Protein Hydrolysate Ingredient Market expands as demand rises for fast-absorbing proteins in clinical nutrition, hypoallergenic infant formulas, and performance recovery products worldwide.

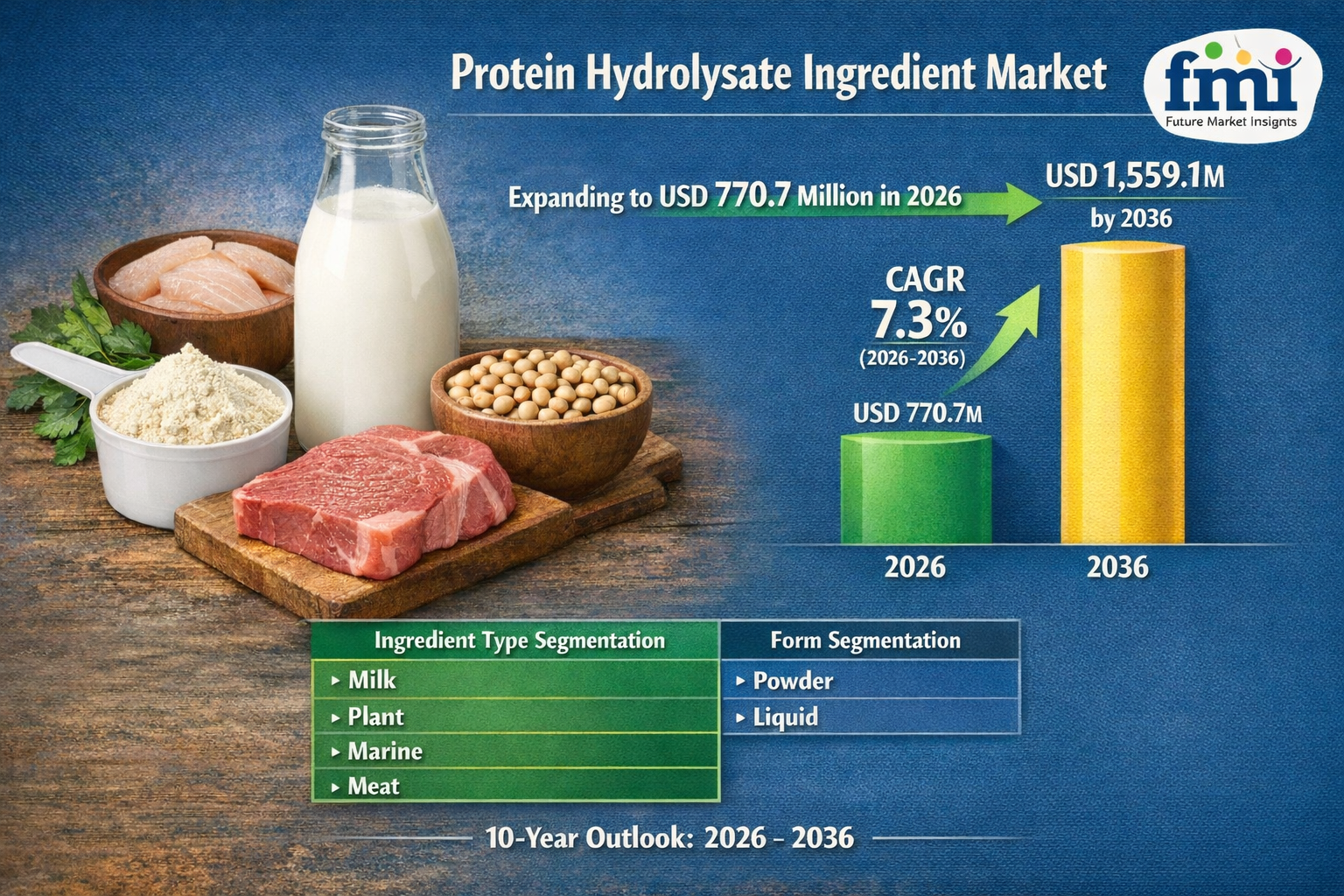

NEWARK, DE / ACCESS Newswire / March 6, 2026 / The global nutrition ingredient industry is entering a new phase of specialization as healthcare-driven nutrition reshapes formulation strategies across infant, clinical, and sports nutrition categories. The Protein Hydrolysate Ingredient Market, which generated USD 718.2 million in 2025, is projected to reach USD 770.7 million in 2026 and expand to USD 1,559.1 million by 2036, registering a CAGR of 7.3% between 2026 and 2036.

