting it as proof of the company’s progress toward profitability. Also, BTIG analyst Gregory Lewis called the monetization “prudent.” In addition, Canaccord analyst George Gianarikas said, “There’s definitely a different feeling in the air; something has changed. After years of constructing its infrastructure—and unfortunately putting the cart before the horse—it appears Plug Power has entered harvest mode.”

Still, this hasn’t reassured investors; rather than celebrating, they saw the possible loss of low-cost federal financing as another risk to the company’s outlook, especially given its ongoing heavy losses. And this is understandable. Plug has invested billions in constructing equipment and facilities to produce hydrogen gas from water and electricity. As mentioned earlier, the company has already put $250 million into the $800 million Texas project, where half of the total cost was expected to be funded through the DOE loan. And now that loan is in jeopardy. Of course, I acknowledge that the company’s strategic pivot appears to be a positive step in general, but given the trade-off, the market’s reaction is completely understandable.

How Did Plug Power Perform in Q3?

Last week, Plug Power reported its financial results for the third quarter of 2025. The company’s revenue grew 1.9% year-over-year (YoY) to $177.1 million, beating Wall Street’s estimates by $0.99 million. The top line got a boost from recognizing long-delayed electrolyzer revenues. GenEco electrolyzer revenue came in at roughly $65 million for the quarter, up 46% sequentially and 13% YoY.

Although revenue exceeded expectations, the company continued to post substantial losses. Its operating loss surged to $348.8 million in Q3, up from $216.2 million in the same quarter last year, while its net loss widened to $363.4 million from $211.1 million. The company outlined roughly $226 million in charges tied to impairments, restructuring, inventory valuation adjustments, and other expenses. As a result, GAAP net loss per share came in at $0.31, significantly missing expectations by $0.18. Notably, without these impairment charges, Plug’s quarterly loss would have been roughly in line with expectations.

A bright spot in the report was the company’s solid progress in reducing cash burn. Net cash used in operating activities stood at $90 million, marking a 49% YoY and 53% sequential improvement. Plug ended the quarter with roughly $166 million in unrestricted cash and cash equivalents. After the quarter, it raised an additional $370 million through the exercise of existing investor warrants.

When it comes to guidance, Plug’s CEO Andy Marsh reiterated, “We are still targeting $700 million in revenue for this year.” Analysts currently project the company to post revenue of $702.95 million for FY25, representing 11.79% YoY growth. Moreover, its annual net loss is estimated to narrow by 70.26% YoY to $0.80 per share.

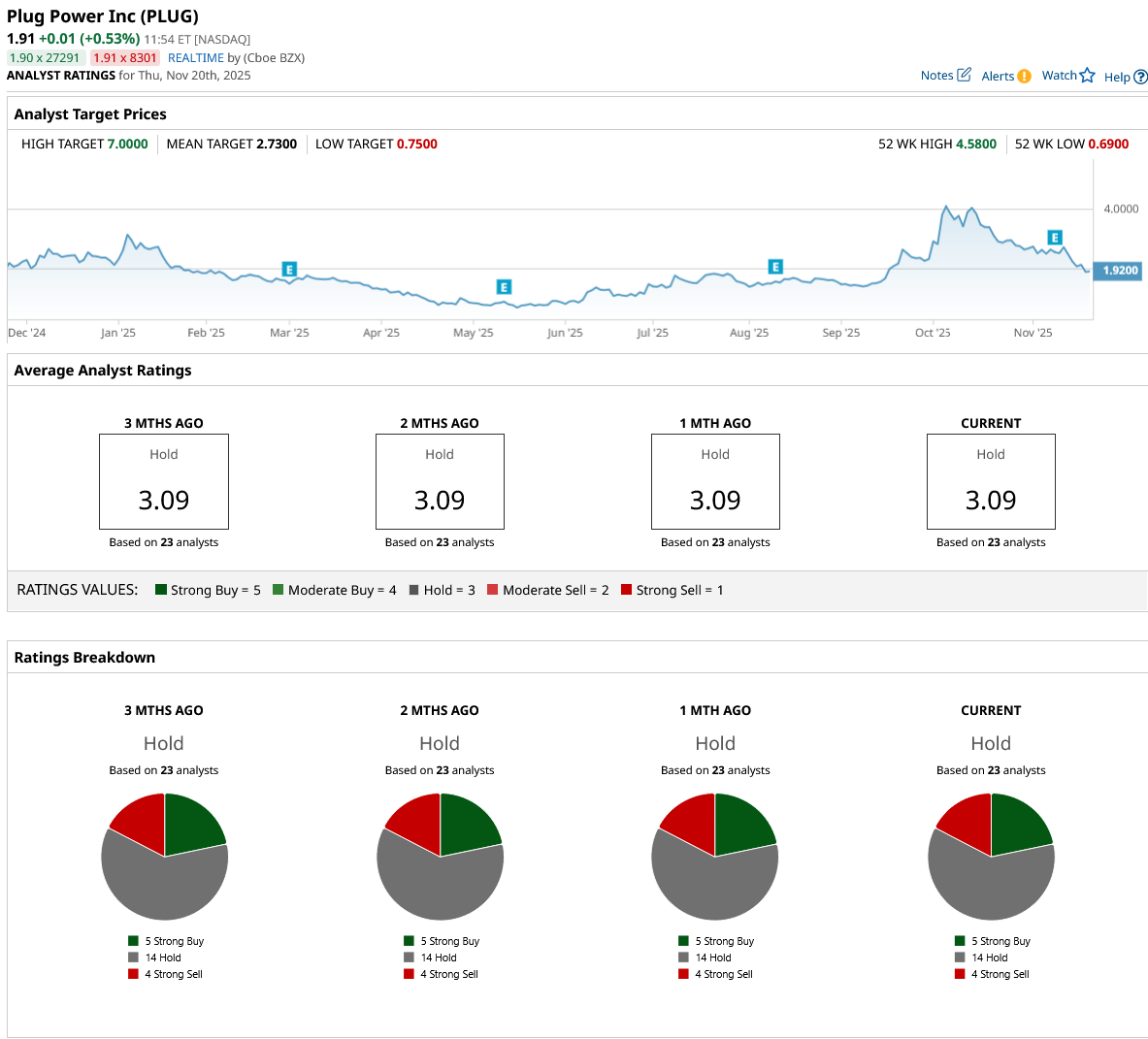

What Do Analysts Expect for PLUG Stock?

Wall Street analysts remain cautious on PLUG stock, as evidenced by the consensus “Hold” rating. Among the 23 analysts offering recommendations for the stock, five rate it a “Strong Buy,” 14 suggest holding, and the remaining four assign a “Strong Sell” rating. Still, PLUG’s mean price target of $2.75 indicates a notable upside potential of 44.7% from current levels.

Putting it all together, I lean toward the bearish cohort of analysts and assign a “Sell” rating. I view the potential loss of low-cost federal financing as a risk to the company’s outlook. Also, Plug lacks a clear path to profitability, which will ultimately lead to further dilution and create more pressure on the stock. While Plug’s plans to work with data centers impressed some analysts, there are many safer and better AI-energy stocks to consider instead.

On the date of publication, Oleksandr Pylypenko did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Wall Street Is Betting on Nuclear Energy, But Legendary Investor Peter Thiel Just Ditched This 1 Key Power Stock

- With $1.6 Billion in Jeopardy, Should You Buy, Sell, or Hold Plug Power Stock Here?

- As Musk Hints That Tesla Could Make Its Own AI Chips, Should You Buy TSLA Stock?

- Think AI Stocks Are Overvalued? Invest in These Data Center Power Trades for the Next Growth Phase.