According to the latest industry outlook from Future Market Insights (FMI), this expansion is being fueled by rising clinical nutrition requirements, the growing prevalence of pediatric food allergies, and increasing demand for rapidly digestible protein peptides in both therapeutic and performance nutrition products.

What was once a niche ingredient primarily associated with sports supplements is now emerging as a foundational component of medical and early-life nutrition. Manufacturers across the food, pharmaceutical, and nutraceutical industries are now shifting procurement strategies toward highly functionalized hydrolyzed proteins capable of delivering faster absorption and improved digestibility.

Key Market Indicators (2026-2036)

Industry Value (2026): USD 770.7 Million

Forecast Value (2036): USD 1,559.1 Million

Projected CAGR: 7.3%

Dominant Ingredient Type: Milk-Based Hydrolysates

Primary Growth Drivers: Clinical nutrition demand and hypoallergenic infant formulations

Discover Growth Opportunities in the Market - Get Your Sample Report Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-1062

The Peptide Advantage: Beyond Conventional Protein Nutrition

Protein hydrolysates are redefining how protein ingredients are utilized in advanced nutrition systems. Unlike intact proteins that require extensive digestion, hydrolyzed proteins are enzymatically broken down into short-chain peptides and amino acids, allowing the body to absorb them far more efficiently.

This transformation has elevated hydrolysates from simple protein ingredients to high-value clinical nutrition tools used in hospitals, infant formulas, and recovery-focused performance nutrition products.

Industry analysts highlight several reasons behind the growing adoption:

Rising clinical malnutrition cases requiring easily digestible protein sources

Growing pediatric food allergies forcing reformulation of infant nutrition products

Increasing demand for rapid recovery solutions in sports nutrition

According to Nandini Roy Choudhury, Principal Consultant for Food & Beverage at FMI:

"Hydrolysates are no longer limited to sports supplements. They are becoming core components of clinical nutrition programs and specialized infant formulations. Manufacturers capable of optimizing peptide profiling while minimizing bitterness will dominate the premium therapeutic nutrition segment."

Precision Nutrition: From Raw Protein to Specialized Peptide Systems

Manufacturers are moving away from generic protein concentrates and investing heavily in enzymatic hydrolysis technologies that enable highly controlled molecular breakdown of proteins.

This shift is largely driven by massive upstream protein supply. For instance, U.S. facilities alone produced 495 million pounds of whey protein concentrate in 2024, creating a substantial raw material base for hydrolysate production.

To differentiate in an increasingly competitive ingredient market, suppliers are focusing on:

Precision peptide engineering to control molecular weight distribution

Advanced filtration systems to eliminate allergenic protein fragments

Flavor optimization technologies to reduce bitterness from hydrolysis

The growing sophistication of these processes is transforming hydrolysate production into a highly specialized ingredient manufacturing discipline.

Ingredient Segmentation: Dairy Sources Continue to Dominate

Among the various ingredient categories, milk-based protein hydrolysates remain the dominant commercial segment.

These ingredients account for nearly 70% of total consumption in 2026, supported by well-established dairy supply chains and superior amino acid profiles required for infant and medical nutrition.

Several structural advantages support dairy dominance:

Large-scale whey processing infrastructure

Proven safety standards for pediatric nutrition

High biological value protein composition

At the same time, manufacturers are exploring alternative hydrolysate sources including plant, marine, and meat proteins to diversify raw material exposure and create specialized peptide formulations.

Form Evolution: Powder Formats Maintain Market Leadership

Commercial hydrolysate ingredients are primarily traded in powder format, which offers superior shelf stability and logistical efficiency across global supply chains.

Powder hydrolysates provide several advantages for large-scale food manufacturing:

Longer storage life compared to liquid ingredients

Reduced microbial risk due to low moisture content

Efficient integration into nutritional powders and protein bars

Spray drying technologies allow manufacturers to maintain stable peptide structures while producing consistent particle sizes, ensuring precise dosing in automated formulation systems.

Liquid hydrolysates remain important for ready-to-drink clinical beverages, but powder formats continue to dominate bulk ingredient trade.

Regional Performance: Asia Emerging as the Growth Engine

While hydrolysate demand is growing worldwide, regional dynamics vary significantly based on healthcare infrastructure, dairy supply chains, and nutrition regulations.

Key Growth Trends by Country

India (8.6% CAGR): Rapid dairy sector expansion and growing clinical nutrition awareness are accelerating hydrolysate demand.

China (8.5% CAGR): Domestic infant formula manufacturers are upgrading formulations to meet stricter national food safety standards.

Brazil (7.3% CAGR): Rising sports nutrition adoption is driving demand for whey-derived hydrolysate blends.

United Kingdom (6.9% CAGR): Aging populations are increasing reliance on specialized medical nutrition solutions.

Germany (6.9% CAGR): Strong infant formula export infrastructure supports hydrolysate ingredient consumption.

United States (5.8% CAGR): High food allergy prevalence continues to sustain demand for hypoallergenic nutrition products.

In Asia, governments are increasingly encouraging domestic production of high-value nutrition ingredients, which is creating joint venture opportunities between Western technology providers and regional manufacturers.

Navigating Market Constraints

Despite strong demand, hydrolysate producers face several technical and commercial challenges.

The most significant barrier remains flavor degradation caused by extensive enzymatic protein breakdown. Hydrolysis often exposes hydrophobic amino acids that create bitter taste profiles, making formulation difficult for mainstream consumer products.

Manufacturers are addressing this challenge through:

Selective enzymatic cleavage technologies

Advanced peptide purification techniques

Flavor masking and bitterness reduction systems

However, these technologies significantly increase production costs, which is why hydrolysates remain concentrated in high-value medical, pediatric, and specialized nutrition markets.

Competitive Landscape: Innovation and Regulatory Expertise Drive Leadership

The protein hydrolysate ingredient industry is dominated by specialized ingredient suppliers with strong regulatory expertise and advanced processing capabilities.

Companies that secure regulatory approvals for specific peptide fractions often establish long-term supply agreements with multinational nutrition brands, creating powerful competitive advantages.

Major industry participants include:

Arla Foods Ingredients

FrieslandCampina Ingredients

Roquette Frères

Darling Ingredients

Glanbia Nutritionals

Kerry Group

Fonterra Co-operative Group

Tate & Lyle

Carbery Group

AMCO Proteins

Strategic consolidation is also shaping the competitive environment. For example, Arla Foods Ingredients recently received regulatory approval to acquire Volac Whey Nutrition, strengthening its position in global whey ingredient manufacturing.

The Outlook: Specialized Peptides Becoming Core Nutrition Infrastructure

Looking ahead to 2036, protein hydrolysates are expected to transition from specialized ingredients to essential components of therapeutic nutrition systems.

As healthcare providers increasingly adopt nutrition-based medical interventions, demand for rapidly absorbable protein formats will continue to expand across hospitals, elderly care facilities, and pediatric nutrition programs.

Combined with rising awareness around muscle health, allergy management, and recovery nutrition, hydrolysate ingredients are poised to play a critical role in the evolution of next-generation functional foods.

The industry's future will be shaped by companies capable of combining enzymatic precision, sensory optimization, and regulatory compliance-delivering specialized protein solutions designed for the most demanding nutritional applications.

For an in-depth analysis of evolving formulation trends and to access the complete strategic outlook for the Protein Hydrolysate Ingredient Market through 2036, Full Report Request - https://www.futuremarketinsights.com/reports/protein-hydrolysate-ingredient-market

Related Reports:

Protein Ingredients Market: https://www.futuremarketinsights.com/reports/protein-ingredient-market

Protein Hydrolysate For Animal Feed Application Market: https://www.futuremarketinsights.com/reports/protein-hydrolysate-for-animal-feed-application-market

Protein Hydrolysate Market: https://www.futuremarketinsights.com/reports/protein-hydrolysate-market

Soy Protein Ingredient Market: https://www.futuremarketinsights.com/reports/soy-protein-ingredient-market

Fish Protein Hydrolysate Market: https://www.futuremarketinsights.com/reports/fish-protein-hydrolysate-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - sales@futuremarketinsights.com

For Media - Rahul.singh@futuremarketinsights.com

For web - https://www.futuremarketinsights.com/

SOURCE: Future Market Insights, Inc.

View the original press release on ACCESS Newswire